Silver, Explained

Silver is often viewed as secondary to its more prominent counterpart, gold. However, the metal has become increasingly differentiated and now stands on its own merits, supported by unique properties that make it attractive as both a precious metal and an industrial commodity. Below, we explain what makes silver a compelling and distinctive investment by answering five key questions.

- How and where is silver extracted?

- How is silver used today?

- What is silver’s relationship to gold, and what differentiates silver?

- What are silver’s supply and demand dynamics?

- What are the differences between investing in physical silver, futures, and silver mining stocks?

How and Where Is Silver Extracted?

Silver ore is mined through both open-pit and underground methods. The open pit method involves using heavy machinery to mine deposits relatively near the Earth’s surface. In underground mining, tunnelling deep shafts into the ground allows for the extraction of the ore. Once extracted, the ores are crushed, ground and separated through a process called flotation, which typically increases the concentration of mineral values by 30 to 40 times.1 Refiners then further concentrate this extraction through the process of electrolysis or amalgamation.

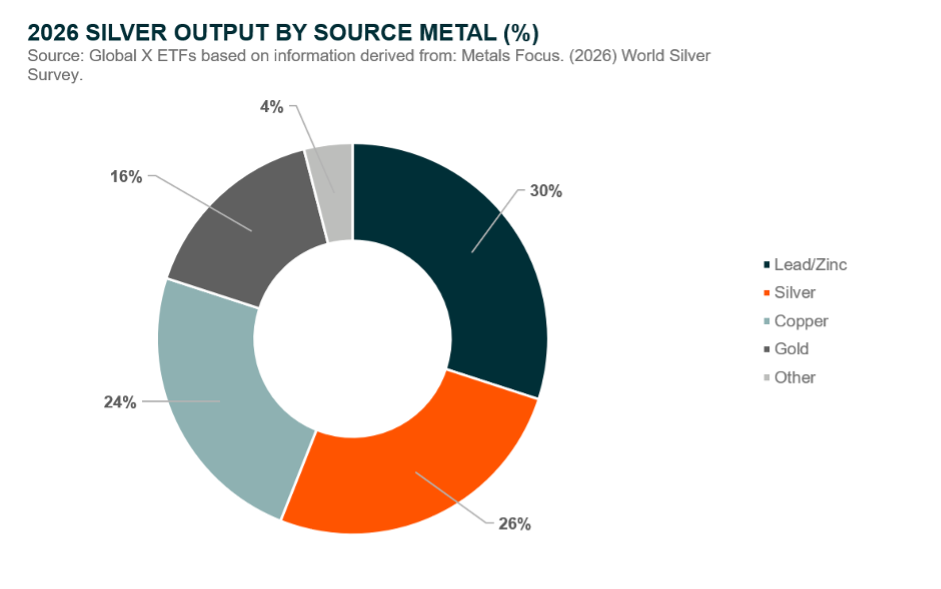

As of 2026, only 26% of silver derives from mining activities where silver comprises the primary source of revenue.2 The remaining 74% comes from projects where silver is a by-product of mining other metals, such as copper, lead, and zinc.3 As one would expect, the revenues of firms focused on primary silver production tend to demonstration higher correlation to, and is more impacted by fluctuations in the silver price than firms that produce it as a by-product.

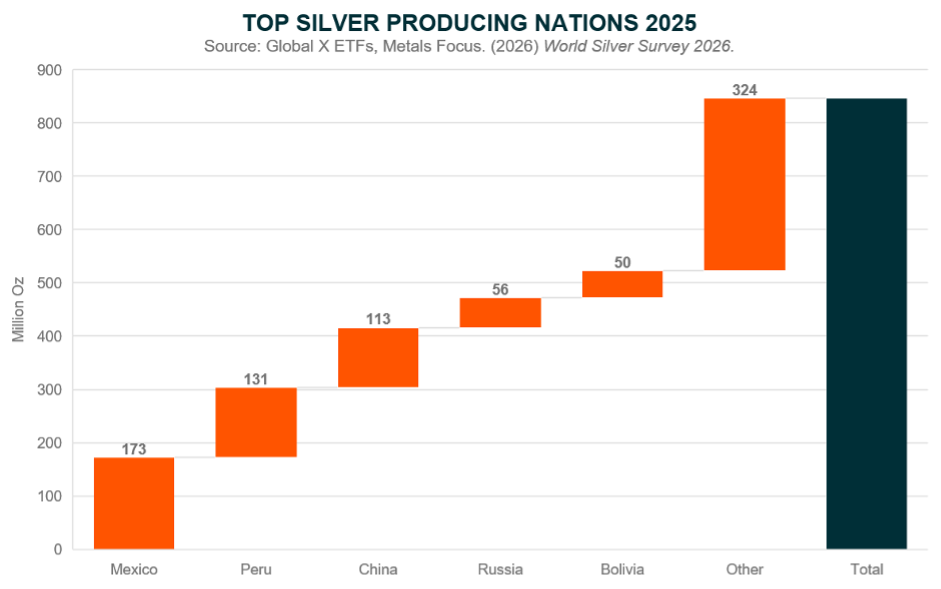

Silver can be found across many geographies, but approximately 50% of the world’s silver production is found in the Americas, with Mexico, Peru, and Chile supplying 42%. Outside of the Americas, the biggest producers are China, Russia and Bolivia, which together contribute to roughly 26% of the world’s production.3

How Is Silver Used?

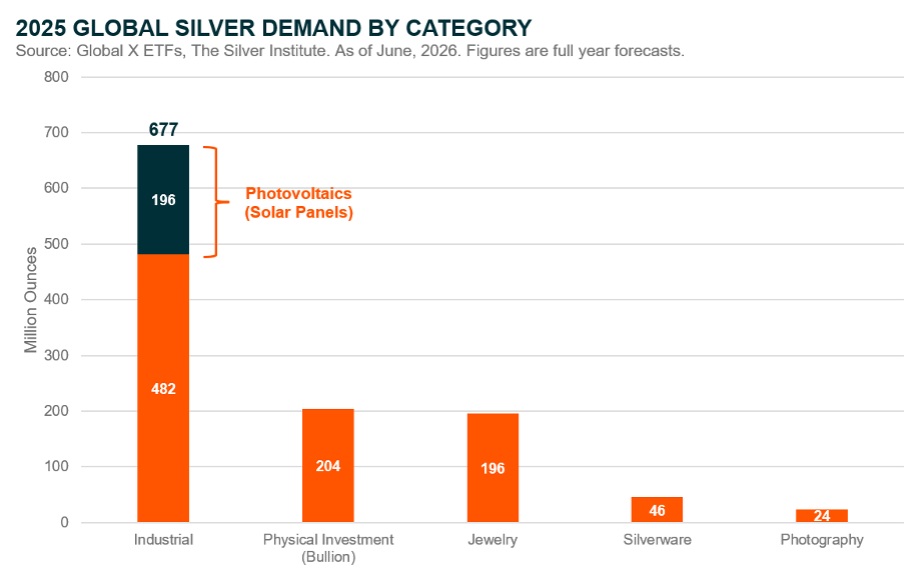

For centuries, silver was primarily used to craft luxury goods such as jewellery, tableware and fine art. This traditional use remains front of mind for many investors, who continue to value silver for its durability and collectability. As of 2025, these applications accounted for around 21% of annual silver consumption, while direct investment in the metal represented a further 18% of demand.4

While many investors recognise silver’s value as a precious metal, its significant industrial demand base is less widely understood. In fact, as industrial consumption has grown substantially in recent years, it now accounts for almost 60% of annual silver demand, making the metal as much an industrial commodity as a precious one.

This growth is underpinned by silver’s thermal and electrical conductivity, ductility, malleability and high reflectivity. Today, it is used extensively across a range of fast-growing technologies, including LED lighting, flexible displays, touchscreens, RFID tags, cellular technology and, most notably, solar panels. Its unique characteristics, combined with the relatively small quantities required in many applications, also make silver a sticky material input once embedded in technology supply chains.

How is Silver Different From Gold?

Silver and gold are often compared to each other as investment options, given their common classification as precious metals. However, the two offer highly differentiated exposures due to 1) Silver’s additional industrial usage and 2) their relative market sizes.

As discussed above, industrial use of silver has increased substantially and now accounts for the majority of demand. By comparison, only around 7% of gold demand is tied to industrial applications, with the remainder largely driven by jewellery, investment bars and central bank purchases.5 Gold is therefore more purely a precious metal, while silver prices are influenced by both precious metals sentiment and economic demand.

The two metals also differ significantly in market size. Silver remains a relatively niche investment, resulting in lower liquidity and a smaller overall market than gold. This tends to produce greater volatility and can occasionally lead to more extreme market dynamics, including supply squeezes.

What is The Relationship Between Gold and Silver?

Gold and silver have formed an iconic pairing for almost as long as human civilisation has existed. Throughout history, the two metals have almost always maintained some form of relative value, and this relationship remains relevant today.

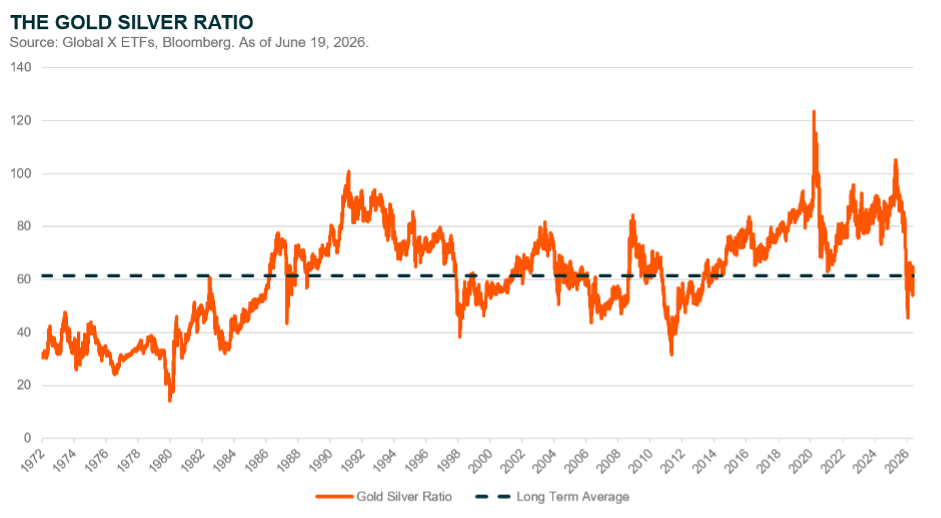

The gold to silver ratio, or GSR, measures how many ounces of silver are required to purchase one ounce of gold. By tracking the relative prices of the two metals, it can help investors identify when one appears unusually cheap or expensive compared with the other. Since the end of the Bretton Woods system and the resumption of open market gold trading, the ratio has averaged around 62.

The GSR is generally most useful at its extremes, when unusually wide valuation gaps have historically tended to narrow over time. One example occurred in April 2025, when the ratio reached 100, a historically rare level. Silver subsequently surged by more than 250% over the following 10 months as the valuation gap narrowed.6

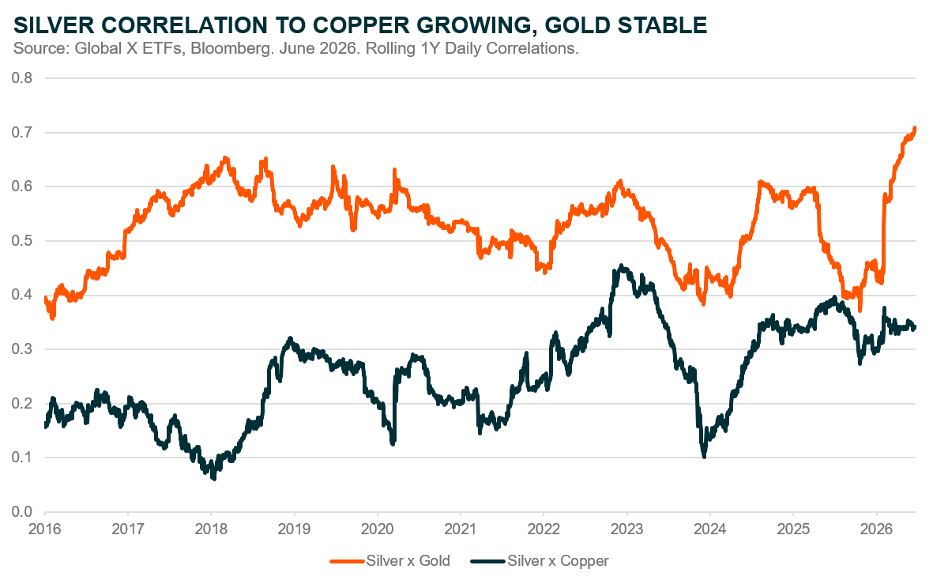

Despite these important differences, silver is still often viewed as a “second gold” because of its similar inverse relationship with real yields and the US dollar, as well as its role as a store of value. Historically, falling US real yields and a weakening US dollar have created a favourable environment for precious metals, including silver. However, over the past decade, silver has displayed a weaker negative correlation with US interest rates than gold, while its correlation with industrial metals has strengthened. This shift reflects silver’s growing industrial demand base and reinforces its unique position as both a precious and industrial metal, making it a potentially compelling addition to investment portfolios.

What Are Silver’s Supply and Demand Dynamics?

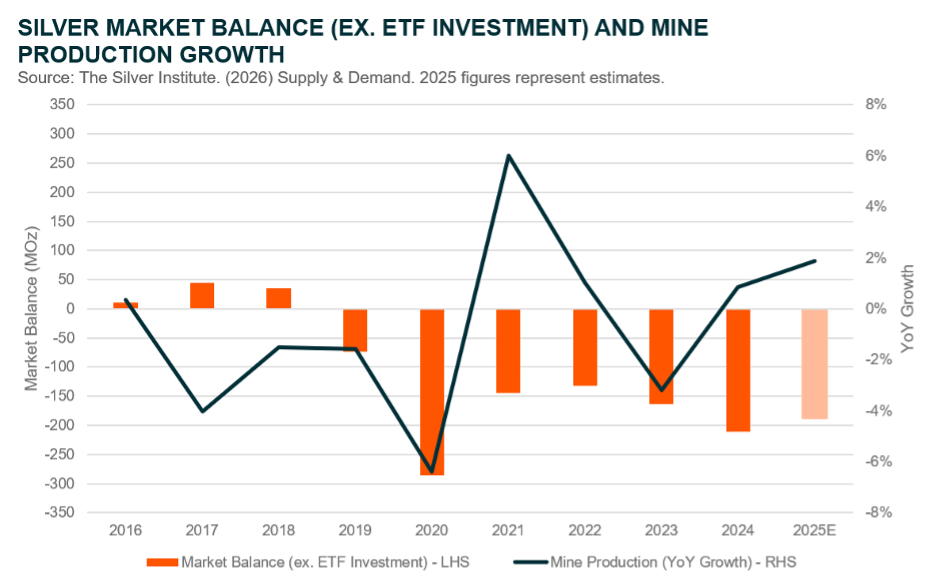

Global silver demand historically remained broadly aligned with supply. However, the market has since shifted into a persistent structural deficit, with demand consistently outpacing production. In 2026, the market is expected to record its eighth consecutive annual deficit.7

Much of this imbalance has been driven by rapidly growing photovoltaic demand. Silver consumption in solar panels reached 195.7 million ounces in 2026, almost four times the level recorded in 2010.8 Vehicle electrification and investment in power generation and distribution have provided additional sources of demand. Meanwhile, production growth has remained stagnant, with total silver supply declining by 27 million ounces over the past decade.

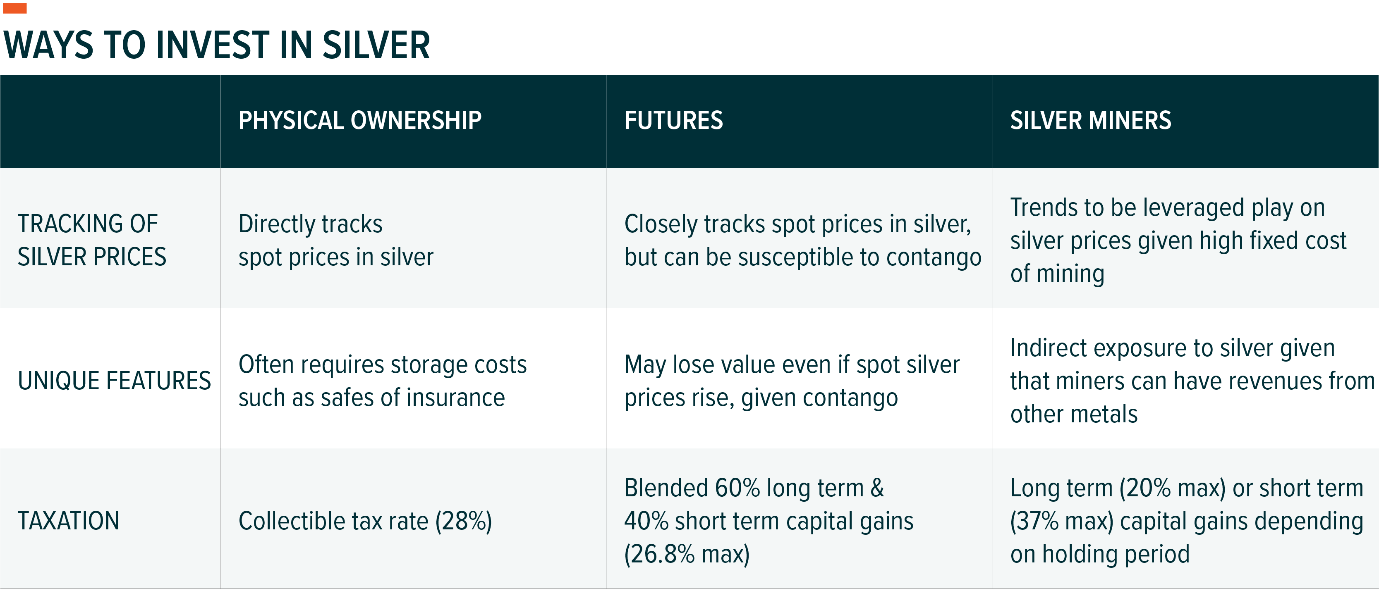

What Are the Differences Between Investing in Physical Silver, Futures, and Silver Mining Stocks?

1. Silver Mining Stocks

Silver mining stocks can offer indirect exposure to silver prices. These stocks tend to be leveraged plays on silver prices thanks to the operating leverage effect. Miners have relative fixed costs for extracting metal, allowing any increase (or decrease) in the underlying commodity owing to pass through almost directly into profit margins. Mining stocks are considerably more liquid than physical silver as they can be bought and sold on a stock exchange and during market trading hours. A potential drawback is that investors are exposed to idiosyncratic risks associated with owning the stock of a particular company, though this can be mitigated by investing via a silver miner targeted ETF.

2. Futures

Paper trading of silver is conducted through the futures market. Paper trading provides investors with exposure to silver without needing to physically hold the metal, potentially improving liquidity and reducing the cost of ownership. Unlike the bullion market, futures markets can also allow investors to use leverage. One downside of futures is contango, when future prices of a commodity are higher than their spot price. This can erode gains over time, even if the spot price of silver rises. The use of futures contracts is subject to market risk, leverage risk, and liquidity risk. They may experience losses that exceed losses experienced by securities that do not use futures contracts. The use of leverage may amply the effects of market volatility.

3. Physical Silver and ETFs

The most obvious way to gain access to silver price is to purchase silver bullion directly from precious metal dealers, who sell it at spot market prices. The advantage of physical ownership is that its value closely tracks the price movements of the broader silver market. However, dealers can charge premiums to buy and sell silver, which can dramatically reduce returns, and there are additional costs of storage, such as buying a safe or renting a safety deposit box that must be considered. This is where a physical silver ETF can offer several advantages. By utilising an ETF, investors gain access to institutional security and storage, as well as proper pricing at a low-cost and with high liquidity. Investing in a physical silver ETF provides all the advantages of owning physical silver and removes the majority of inconveniences. That said, silver itself remains a volatile asset, and an ETF does nothing to shield investors from the price swings that come with exposure to the metal.

Silver: The Best of Both Worlds

Silver is a unique metal because it has properties of both a precious and an industrial metal. We believe this makes silver a useful portfolio holding as it can potentially appreciate in both environments where demand for precious metals can rise, such as during periods of heightened volatility, as well as in eras of strong economic growth where industrial demand is expanding. For long term investors, Global X believes that allocating to physical silver can help provide a balanced approach to wealth preservation and capital appreciation.

Related ETFs

578A – Global X Silver ETF (JPY Hedged)

579A – Global X Silver Miners ETF

SIL – Global X Silver Miners ETF

Click the fund name above to view current performance and holdings. Holdings are subject to change. Current and future holdings are subject to risk.