Lithium and EV Market Update: Slower-Than-Expected Sales Growth Just a Bump in the Road

Electric vehicle (EV) sales doubled globally between 2020 and 2021 and increased by another 60% in 2022 as it became clear that the future of transport is electric.1 Supportive government policy, improving technology, charging station deployment, and commitments from traditional automakers contributed to the rapid transition toward EVs. Such a shift left lithium miners scrambling to increase capacity, a process that can take anywhere between 5 and 25 years.2 As a result, lithium prices surged more than 150% in 2022, well above previous all-time highs.3

It wasn’t the same story in 2023, as lithium prices softened due to slower-than-expected EV sales growth, which we attribute to market dynamics in China and elevated costs for consumers. Despite the detour, EV adoption remains brisk, and we maintain our conviction in the specialty chemical that has been dubbed “white gold.”

Key Takeaways

- Global EV markets got off to a slow start in 2023, but they continued to demonstrate strong sales growth under more challenging conditions than in years past.

- Battery makers took the opportunity to destock inventories, which caused lithium prices to fall through most of 2023.

- Recent EV sales growth and lithium price trends do not compromise the core pillars that support EV adoption, and the outlook remains strong for suppliers of the EV revolution.

EV Sales Growth Slower, Not Moving in Reverse

EV and battery market research firm Rho Motion expects global EV sales to total just under 14 million units and grow by more than 30% in 2023, down from a forecast closer to 40% growth at the beginning of the year.4,5 We view China’s struggles in moving on from pandemic policies as one of the most important stories for the EV space in 2023 and a key driver of this downward revision, albeit to still-strong growth.

The uncertain economic backdrop and the phase down of direct subsidies on EV purchases at the end of 2022 weakened sales in China, especially in Q1. Given that China is forecast to account for almost 60% of global EV sales in 2023, its underwhelming performance reverberated throughout supply chains and impacted investor sentiment toward the broader electrified mobility ecosystem.6

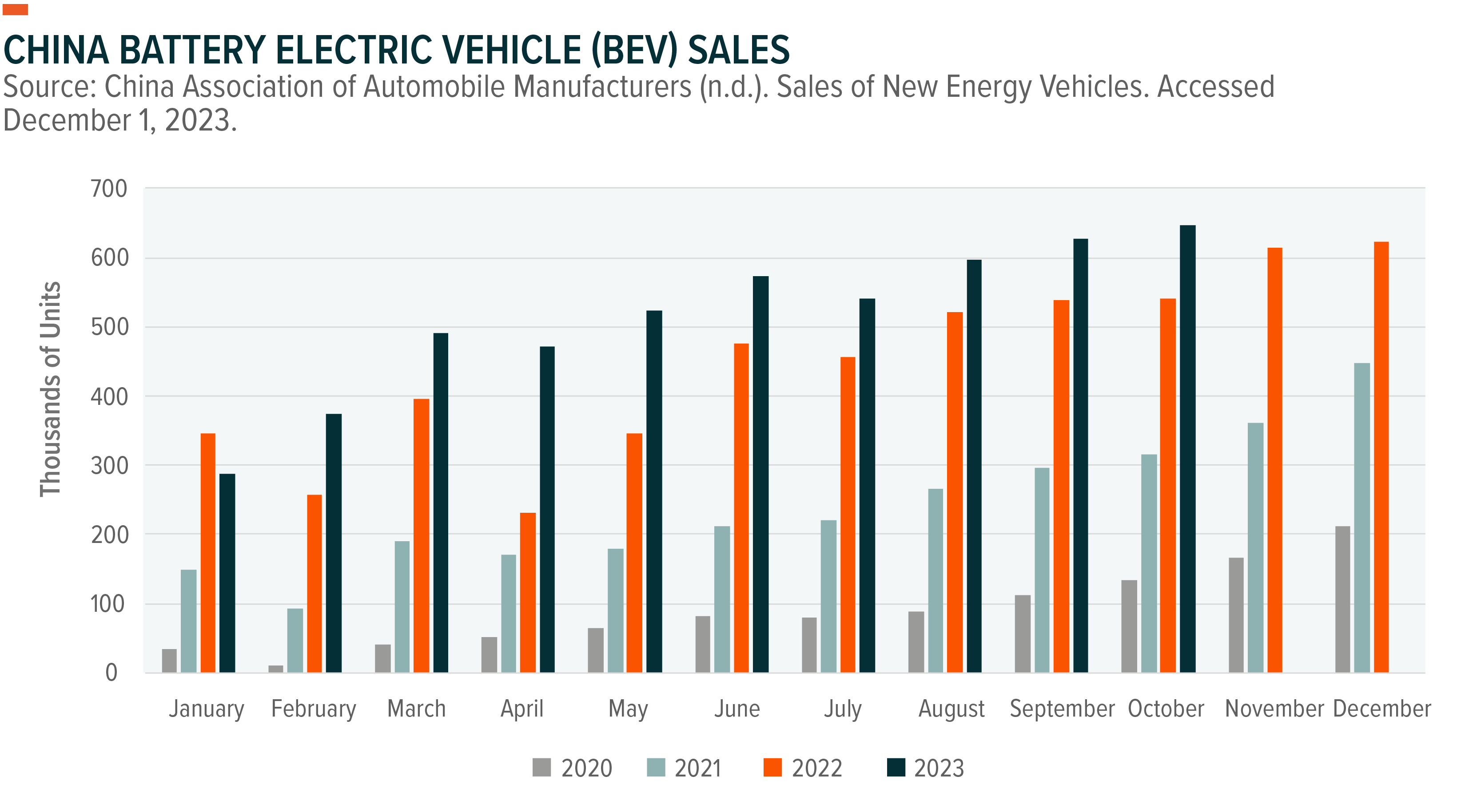

Despite these headwinds, China’s EV market is still growing. Battery electric vehicle (BEV) sales through the end of Q3 were up 26% relative to the comparable period in 2022.7 Hybrid sales were up 87%.8

Elsewhere, U.S. EV sales growth remained strong. According to Kelley Blue Book, volumes reached 313,086 units in Q3, up 50% year over year (YoY) and 5% quarter over quarter.9 Sales through September reached just over 873,000 units, putting the United States firmly on track to surpass 1 million in annual sales for the first time.10

Higher borrowing costs were a notable consideration for consumers. In Q3, the average APR on loans for new vehicles in the United States was 7.4%, a nearly 30% YoY increase.11

The combination of inflation and rising interest rates have consumers less inclined to purchase more expensive versions of products and services, and vehicles are no exception. EV costs declined dramatically in recent years, but still sell at a transactional premium to conventional vehicles. The average price paid for an EV in the United States in September 2023 was $50,683, down 22% from the year prior but still about 6% higher than average price paid for a new vehicle overall during that period.12

Lithium Prices Retreated from All-Time Highs, Fundamentals Intact

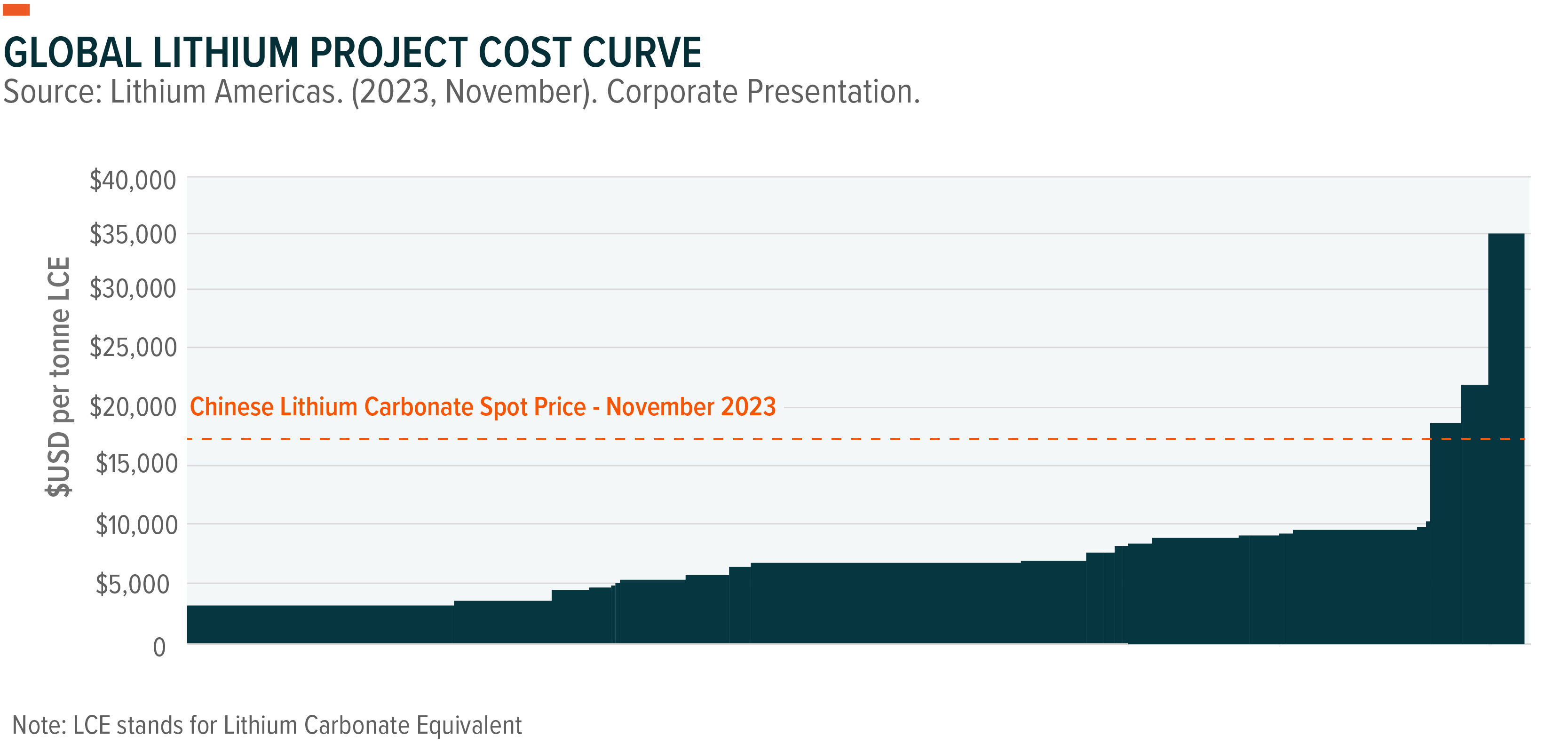

After surging past record after record in 2022, lithium prices cooled in 2023. The global lithium price index maintained by Benchmark Mineral Intelligence was down 70% at the end of November.13 At the end of November, Chinese lithium carbonate traded for about 17,000 USD per tonne compared to a peak of about 81,000 USD per tonne in November 2022.14

Several factors played into these prices declines. The phasedown of subsidies in China at the end of 2022 pulled forward demand and exasperated EV sales’ typical seasonal trends. Historically, Q1 is the weakest quarter for EV sales and Q4 is the strongest. As a result of policy changes and a continuation in Q1 weakness, BEV sales in China decreased by 18% YoY in January 2023 and 54% from December 2022.15 As of the end of Q3 2023, January was the only month of the year where Chinese BEV sales declined compared to the year prior.16

China’s slow start to 2023 enabled battery makers to begin working through lithium inventories that were stockpiled in previous years and forgo large additional purchases. This dynamic coupled with new lithium capacity coming online in regions such as Australia, China, Argentina, and Brazil compressed lithium prices.17

Large lithium supply deficits in 2022 were a function of years of EV sales momentum that suppliers were not able to keep up with given the timelines and degree of difficulty associated with bringing different resources to market. Heading into 2023, prices were expected to moderate from 2022 levels, though the magnitude of volatility caught industry participants by surprise. On Albemarle’s November Q3 earnings call, President of Energy Storage Eric Norris remarked that given the strong fundamentals behind the market, he was “a little bit perplexed as to why price is where it is.”18

Heading into 2024, lithium prices remain meaningfully higher compared to history and are supportive of miner profitability. For most projects today, break-even is 5,000–8,000 USD per tonne, well below current market prices.19

Lower material input prices could also usher in healthier cost dynamics for the EV space. After increasing in 2022, lithium-ion battery costs are likely to come down again for 2023, which could translate into more affordable EVs. Benchmark Mineral Intelligence’s NCM High Nickel Index is down 53% year-to-date and its LFP Index is down 73%, suggesting that falling prices for lithium along with nickel, cobalt, and manganese translated into falling cathode prices.20,21

We Believe the Future Is Still Electric

Uncertainty remains in the short term, especially in China, but the pillars that have supported EV adoption in recent years are intact. We expect government policies, improving cost dynamics, a proliferation of charging infrastructure, and normalization of EVs as an emergent technology to continue to support growth. According to the International Energy Agency (IEA)22, EVs are one of only three clean technologies on pace to allow the world to reach net zero emissions by 2050.23

Further positives for the space could come in the form of an emerging suite of technologies that may be primed to address current limitations of EVs and bolster adoption. Next-generation battery technologies such as solid-state are expected to improve range, charging time, safety, and affordability of EVs and are already being developed by traditional automakers. Widespread solid-state commercialization is unlikely to begin until the end of the decade, but early iterations of this technology are already available to consumers.24 In July 2023, Chinese electric automaker Nio shipped the first ES6 SUVs with a 150 kilowatt-hour (kWh) semi solid-state battery pack that can support a range of 578 miles on a single charge.25

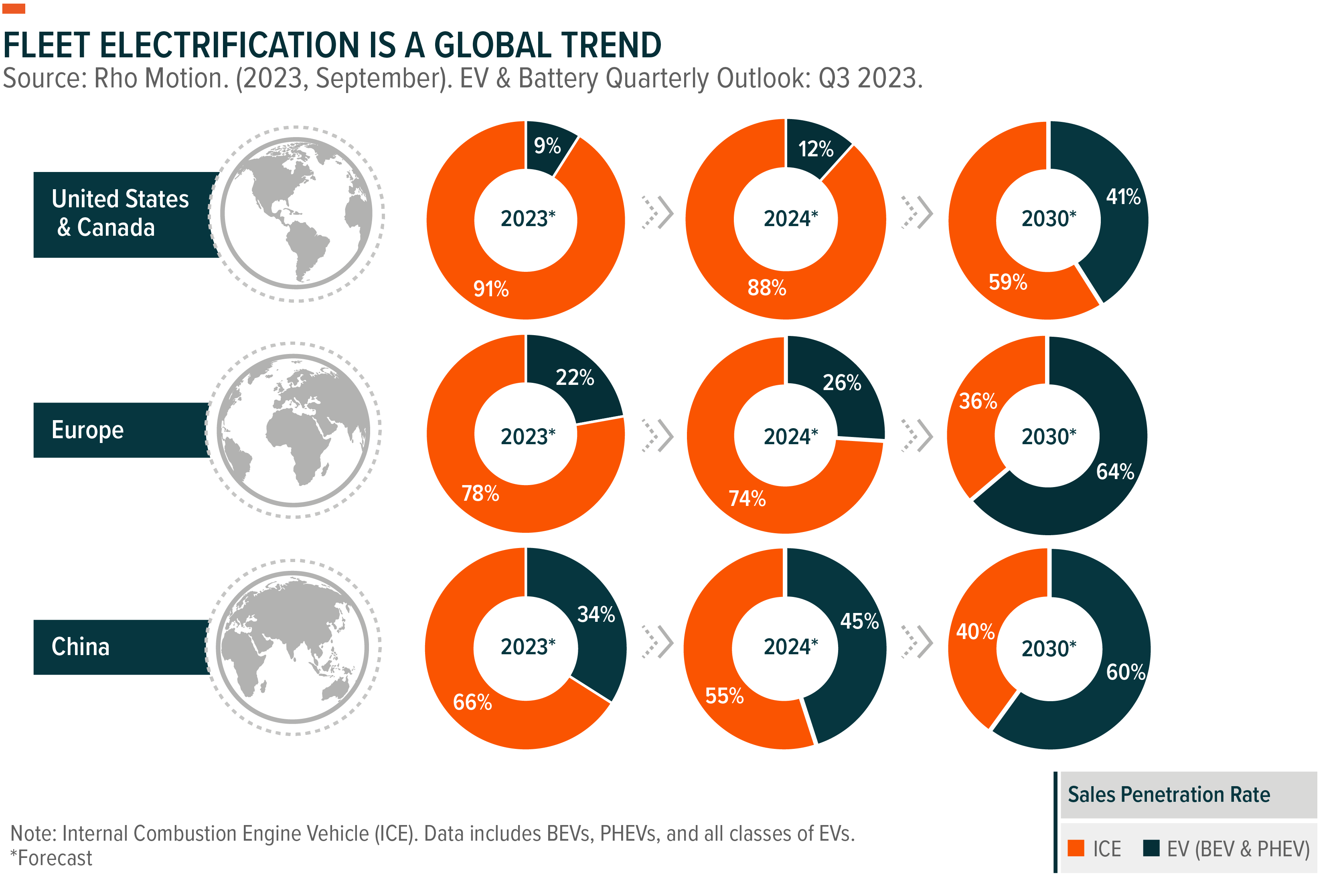

It is also important to note that although EV sales surged in recent years, the theme remains in the early stages of adoption. EV sales are likely to account for just 17% of global light-duty vehicle sales in 2023.26 Between 2022 and 2035, global EV sales are forecast to grow at a compound annual growth rate (CAGR) of 15.5% and account for more than 60% of annualized overall vehicle sales by the end of that period.27

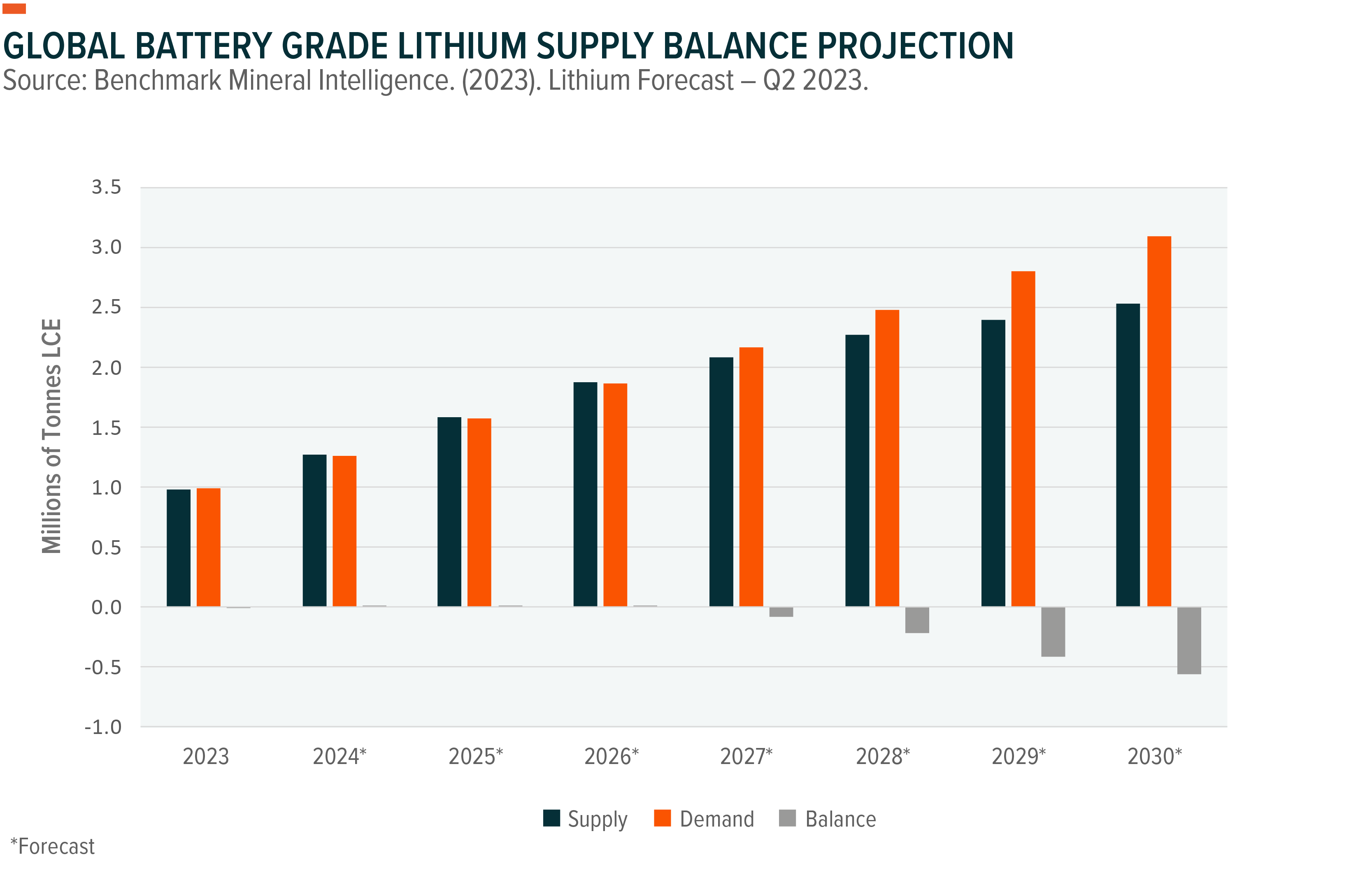

The lithium market is forecast to remain tightly balanced over the next several years until meaningful deficits arise again in 2027, coinciding with an expected expansion in EV penetration.28 Lithium spot prices may find support in the near term from thinning battery maker inventory levels and production curtailment for lithium projects at the highest end of the cost curve.

The forecast for near lithium supply equilibrium in the coming years is likely to be a delicate one. Delays to major projects in the space could quickly shift the market to deficit and introduce new upward pressure on prices.

Conclusion: The EV Growth Story Set to Continue

The EV industry encountered some bumps in the road in 2023 that also impacted upstream suppliers. However, the theme continued to grow, and the narratives behind the EV revolution are mostly unchanged. The EV industry may be moving into its next chapter as part of its maturation, but the technology remains in its early stages of adoption. In our view, the EV industry and adjacent lithium & battery tech companies have a long runway for growth ahead.

Related ETFs

LIT – Global X Lithium & Battery Tech ETF

DRIV – Global X Autonomous & Electric Vehicles ETF

Click the fund name above to view current holdings. Holdings are subject to change. Current and future holdings are subject to risk.