Short- and Long-Duration Energy Storage Essential to the Clean Energy Transition

The adoption of renewable energy is accelerating globally, particularly wind and solar power, as governments and corporations work towards meeting climate change-related emissions reduction targets and boosting energy security. The International Energy Agency (IEA) forecasts renewables capacity growth will be 50% higher from 2021–2026 than 2015–2020.1 Despite this strong outlook, even faster renewable energy development will be required to reach global net-zero emissions by mid-century and keep global warming under 1.5˚C by 2100.2 In our view, the widespread adoption of energy storage systems is key to reaching the high levels of renewable energy generation required to reduce emissions within the power sector.

In this report, we explore how the global proliferation of renewable energy can drive rapid growth in energy storage over the coming years, with both short- and long-duration energy storage systems essential to the green energy transition.

Key Takeaways

- Energy storage capacity and generation are set to grow rapidly over the coming years, driven by the global proliferation of renewable energy, grid supply challenges, government support, and lower technology prices.

- We expect the rapid adoption of short-duration battery energy storage systems to create investment opportunities across the renewables and battery value chains, including renewables developers, storage system manufacturers, and miners of critical minerals.

- Growing government support for long-duration energy storage systems could support power grids while accelerating wind, solar, and hydrogen power development significantly. To reach net-zero power sector targets, the growth of these systems could represent a $1.5–3.0 trillion investment opportunity.3

A Successful Clean Energy Transition Requires Energy Storage Solutions

In 2021, renewable energy generation capacity grew by 9.1% to just under 3,065 gigawatts (GW).4 Globally, renewables accounted for 81% of all new capacity additions last year, driven by the wind and solar power sectors.5 We expect robust renewables’ growth to continue, with forecasts for capacity to reach 4,800GW by 2026.6 For context, 4,800GW is roughly equivalent to global fossil fuel and nuclear power capacity combined.7 In total, renewables are forecasted to account for 95% of all power capacity growth between 2022 and 2026.8

The robust growth outlook for renewable energy is due to several factors. Many governments are ramping up climate change mitigation efforts, including support for renewable energy adoption through tax credits, subsidies, and renewable project tenders and auctions. In the U.S., President Biden set a target for reaching a carbon pollution-free power sector by 2035.9 Also, corporations are seeking their own renewable energy supply to meet sustainability targets. In 2021, corporations procured 31.1GW of renewable energy globally via power purchase agreements (PPAs).10 The top three corporate clean energy buyers last year were Amazon, Microsoft, and Meta.11

In addition, technological advancements, including to wind turbines and solar modules, make wind and solar power increasingly cost-competitive with traditional power sources while boosting overall performance and efficiencies. Critically, energy storage system technologies are also improving and becoming more cost-competitive due to falling battery costs and increased government support in many countries, including the U.S. and China.12 Global energy storage is forecast to explode from 17GW/34 gigawatt hour (GWh) in 2020 to 358GW/1,028GWh in 2030, according to BloombergNEF.13 The U.S. and China appear set to be the largest energy storage markets, with India, Australia, Germany, Japan, and the U.K. also expected to see strong growth.14

The energy storage landscape includes short- and long-duration energy storage solutions. Short-duration energy storage (SDES), also known as short-term energy storage, is defined as any storage system that is able to discharge energy for up to 10 hours at its rated power output. Long-duration energy storage (LDES) is any system that is able to discharge energy at its rated power output for 10 or more hours.15 We expect both types of storage will be necessary to balance increasingly renewable power grids on hourly, daily, weekly, and even seasonal timescales.

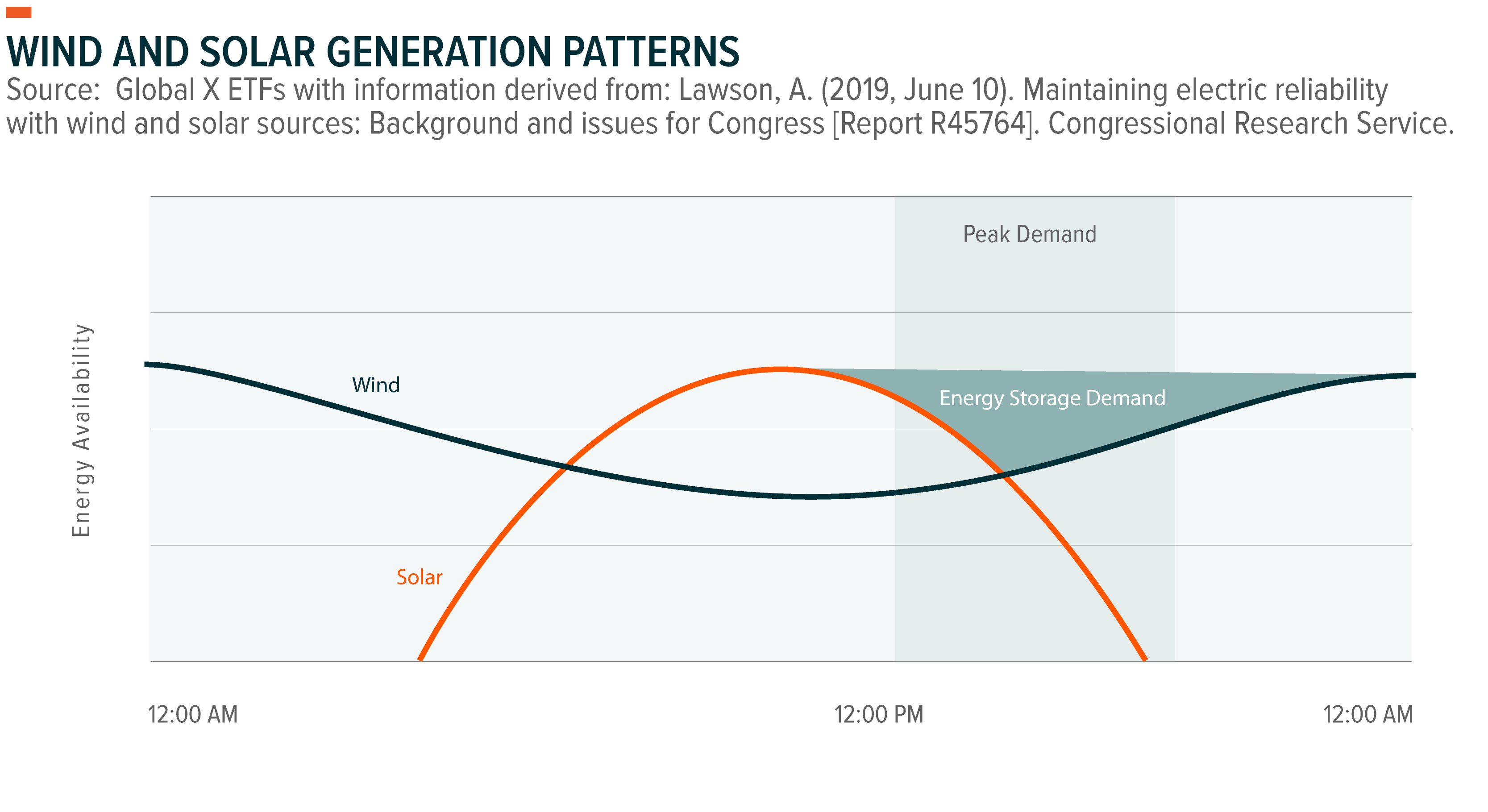

In our view, the widespread adoption of energy storage systems is essential for renewable energy to comprise high shares of the global power system, and the growing deployment of energy storage has the potential to accelerate wind and solar power growth. As intermittent power sources, wind and solar energy production often does not align with peak energy demand.16 The variability creates challenges for governments facing growing grid supply challenges, particularly amid increasing risks of extreme weather events that disrupt electricity production.17 In the U.S., the power crisis in Texas due to extreme cold temperatures in February 2021 and the risk of blackouts in California due to the prevalence of wildfires are two examples that highlight the importance of adopting grid-stabilizing technologies. Renewable energy paired with energy storage systems offers a potential solution.18

Growth in Battery Energy Storage Encompasses the Renewables and Battery Supply Chains

Battery energy storage systems (BESS) projects typically have short storage duration of 4–6 hours.19 BESS designs can use a variety of battery chemistries, including lithium-ion, nickel-based, sodium-based, and lead acid.20 However, lithium-ion systems dominate the space. Over 90% of installed energy storage capacity in the U.S. came from lithium-ion systems as of year-end 2019, similar to the rest of the world.21,22

Lithium-ion BESS are expected to continue to dominate the energy storage market globally over the coming decade due to their increasing cost-competitiveness and established supply chain.23 Given the strong growth outlook, the global battery energy storage market could grow from $10.9 billion in 2022 to $31.2 billion by 2029. For the full decade, the battery energy storage market could grow at 16.3% compound annual growth rate (CAGR).24

The growing BESS market creates opportunities for renewables project developers. Leading renewables developers such as NextEra Energy Resources, Enel Green Power, AES Corp, and Vistra Corp. are rapidly expanding their battery energy storage project pipelines.25 Notable operational projects include the 409MW/900 megawatt hour (MWh) Manatee Energy Storage Center from Florida Power & Light, a regulated utility of NextEra, and the 400MW/1,600MWh Moss Landing Energy Storage Facility by Vistra in California. The two projects are among the largest BESS in the world.26 Vistra plans to expand Moss Landing with an additional 350MW/1,400MWh battery system.27

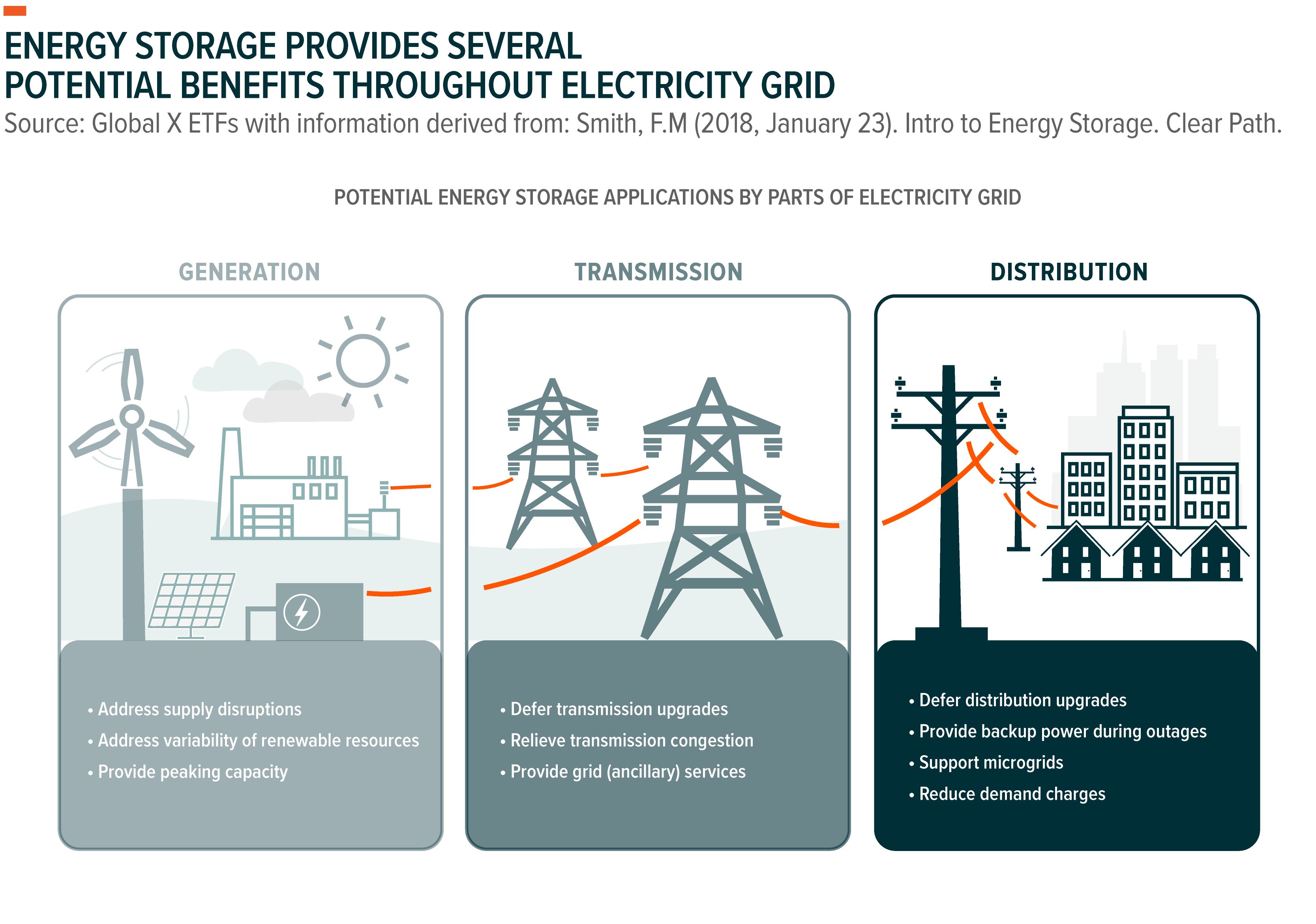

Renewables developers could find additional wind and solar development opportunities as energy storage scales, with energy storage being a potential solution for insufficient and congested transmission and distribution infrastructure.28 Notably, energy storage systems offer several potential benefits including enhancing grid reliability, deferring transmission upgrades, and relieving transmission congestion.29,30 A lack of transmission or congested lines are a primary barrier to widespread renewables development in many countries, including the U.S. and Chile.31,32

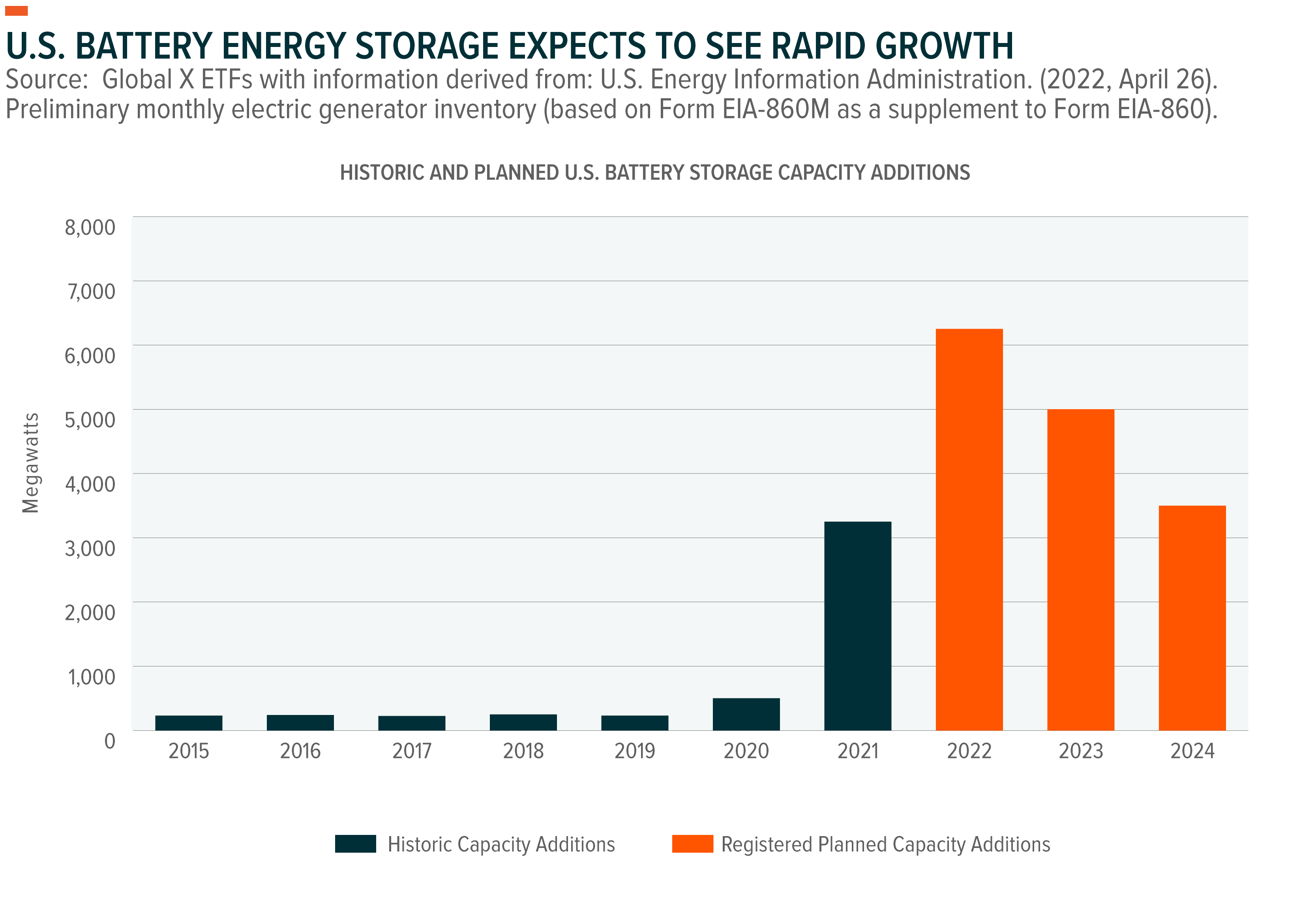

As a result, renewable energy developers are increasingly pairing wind and solar projects with BESS projects to create hybrid power systems. Of the 14.5GW of battery storage capacity registered as of year-end 2020 to come online in the U.S. through 2024, 63% are set to be co-located with solar power projects and an additional 9% with wind power projects.33 Hybrid renewables plus storage projects have the potential to reduce upfront transmission upgrade and interconnection costs, reduce how much electricity production is curtailed in times of oversupply, and expand the time window in which a project can send electricity to the grid.34

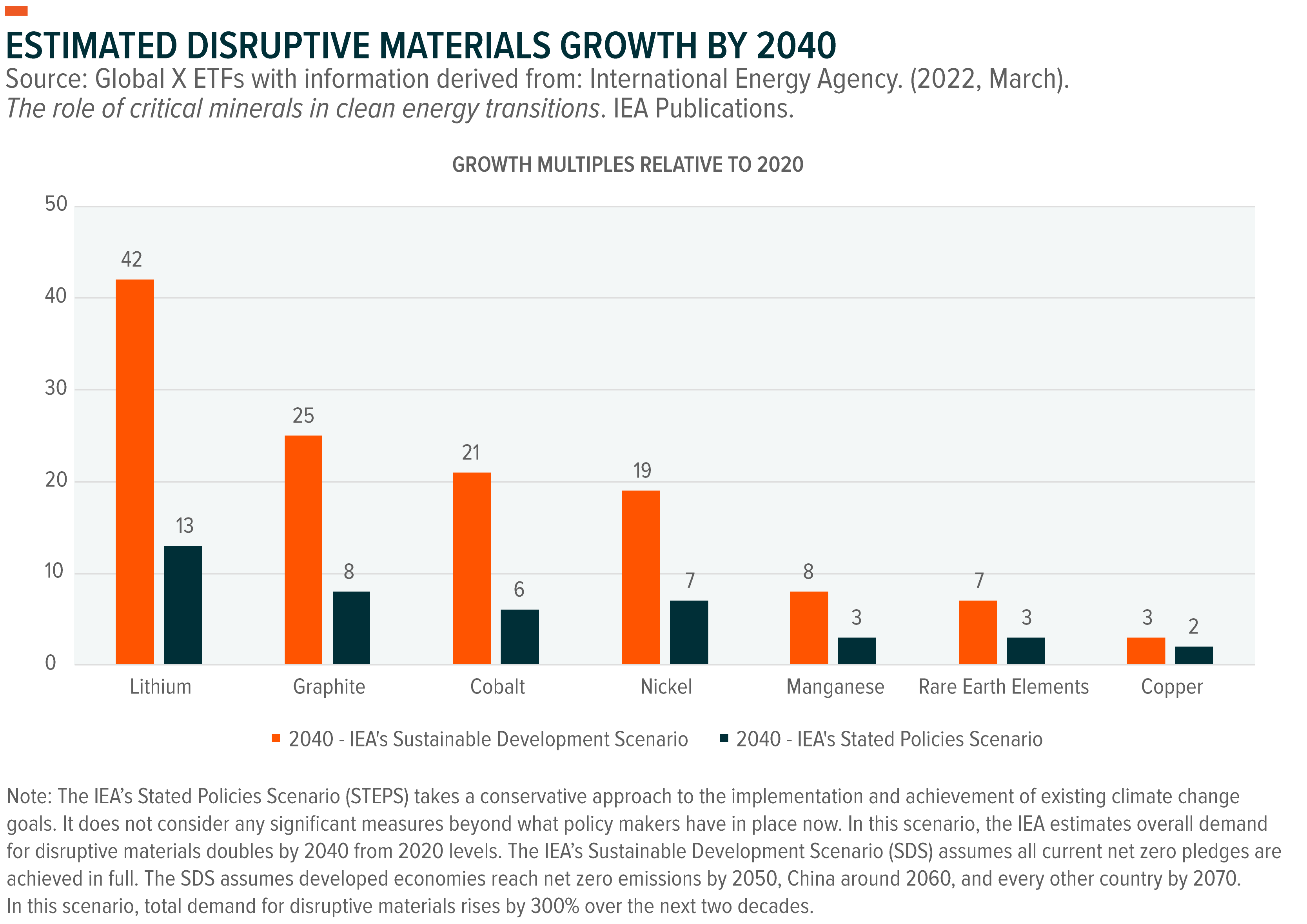

The rapid uptake of BESS can also create opportunities across the battery energy storage supply chain. Leading battery energy storage system manufacturers, including Tesla and Fluence Energy, a joint venture between Siemens and AES Company, reported strong demand through Q1 2022.35,36 Fluence Energy added 600MW in energy storage project orders, a 525% increase compared to Q1 2021.37 Energy storage growth could also increase demand for miners of lithium and other critical minerals, including copper, cobalt, nickel, and rare earth elements. Depending on rate of growth in clean energy technologies such as electric vehicles and energy storage, lithium demand could be 13–43 times higher in 2040 than 2020. Cobalt and nickel demand could be around 6–20 times higher.38

Development of LDES Systems Has Newfound Momentum

Long-duration energy storage systems offer stable energy output ranging from 10 hours to days, weeks, and even seasons, providing enhanced grid reliability compared to short-duration energy storage systems.39 LDES systems have been around for decades, most notably in the form of pumped storage hydropower systems. However, cost, permitting, and technological barriers, in addition to a lack of regulatory support, prevented LDES systems from widescale adoption.40,41

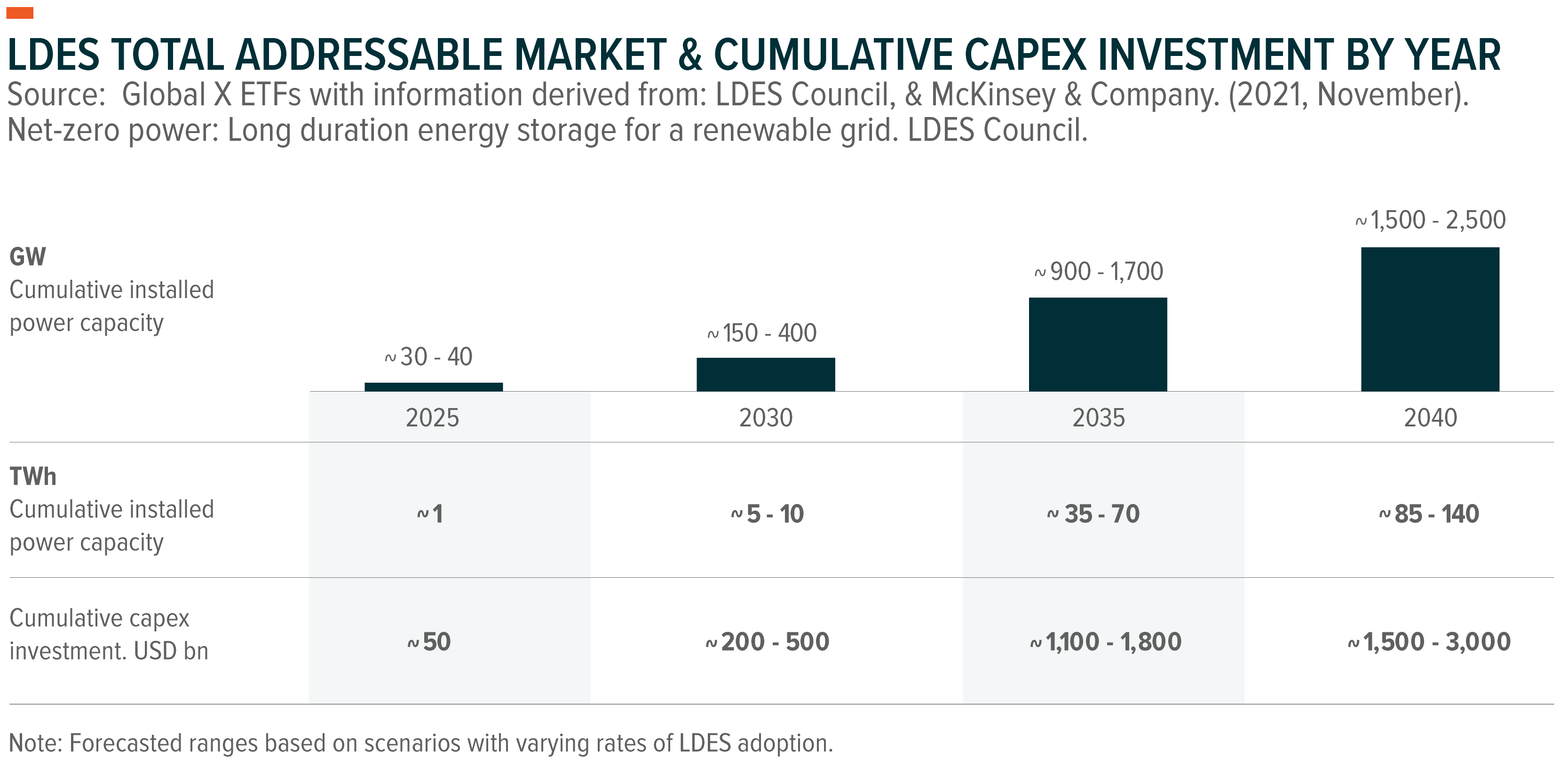

We expect that to change, though, as significant growth opportunities for LDES technologies emerge. To reach a global net-zero power sector targets, LDES must be scaled up by an estimated 400 times from present-day levels to 85–140TWh by 2040.42 This scale-up equates to a $1.5–3.0 trillion investment opportunity.43 Government interest in LDES systems is growing, including in the U.S. In July 2021, the U.S. Department of Energy announced an initiative called the Long Duration Storage Shot, which seeks to reduce costs for LDES by 90% by 2030.44

We expect that growth in LDES systems can also create investment opportunities in renewable energy. Similar to BESS, LDES systems could help unlock the potential of wind and solar power in power generation, particularly as renewables begin to reach 60–70% market share.45 Further grid stabilization could make renewables a more suitable option that compares to traditional stable baseload power sources such as natural gas, coal, and nuclear.

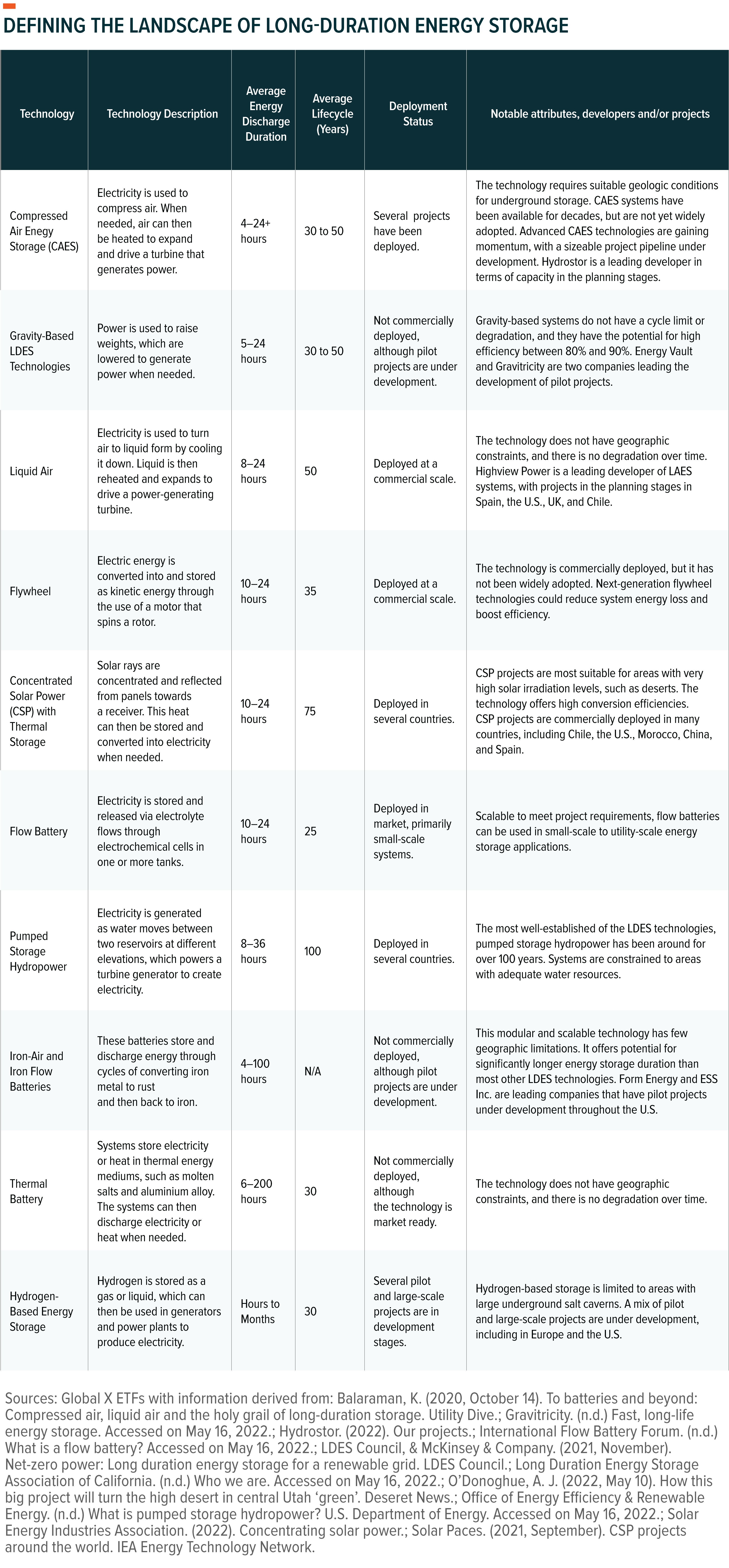

In addition, the need for LDES systems presents a sizeable use case for hydrogen, particularly green hydrogen. As the table below shows, hydrogen-based energy storage has the potential to store power for weeks to months, so these projects could be used to account for seasonal differences in electricity production.46 Power-to-hydrogen-to-power industrial scale projects are still in the very early stages of development. That said, pilot projects are expected to come online over the next few years, including the 12MW HYFLEXPOWER project in France.47

Similar to hydrogen-based storage, most other LDES technologies are also in the early stages of adoption. The types of LDES systems that we expect to take off at a commercial scale include compressed air energy storage, liquid air energy storage, non-lithium-ion batteries, and hydrogen-based energy storage systems. The adoption of these technologies is expected to vary due to location suitability and cost constraints.

Conclusion: Energy Storage Plus Renewables Creates Opportunities

Renewable energy sources, primarily wind and solar power, are set to account for the majority of growth within the power sector over the coming years. But to take full advantage of this potential growth requires reliable energy storage systems that can bolster energy grids already under pressure from increasing variability and climate change. We expect investment opportunities to materialize across the renewables and battery energy storage value chains, including miners of critical minerals, manufacturers of BESS technologies, and renewables developers. Longer-term, we expect the potential that long-duration energy storage systems hold to finally gain traction, accelerating opportunities in the renewables, energy storage, and hydrogen spaces.

Related ETFs

CTEC: The Global X CleanTech ETF seeks to invest in companies that stand to benefit from the increased adoption of technologies that inhibit or reduce negative environmental impacts. This includes companies involved in renewable energy production, energy storage, smart grid implementation, residential/commercial energy efficiency, and/or the production and provision of pollution-reducing products and solutions.

RNRG: The Global X Renewable Energy Producers ETF seeks to invest in companies that produce energy from renewable sources including wind, solar, hydroelectric, geothermal, and biofuels.

WNDY: The Global X Wind Energy ETF seeks to invest in companies positioned to benefit from the advancement of the global wind energy industry. This includes companies involved in wind energy technology production; the integration of wind into energy systems; and the development/manufacturing of turbines that harness energy from wind and convert it into electrical power.

RAYS: The Global X Solar ETF seeks to invest in companies positioned to benefit from the advancement of the global solar technology industry. This includes companies involved in solar power production; the integration of solar into energy systems; and the development/manufacturing of solar-powered generators, engines, batteries, and other technologies related to the utilization of solar as an energy source.

LIT: The Global X Lithium & Battery Tech ETF invests in the full lithium cycle, from mining and refining the metal, through battery production.

DMAT: The Global X Disruptive Materials ETF seeks to invest in companies producing metals and other raw materials that are essential to the expansion of disruptive technologies, such as lithium batteries, solar panels, wind turbines, fuel cells, robotics, and 3D printers. Targeted materials include companies involved in the exploration, mining, production and/or enhancement of Rare Earth Materials, Zinc, Palladium & Platinum, Nickel, Manganese, Lithium, Graphene & Graphite, Copper, Cobalt & Carbon Fiber.

HYDR: The Global X Hydrogen ETF seeks to invest in companies that stand to benefit from the advancement of the global hydrogen industry. This includes companies involved in hydrogen production; the integration of hydrogen into energy systems; and the development/manufacturing of hydrogen fuel cells, electrolyzers, and other technologies related to the utilization of hydrogen as an energy source.

Click the fund name above to view current holdings. Holdings are subject to change. Current and future holdings are subject to risk.