The Case for Risk Managed Income ETFs

On August 26th, 2021, we listed the Global X Nasdaq 100 Risk Managed Income ETF (QRMI) on the Nasdaq stock exchange and the Global X S&P 500 Risk Managed Income ETF (XRMI) on the New York Stock Exchange (NYSE). In this piece, we explain why investors may want to consider risk managed income strategies and how QRMI and XRMI can be efficient ways of gaining this exposure.

Key Takeaways

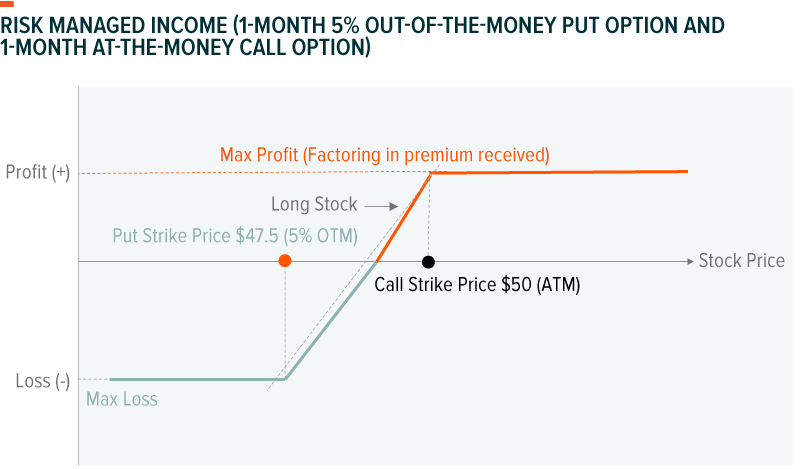

- Risk managed income strategies typically own the securities in an equity index, while also selling a covered call option on that index and buying an out-of-the-money (OTM) protective put. This is a net credit collar strategy, meaning it expects to generate positive option premium income, while protecting against market selloffs.

- Risk managed income strategies are typically used as long-term strategic allocations in income-oriented portfolios, given that they have negligible inflation risk and seek to provide a diversified source of income.

- In exchange of pursuing net option premium income, risk managed income strategies forfeit upside participation in their underlying equity index and may experience some albeit limited, downside risks.

- XRMI and QRMI sell one month at-the-money (ATM) call options and purchase one month 5% OTM put options on their respective equity indexes.

What Are Risk Managed Income Strategies?

Today, investors face a difficult challenge in managing their investments: how to generate enough income amid a low interest rate environment, while mitigating the risks of rising rates or major market selloffs. Traditional fixed income instruments, like government, corporate, and municipal bonds, tend to preserve capital, but currently offer historically low yields and are sensitive to rising rates and inflation. Meanwhile high dividend stocks, REITs, and MLPs are often less sensitive to rates and generate high yields, but can be susceptible to drawdowns.

One potential solution for investors to consider are risk managed income strategies, which utilize options to generate an alternative source of portfolio yield, while mitigating downside risks. To strike a balance between these outcomes, risk managed income strategies couple a covered call with a protective put. A covered call involves purchasing securities, such as equities, and then simultaneously selling a call option on those securities. A call option gives the buyer the right, but not the obligation to buy a security at a pre-determined strike price within a given time frame. Selling covered calls can generate high income that has little or no interest rate risk, in exchange for forfeiting the upside potential of the underlying equity securities. By buying a put option for the same securities, a protective put can mitigate losses if the market sells off. A put option gives the buyer the right, but not the obligation to sell a security at a pre-determined strike price within a given time frame in exchange for paying a premium.

Such strategies are also considered ‘net credit collars’ where the premium received from selling the call option exceeds the cost of purchasing the put, resulting in a positive income stream to the investor. To achieve this outcome, a risk managed income strategy typically must write the call option at or close to at-the-money (meaning the strike price equals the current price of the underlying security), while purchasing a further out-of-the-money put option. This way the price of the put option costs less than the call option sold. To illustrate how this ‘net credit collar’ aspect works, we can use the example of stock XYZ and the difference between purchasing an ATM vs. OTM put option. An investor buying stock XYZ and an at-the-money (ATM) put option at XYZ’s current share price effectively hedges against downside moves. But ATM put options are also more expensive than OTM put options and could expire worthless if XYZ rises. Buying an OTM put option that is 5% below XYZ’s strike price will likely cost less, but will only begin to protect against losses in excess of 5%. The less costly 5% OTM put option, as opposed to the more costly ATM put option is how this risk managed income strategy becomes a ‘net credit collar’.

Why Should Investors Consider Risk Managed Income Strategies

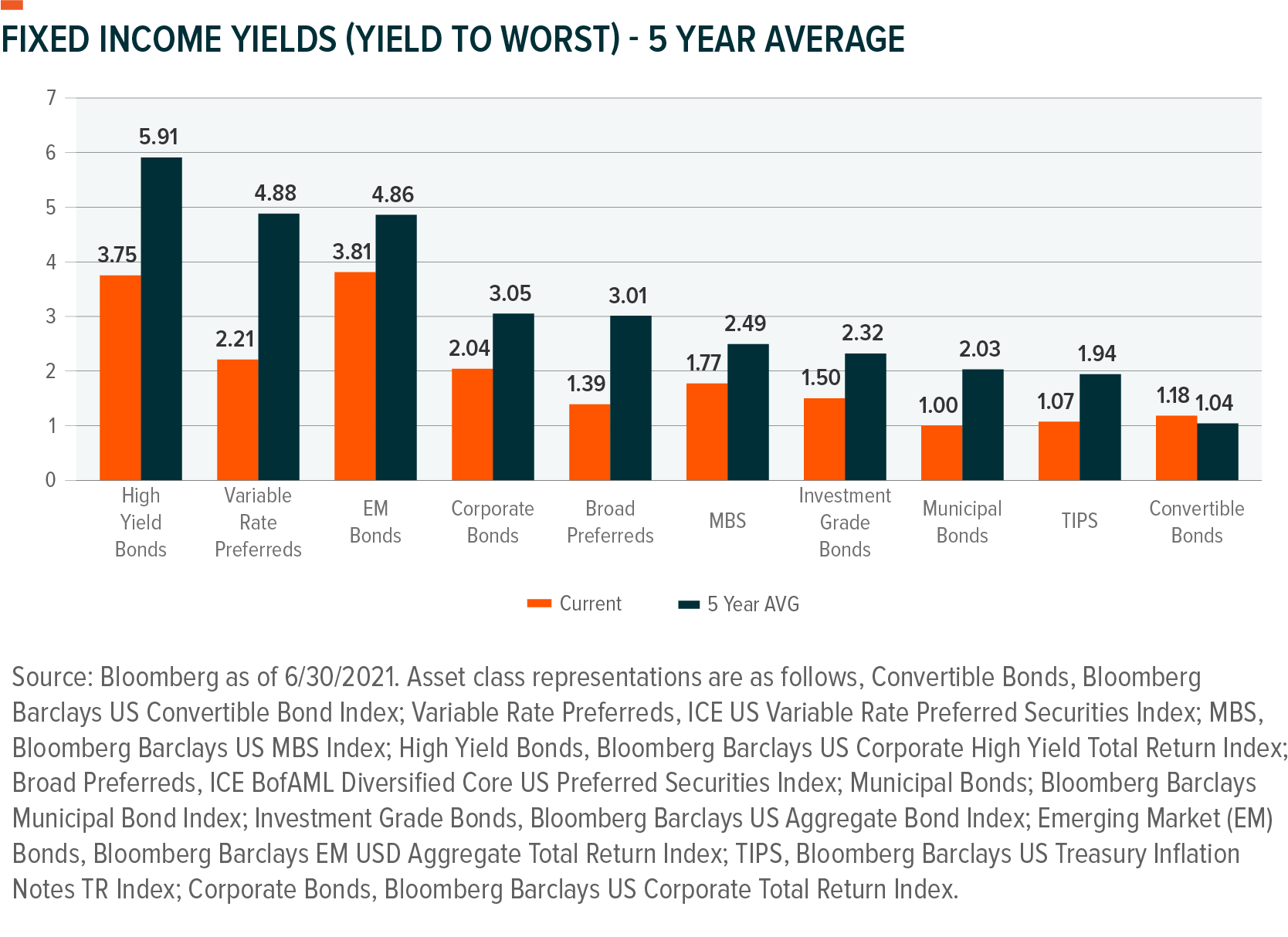

Central banks in many developed markets have set policy rates at zero, or negative levels, presenting challenges for investors who rely on their portfolios for income. The fixed income space, traditionally a mainstay in retiree portfolios, is in the midst of a three-decade-long rally with unprecedented levels of central bank support. As such, yields across nearly all major fixed income sectors are trading well below historical averages. This dynamic is often forcing investors into higher credit risk or longer duration areas in the hunt for more meaningful yields. But if rates rise or economic conditions weaken, risks could quickly materialize.

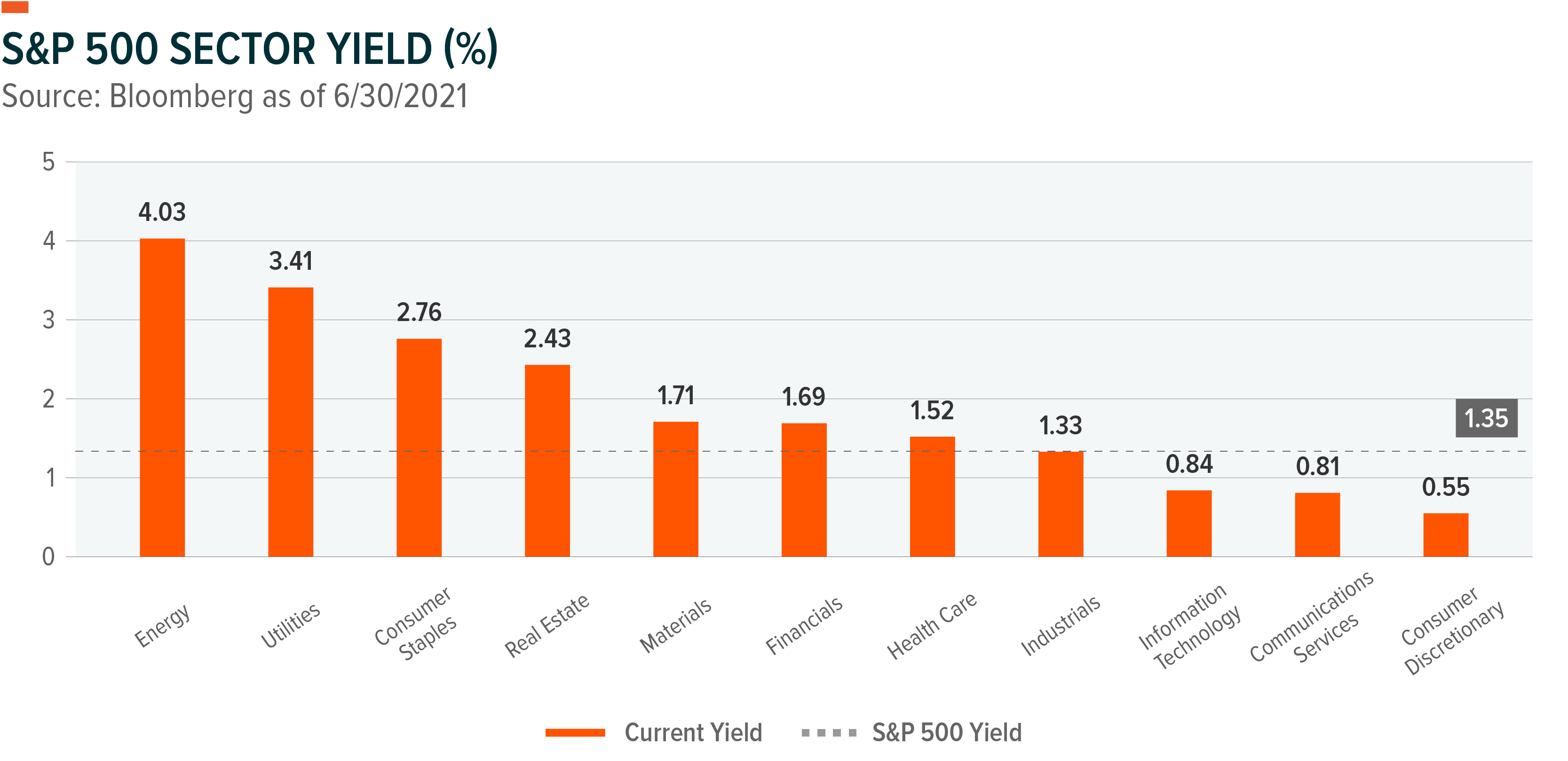

Similarly, within the equities space, dividend yields are low, even in areas that typically used to offer meaningful yields, like Real Estate and Utilities, resulting in inadequate income opportunities from the asset class.

One area that has thrived in the current market environment are covered call strategies. Covered calls aim to generate high income by selling call options that forfeit some or all of the upside potential of an underlying asset in exchange for a premium. This can be a particularly helpful strategy in sideways or upwards trending markets as investors can collect premium income, while volatility is low. They can also be useful if investors are concerned about rising rates, because the income generated from covered calls has a negligible relationship with interest rates.

But for many retirees, income generation can be just as important as protecting their principal amid selloffs. Covered call strategies offer limited downside protection (to the extent that options premiums received would offset some or all of the decline) and therefore may not meet particularly risk-sensitive investors’ needs. Risk managed income strategies seek to address this by combining a covered call with a protective put. When designed correctly, a risk managed income strategy should generate income (albeit less than a similar covered call strategy), while limiting downside risks.

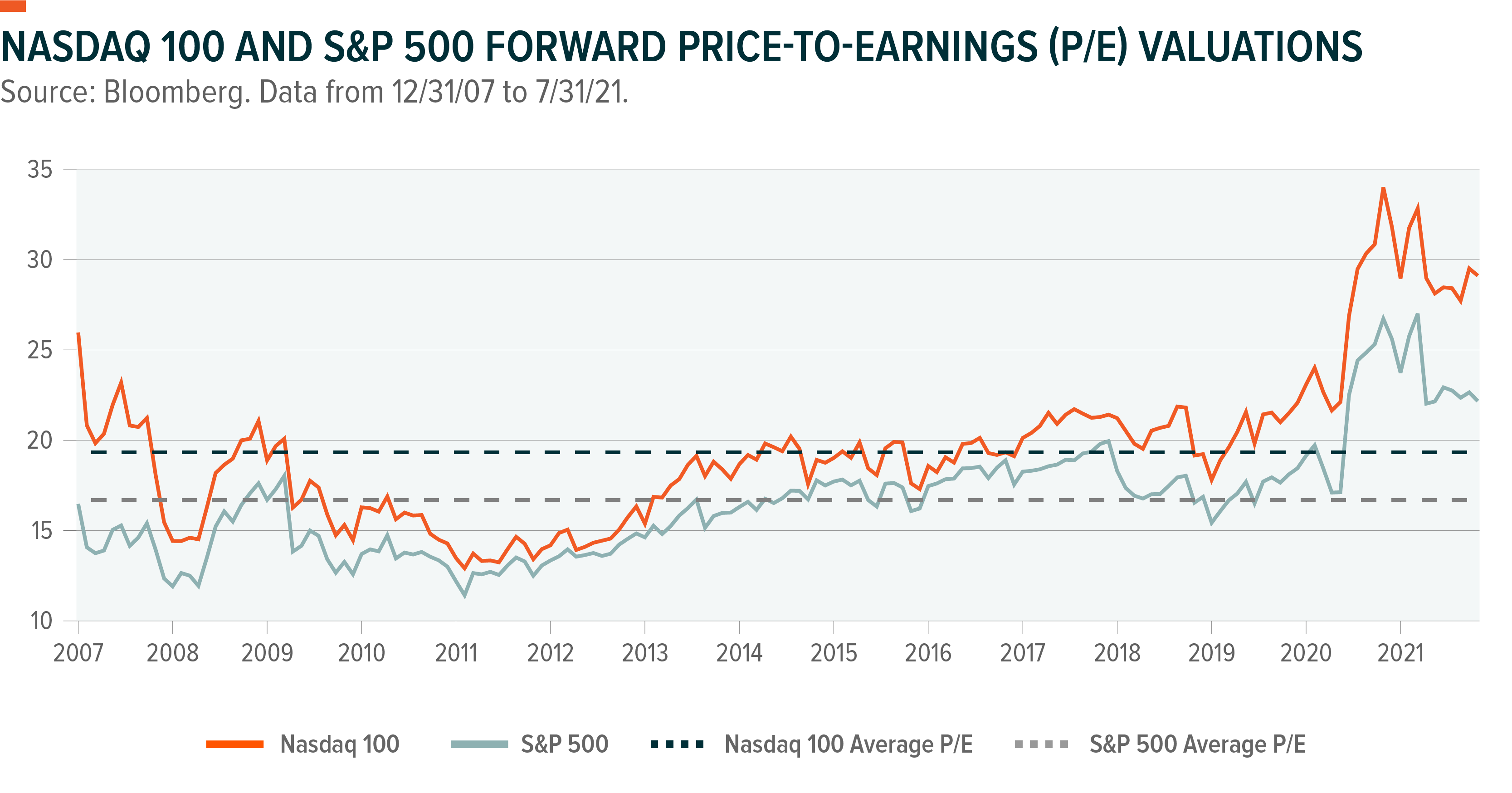

Investors may be wise to consider protecting against downside risks given that U.S. equity markets have been in a decade-plus long bull market. Both the Nasdaq 100 and S&P 500 are trading at valuations well above historical averages, which can introduce greater downside risk potential if valuations normalize.

Global X Risk Managed Income Strategies, Explained

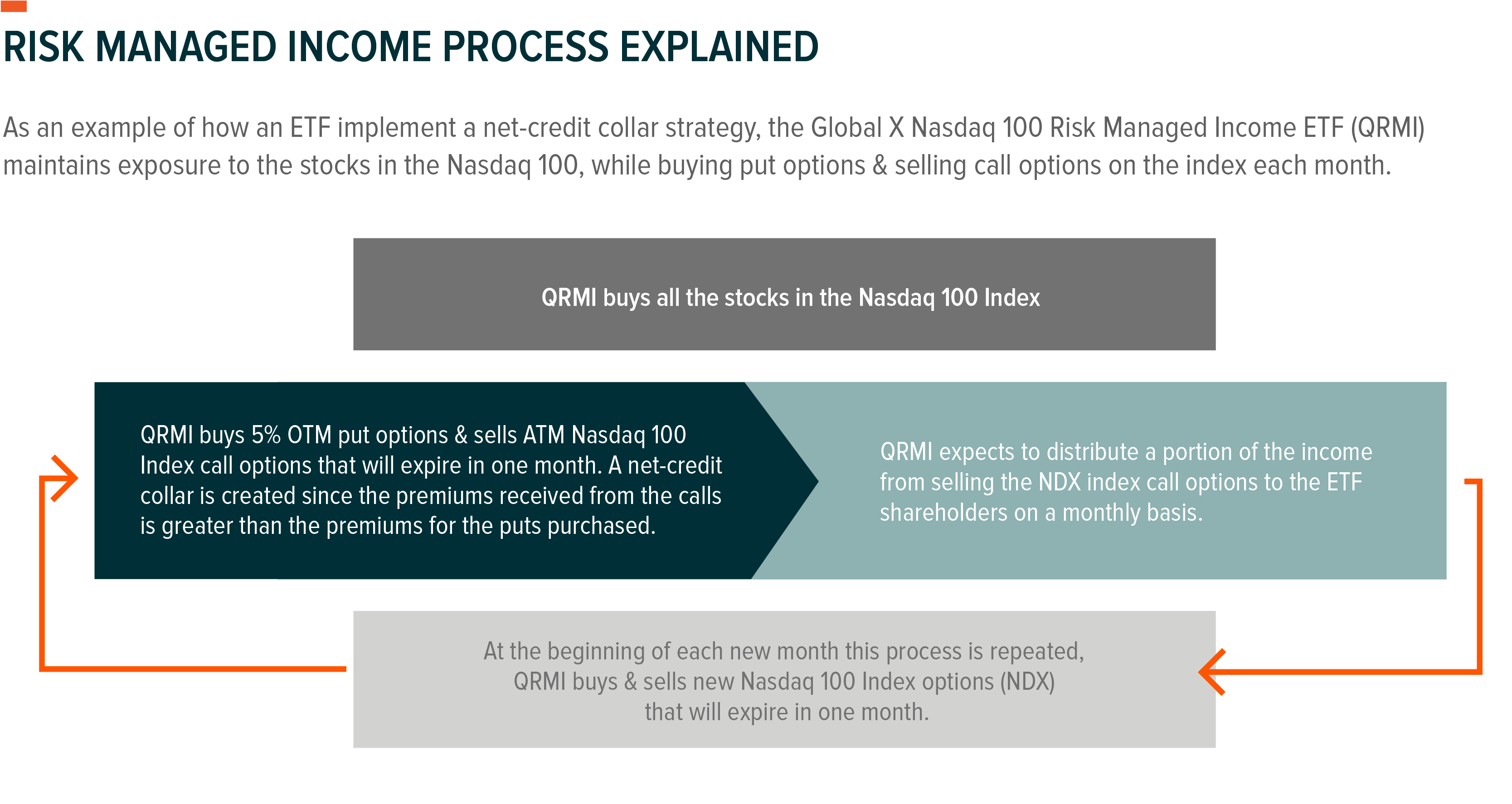

The QRMI and XRMI ETFs are designed to provide a monthly source of income to investors, combined with a measure of downside risk mitigation. Both funds follow similar processes, but have different underlying indexes: the Nasdaq 100 and the S&P 500, respectively. Using QRMI as an example, Global X portfolio managers replicate the Nasdaq 100 Index by purchasing each of the stocks in their assigned weights. They then sell an at-the-money (ATM) call with an expiration date in one month. They couple that position with the purchase of a put option that is 5% OTM with an expiration date in one month. QRMI expects to settle the previous month’s options on their expiration dates and distribute a portion of the net income from the options premiums. Portfolio managers then enter into new one month options positions and the process repeats.

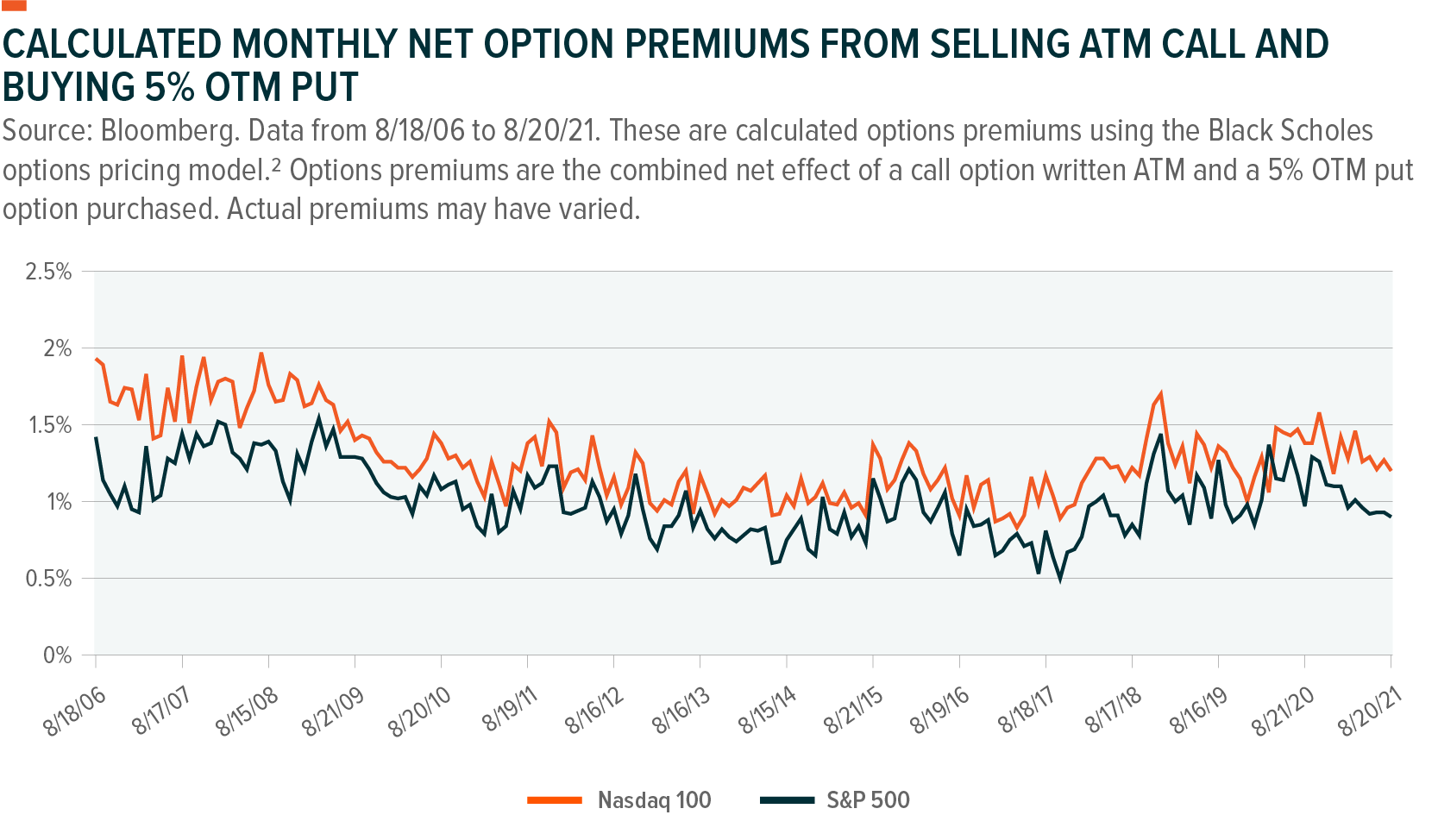

A key feature of risk managed income strategies is the expected net credit from the two options positions, which is expected to create an income stream for investors. Using the Black-Scholes options pricing model, we can see the simulated expected monthly premiums received for both Nasdaq 100 and S&P 500 strategies that sell ATM call options and buys 5% OTM put options. The frequency is measured every month for monthly options written and purchased. Monthly levels averaged approximately 1.30% and 1.01% for Nasdaq 100 and S&P 500 respectively, resulting in annualized figures of 15.6% and 12.12%. Given that options premiums are positively correlated to volatility, we can see net premiums spiked during more volatile periods like the global financial crisis in 2008 and the COVID-19 pandemic in 2020.

Using Risk Managed Income Strategies In a Portfolio

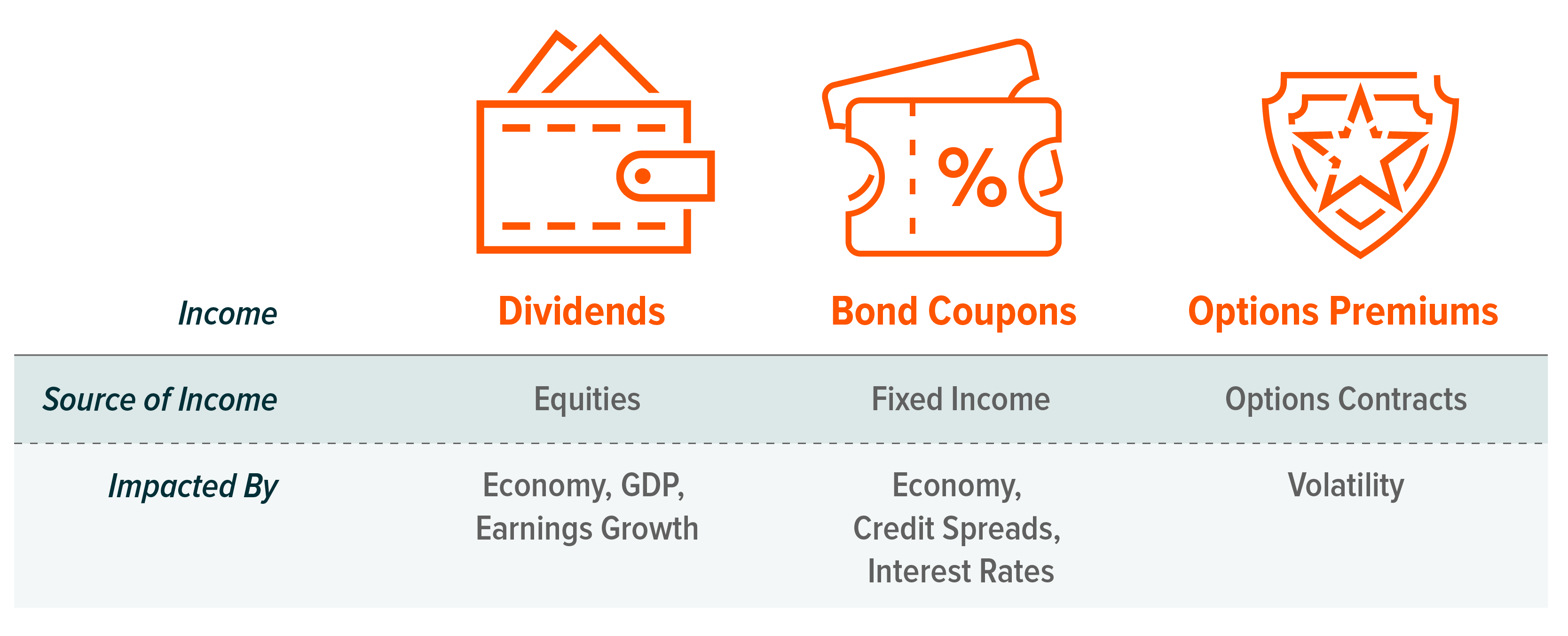

Risk managed income strategies can offer an alternative source of yield to income portfolios. While bond coupons are impacted by interest rates and credit spreads, and dividends are driven by earnings and economic strength, risk managed income from premiums is driven primarily by volatility. As volatility increases, option premiums become more expensive, resulting in a greater net credit between selling the ATM call option and buying the OTM put.

Given the unique source of income, risk managed income strategies can serve as a diversifier in an income portfolio, either in an alternatives bucket or by reducing exposure to equities. More specifically, income investors are often underweight tech exposure and may enhance diversification by adding a risk managed income strategy based on the tech-heavy Nasdaq 100.

Conclusion

In today’s low yield environment traditional sources of income are simply not solving many investors’ income needs – a situation that could be exacerbated by rising rates. We believe the Global X Nasdaq 100 Risk Managed Income ETF (QRMI) and the Global X S&P 500 Risk Managed Income ETF (XRMI) can be important diversifiers in income-oriented portfolios, by generating a source of income that is not tied to rates and has protections to mitigate downside risks.

Related ETFs

QRMI: The Global X Nasdaq 100 Risk Managed Income ETF (QRMI) invests in the securities of the Nasdaq 100 with a 1-Month 5% Out-of-the-Money (OTM) Put and 1-Month At-the-Money (ATM) Call net credit collar option overlay in an effort to generate income while providing a floor on potential losses.

XRMI: The Global X S&P 500 Risked Managed Income ETF (XRMI) invests in the securities of the S&P 500 with a 1-Month 5% Out-of-the-Money (OTM) Put and 1-Month At-the-Money (ATM) Call net credit collar option overlay in an effort to generate income while providing a floor on potential losses.