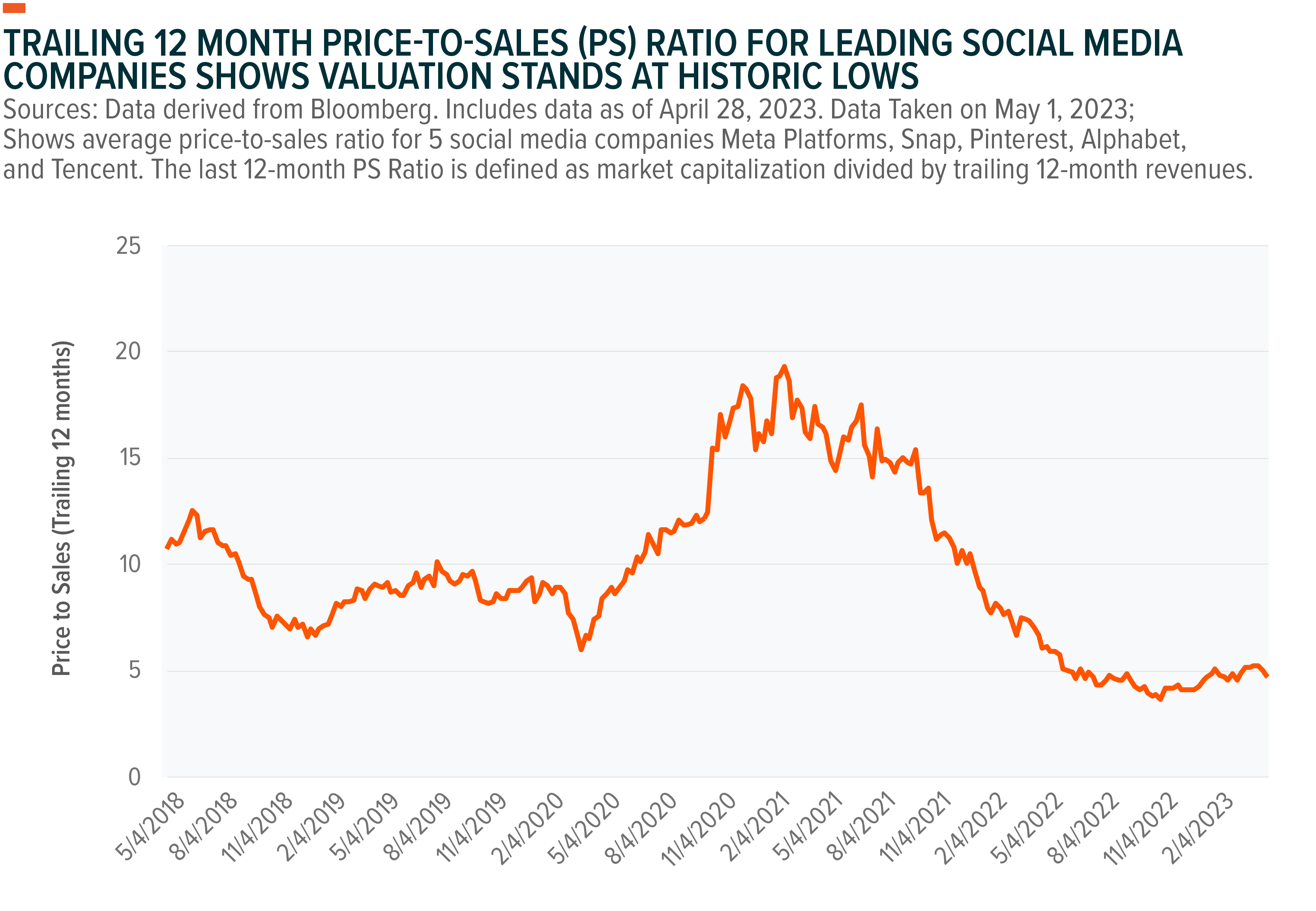

Social Media: Thriving Engagement and Low Valuations Could Potentially Drive Outperformance

Social media platforms continue to cement their role in the lives of everyday consumers, despite receding COVID-19 tailwinds. Time spent and user engagement are visibly up across leading global services, including Meta Platforms, YouTube, TikTok, Snapchat and more. While a weak broader advertising market has kept top-line growth in check for social platforms, we believe that dollars follow attention and that social media companies will grow much faster relative to legacy channels when the broader ad market recovers. With valuations for social media companies near historic lows, the investment case appears increasingly attractive.

Key Takeaways

- Time spent on social media platforms has grown consistently for the past three years. We believe this migration of attention away from legacy channels could be permanent.

- Investments in emerging formats by social media platforms, such as short video, have been extremely successful in exacerbating the shift of time spent away from legacy media.

- A recovery in ad spending from the slump of 2022 could allow top-line growth for social media companies to rebound. Attractive valuations appear to offer an exciting entry point.

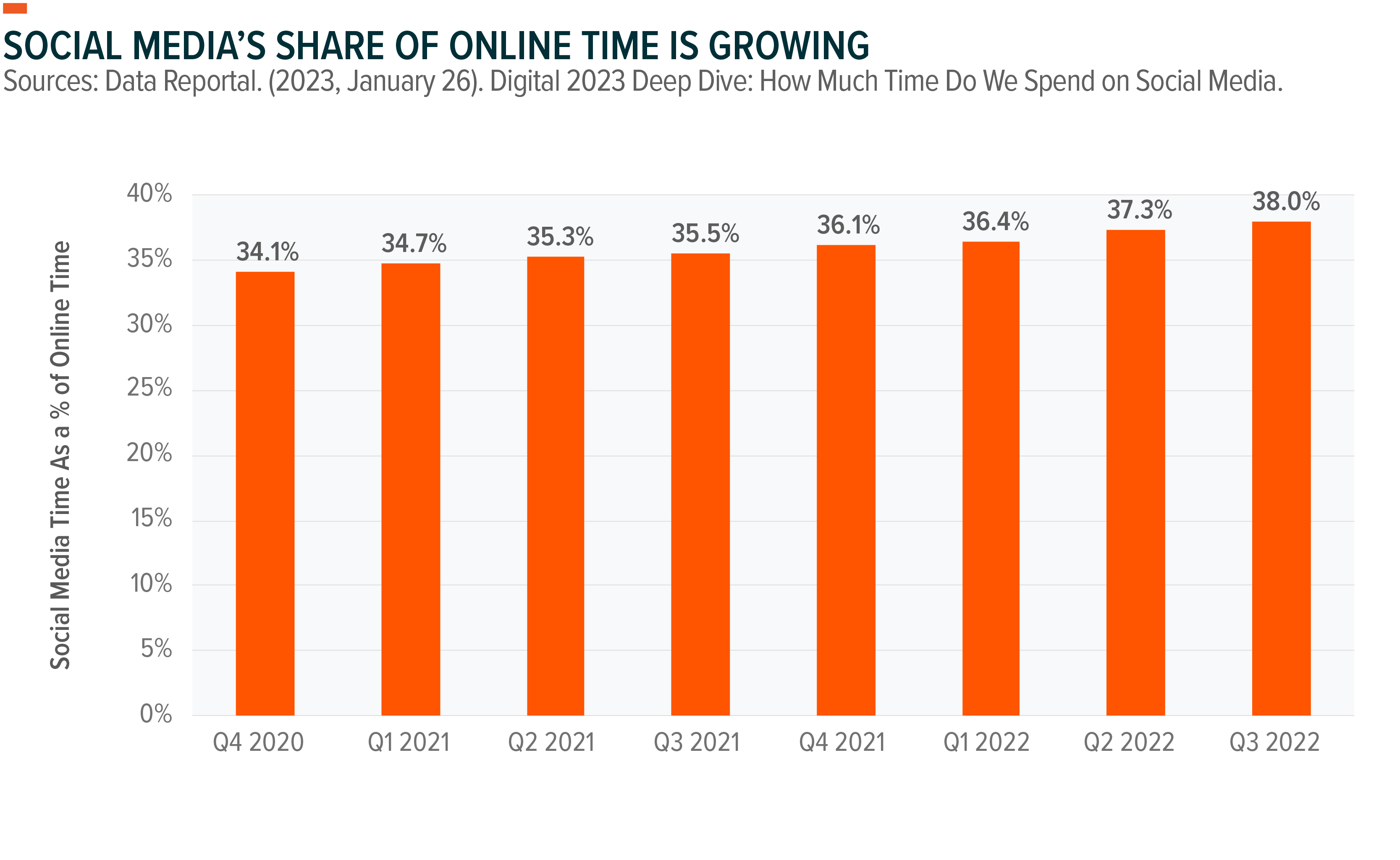

Social Media’s Share of Attention Is Growing

Nearly 4.9 billion people use social apps around the world, with an average individual spending 2 hours and 31 minutes on social platforms daily.1,2 Even as time spent online as a whole declines, social media’s share of time spent online continued to grow, increasing three percentage points in the past 12 months.3

That growth, even as people return to the normalcy of outdoor leisure, commuting, and the office, underlines the unrivaled position of social platforms as the primary channel for digital leisure time for everyday consumers, as platforms have successfully bundled broader entertainment, news, and other content verticals into their folds.

Recent quarterly releases from leading social media companies further substantiate growing engagement. For the most recently reported quarterly results, Meta Platforms managed to report 3.02 billion daily active users across its family of apps, up 5% year-over-year (YoY).4 Snapchat, which runs a social messaging application, topped 383 million daily active users, up 15% YoY.5 Alphabet’s YouTube continues to be a leading platform in streaming time share, beating Netflix and other popular streaming video on demand (SVOD) services.6

Gaming platforms structured around social profiles, such as Roblox, have seen similar growth momentum. Roblox reported 67.3 million daily active users, up 22% YoY for the month of February 2023.7 We believe this shift of attention could be permanent, boosted by the improving network effects, growing volumes of content on these platforms, and bundled services, which reinforces a growth flywheel effect.

Social also wins from the parallel erosion of legacy channels. Time spent watching TV in the US has been on a spiral decline, expected to drop another 17% YoY in 2023.8 Readership for newspapers has been on a secular decline, as well.9 The shift is even more profound in younger generations. Nearly 47.3% of Gen Z spends more than three hours a day on social media in the US, as TV viewership continues to shrink.10

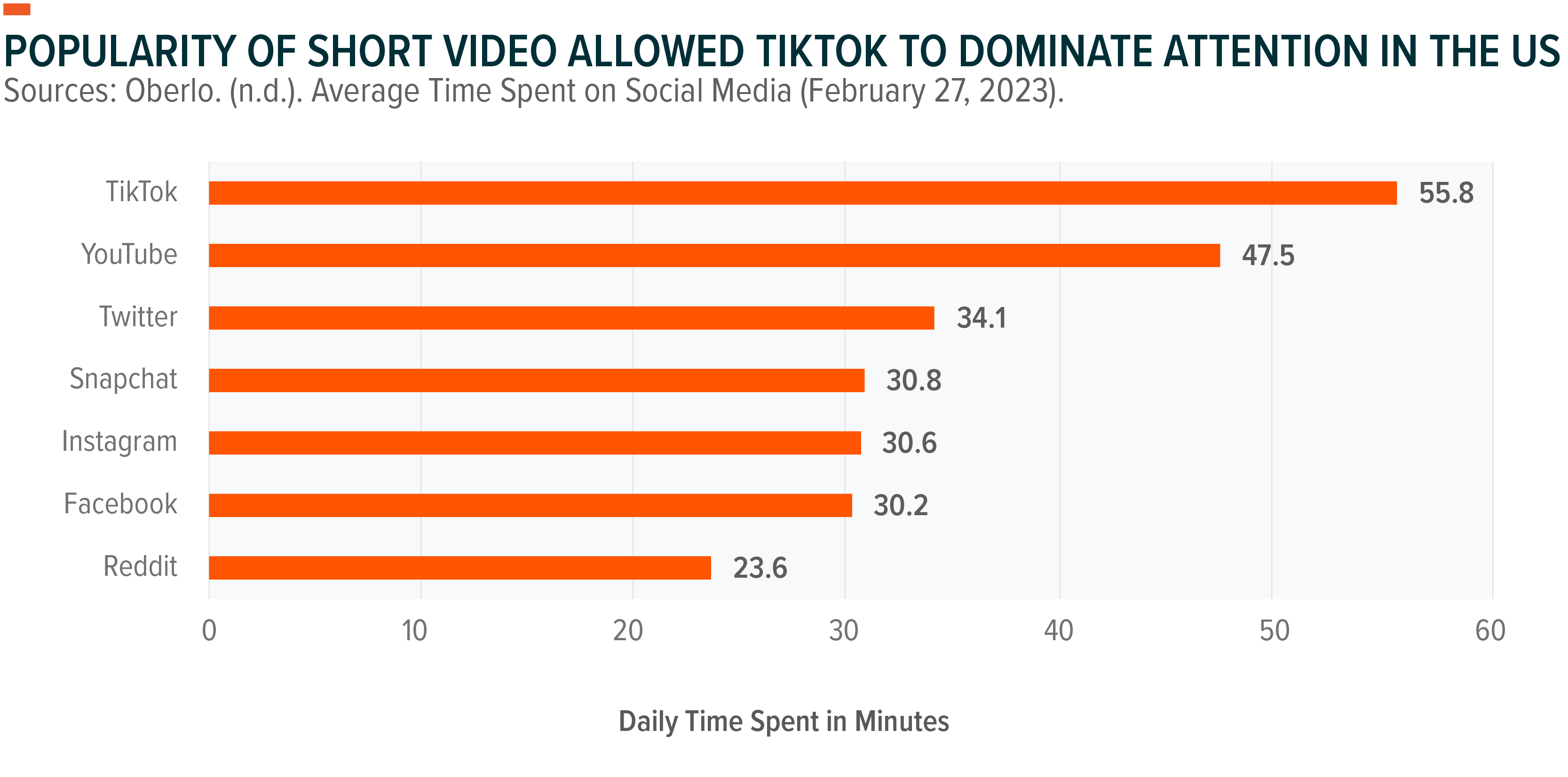

Short Video Chapter Is Just Getting Started

The success of TikTok brought short video under focus. In just under five years, TikTok managed to displace major social networks to command 55.8 minutes a day spent on the platform by the average US user.11 That growth helped TikTok earn an estimated $11 billion in revenues last year.12

The popularity of the format forced other platforms to integrate short video. As a result, engagement across Meta’s Instagram-Reels, Snapchat’s Spotlight, and Alphabet’s YouTube-Shorts is growing rapidly. This has led to an increase in impression inventory that is yet to be monetized effectively by platforms. For example, Meta indicates that only 40% of advertisers have begun embracing Reels for ads.13 We believe the short video channel displays the potential to become the primary driver of growth for these platforms for the next couple years.

Moreover, while TikTok has managed to retain pole position so far, its dominance is threatened by growing regulatory risk, and we view that as a positive for Meta Platforms, Google’s YouTube, and Snap. If regulators restrict TikTok’s reach in the US, the attention and nearly $11 billion in revenues will be up for takes, which could considerably boost growth for Meta, Alphabet, and Snap.

Lastly, we believe short video also offers an exciting segue into immersive content. As users continue to spend more time on social platforms, and embrace escapism, consumer tech will have to evolve to service emerging needs – accommodating immersive experiences, multi-modal input, intuitive interfaces, faster connections, and a new set of user demands.14

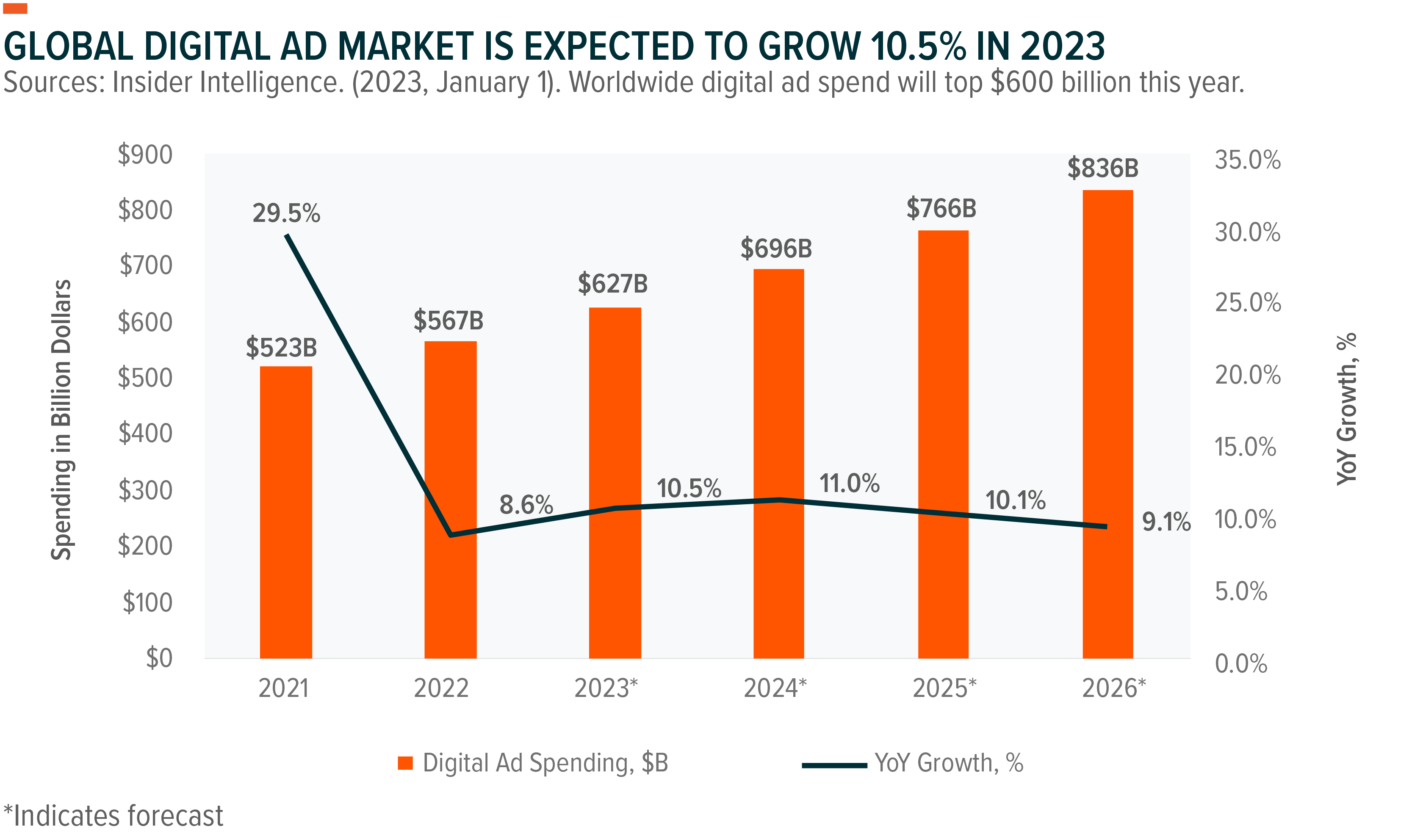

Return to Growth Is Highly Likely

Rising interest rates and growing expectations for a recession discouraged brands from generously spending on ads in 2022. As a result, the digital advertising industry reported its first single-digit growth year in history.15 Meta Platforms, Alphabet, Snap and other ad-based social platforms reported YoY revenue declines.

However, a swift recovery is anticipated in 2023. Spending on digital ads is expected to rise 10.1% this year, with growth accelerating in the following years.16 Given the growth witnessed by social platforms in terms of engagement during the downturn, we believe these platforms will be outsized beneficiaries in a recovery. Moreover, nearly 34.8% of total global advertising spending is still allocated to non-digital channels, portions of which should likely also move online.17

Meanwhile, social media companies have been using the downturn to cut costs aggressively. Meta Platforms shed 11,000 jobs in its last round of cutbacks, while Alphabet slashed 12,000 jobs and paused hiring.18,19 These cuts, coupled with strategic reallocations of resources, should allow these companies to get leaner, powering bottom-line efficiencies in the coming years.

Generative AI is another major driver of future growth. From helping create personalized content, to better targeting ads to users, to more sophisticated and effective chatbots for small and medium businesses, generative AI can help social media platforms increase their monetization with a host of features targeted at users, merchants, and brands.

Conclusion: Opportunity for Potential Outperformance

Weakness displayed by the broader advertising market, due to persistent inflation and uneven macroeconomic conditions, is keeping growth in check for social media platforms. However, platform engagement continues to thrive, as consumers default to social digital channels for news, entertainment, and content services. With the advertising drought likely ending, aided by easing, we believe social platforms could return to growth while potentially delivering enhanced bottom-line performances. Despite the market’s favorable treatment recently, valuations still appear attractive for the cohort.

Related ETFs

SOCL – Global X Social Media ETF

Click the fund name above to view current holdings. Holdings are subject to change. Current and future holdings are subject to risk.