Inflection Points at Mid-Year: Favorable Winds, Choppy Seas

“Be as thou wast wont to be. See as thou wast wont to see.”

— William Shakespeare, A Midsummer Night’s Dream

Just as there is at the end of Shakespeare’s famous whimsical comedy, there’s much to reconcile in financial markets halfway through 2024, both what has been and what we expect to see. At the start of 2024, we expected economic growth to slow, the consumer to moderate, inflation to stay above target, and rates to remain elevated for longer.1 That scenario has largely played out, but core economic factors like labor, leverage, and liquidity are still near historically strong levels.2 In our view, U.S. economic growth may well surprise to the upside on stronger-than-expected corporate investment along with margins that can continue to expand in the coming quarters.

Our base case is built on the belief that a multi-year secular transition in automation and digitalization is challenging conventional economic thinking and quietly powering growth and market values. Markets do not go up in a straight line, and an economic hiccup or geopolitical challenge could put pressure on risk assets. Nonetheless, our bullish narrative on risk assets, equities, and a series of mature growth themes remains intact.

Key Takeaways

- The consumer is expected to slow, but labor, leverage, and liquidity remain strong, helping to explain the equity market’s advance thus far in 2024 and the potential for further gains.

- Three considerations for the second half of the year:

- Stronger corporate investment can help U.S. growth beat expectations yet again.

- Higher profit margins for S&P 500 companies could be the new normal.

- Geopolitical challenges may drive market volatility more than monetary policy.

- Consider opportunities tied to the AI ecosystem like AI developers and data centers, themes tied to geopolitical risk like U.S. Infrastructure and Defense Tech, and hedged equity exposure.

The 3 Ls Give a Clean Bill of Economic Health

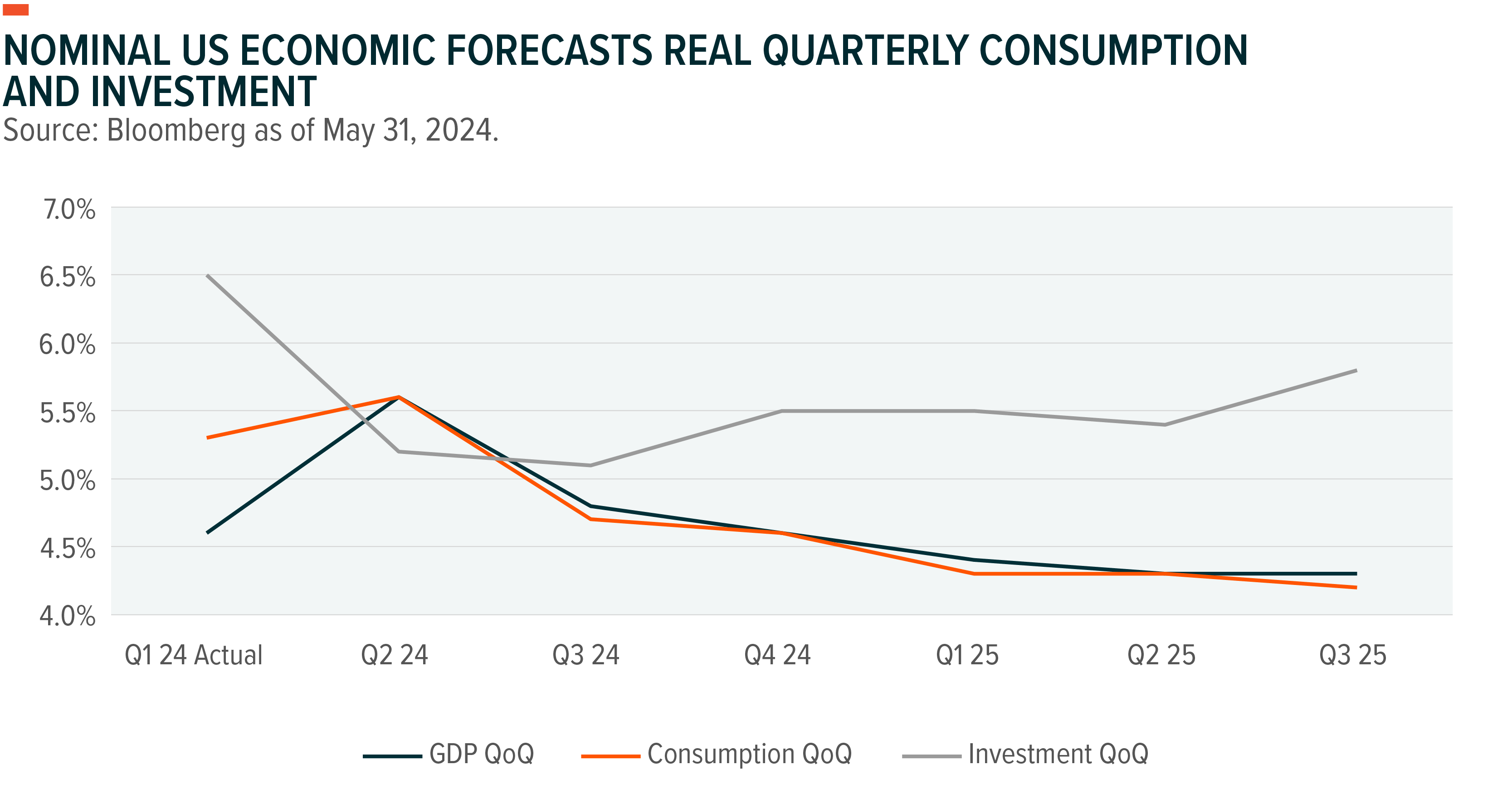

The U.S. economy seems healthy at the mid-year mark. There are some cautionary signs worth watching, but nominal growth at an annual clip of 5.4% is worth celebrating. Concern over a slowing consumer is warranted, but that is already baked into consensus economic forecasts.3

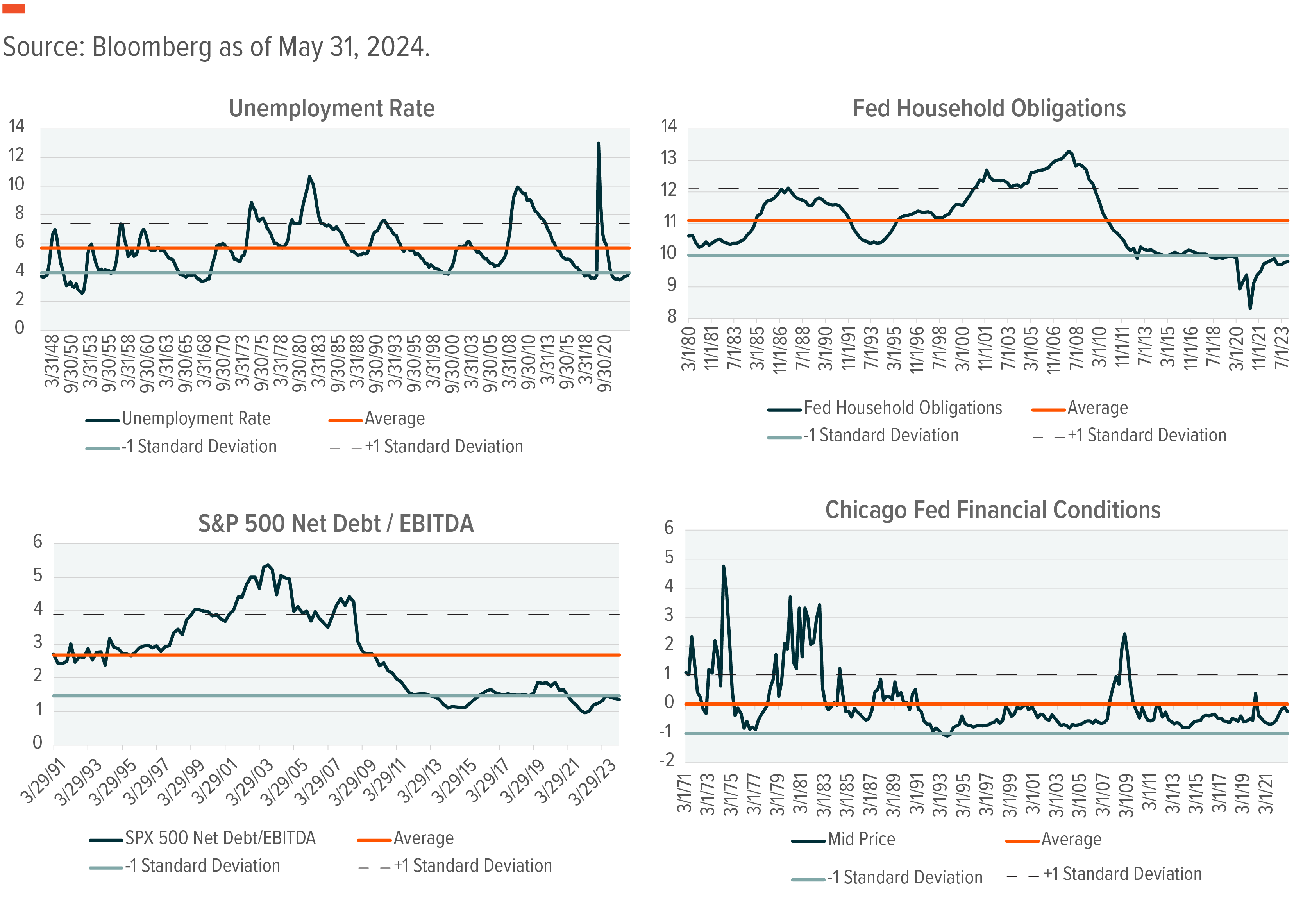

For the U.S. economy to have a meaningful slowdown and enter a recession, usually one or more of the 3 Ls deteriorate rapidly. The economy typically hums along when labor, leverage, and liquidity are all sound, and at present all three suggest that the economy is healthy and perhaps even strong. The unemployment rate ticked up to 4.0% in May from 3.7% at the start of the year, but this modest increase does not seem like cause for concern, especially considering that the long-term average is 5.7%.4

Household leverage, measured by monthly debt obligations relative to income, has declined since the Great Financial Crisis.5 Obligations improved further during COVID when homeowners refinanced at low rates and used stimulus to pay down existing debt. Despite potential consumer slowdown, the debt burden remains manageable and one standard deviation below normal. Corporate leverage also remains below long-term average.6

Financial conditions and liquidity may be the most interesting of the 3 Ls. Despite a 5.5% fed funds rate, U.S. financial conditions have loosened since March 2023.7 Real wage increases for low-income labor and elevated stock markets have added liquidity despite the Fed’s attempt to tighten. If conditions stay loose, this could be the first time since 2000 that the Fed begins a cutting cycle with favorable financial conditions.

Where the Puck Is Going

Three areas could prove particularly critical for markets in the second half of 2024.

Regime Rewind Leads to Higher Growth

The low-growth regime that lasted from 2001 to 2019 might be coming to an end, which would be worthy of a midsummer party. For almost 20 years, U.S. nominal GDP growth averaged just 4.0%, a major downshift from the 6.4% rate from 1983 to 2000.8 Since Q1 2020, growth has averaged 6.3%. This revitalized growth level may stem from residual COVID effects, but may also signal a shift to sustained higher growth and rates.

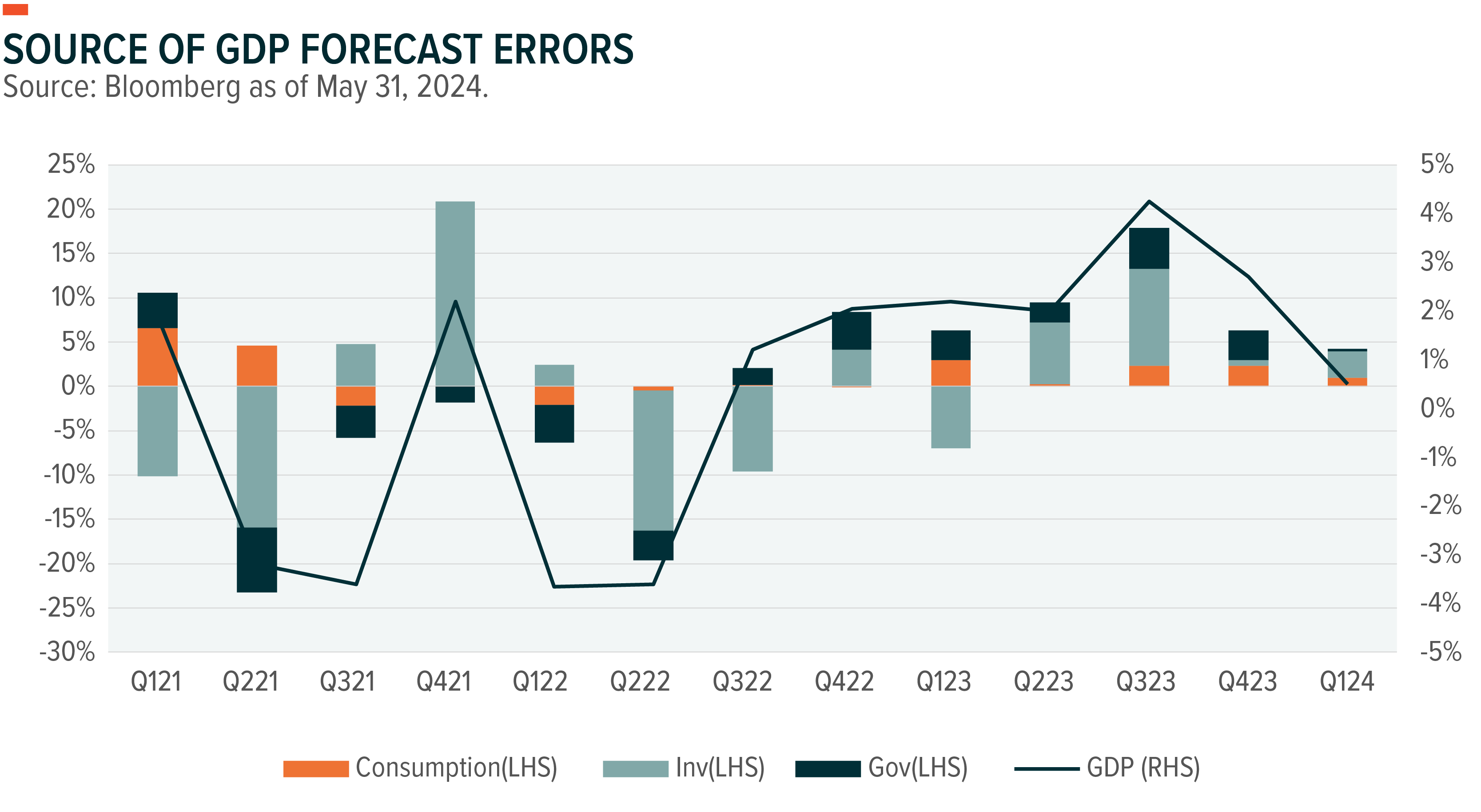

Corporate investment could well be the long-lost ingredient. Companies essentially stopped investing in the 20-year period following the dotcom bust.9 Capital expenditure growth was anemic and stagnant. Over the past four years, corporate investment returned in a big way. For 10 straight quarters ending in Q3 2023, companies grew investment by double digits and, in most quarters, faster than earnings.10 GDP forecasts have regularly missed the mark over the past few years, with the largest culprit being economic prognosticators underestimating the impact of renewed corporate investment.

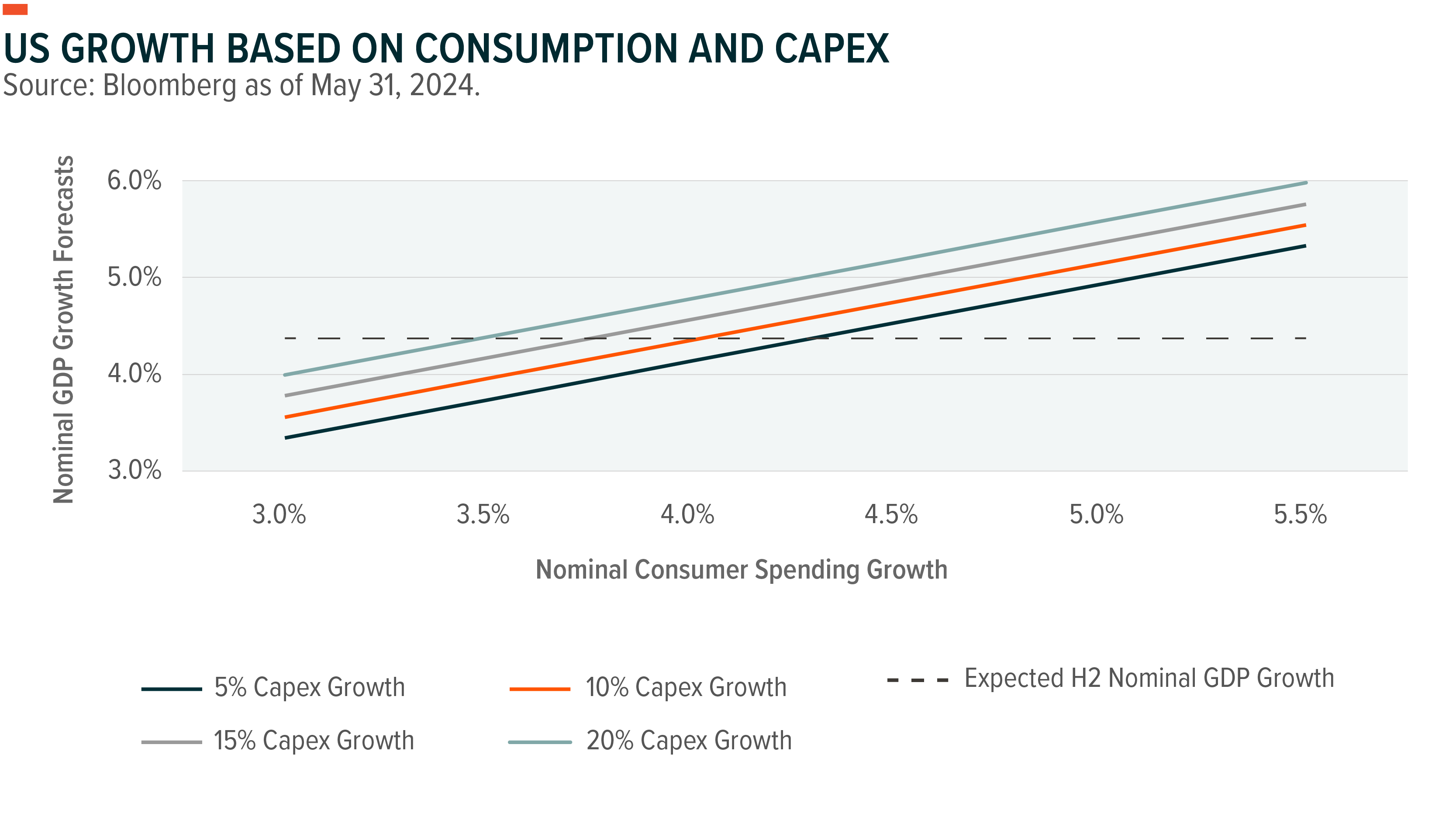

Capex typically follows return on capital (ROC). When ROC is high, companies can expect greater benefits from reinvesting in their business. There is a strong correlation. When ROC rises by 1%, companies increase their capex by 4.7% on average.11 Currently, ROC is running about 2.5% above the long-term average of 7.9%. That 2.5% increase in ROC could translate to an increase in capex of more than 10%, and current expectations may be underestimating investment in the second half of the year.

Examining consumption and capex growth shows the increasing importance of corporate investment. The consumer has long been the economy’s most important driver, but the impact of investment has added significance now. From 1997 to 2014, a 1% increase in investment was associated with a 0.22% increase in growth.12 Since then, that relationship has almost doubled to 0.43%. We use this 0.43% to model potential scenarios, and based on the consensus forecasts above, we find that capex growth above 10% would generate growth that beats current expectations. This scenario seems attainable and is our base case.

Corporate Profitability Keeps Leveling Up

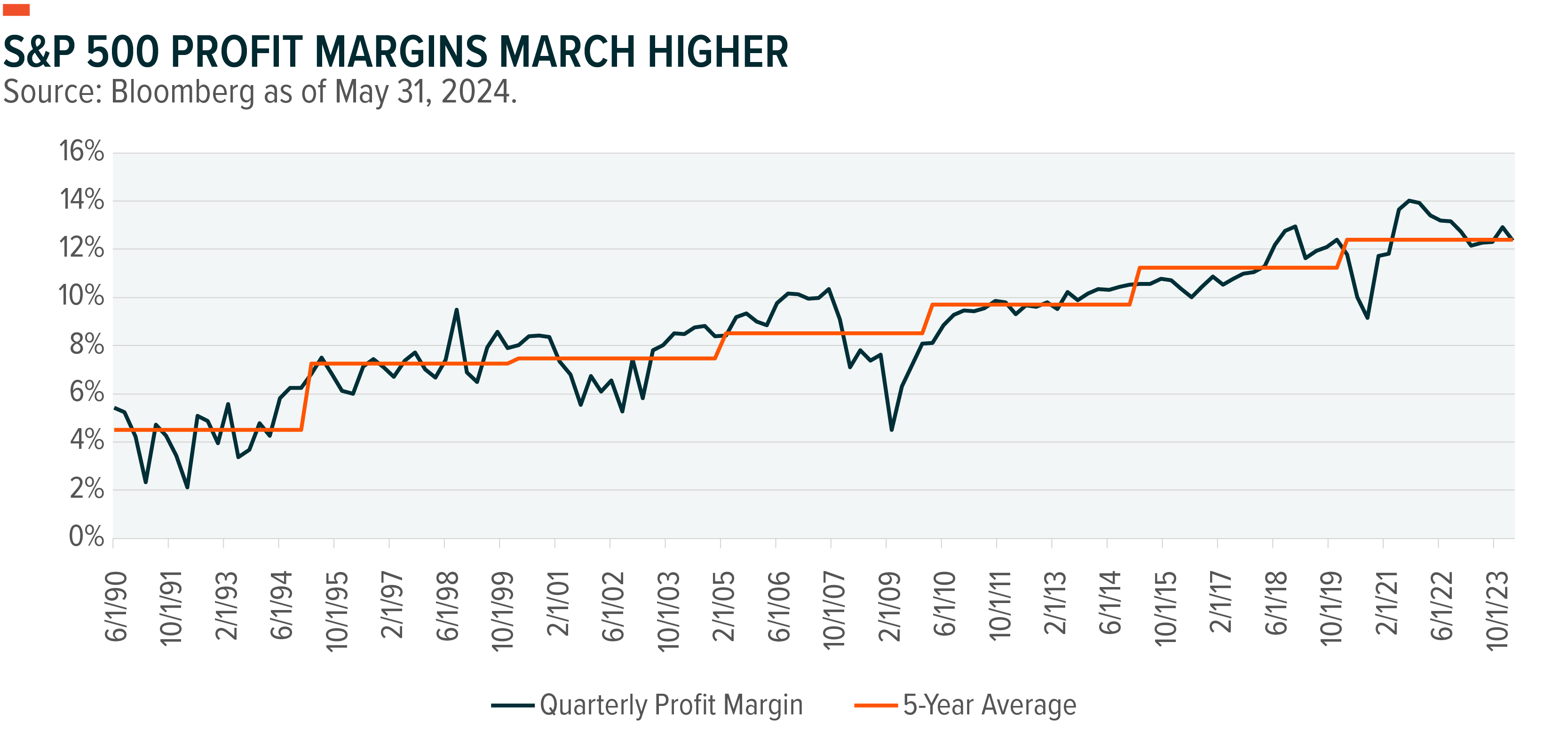

Profit margins for large-cap companies hit record highs the past few years and stepped up meaningfully from the 2010s. The S&P 500 delivered quarterly profit margins above 12% for 13 consecutive quarters, which is a first.13 Consensus forecast calls for further expansion to 13% in the second half.14

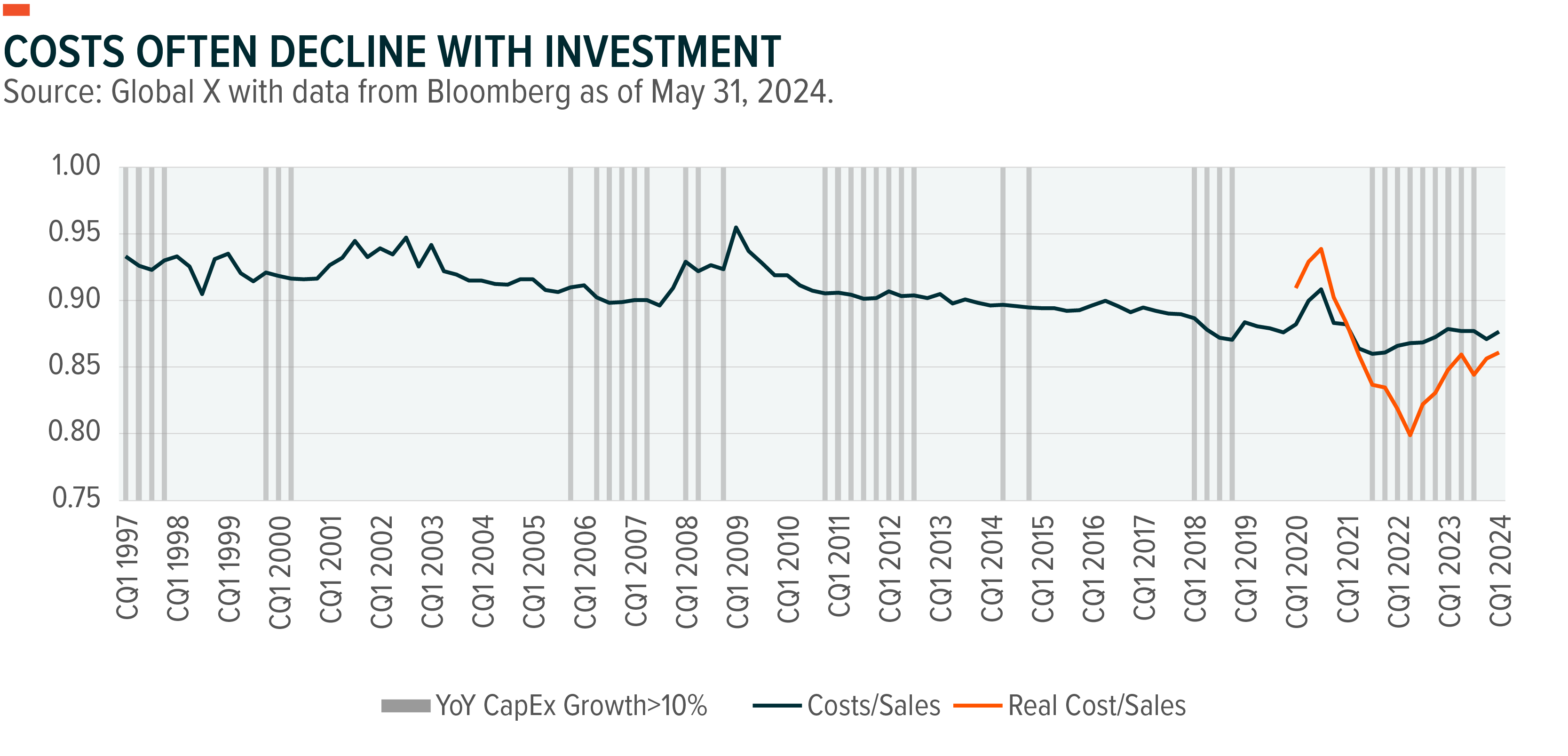

Margins may be able to move even higher. At a simplistic level, profit margins improve when companies grow sales faster than costs. This scenario can occur when the economy expands rapidly or companies cut costs by reducing labor costs and investing to develop more efficient processes. Focusing on the latter, costs typically grow slower than sales when capex growth exceeds 10%.15 Strong corporate spending would support better economic growth and potentially contribute to higher margins.

The recent period of extended capex growth looks a little different with costs outpacing sales. The historical relationship between capex growth and margin improvement may be breaking down, but the most recent trend is more likely a byproduct of higher producer inflation recently. Sales should be sensitive to the Consumer Price Index (CPI) with costs sensitive to the Produce Price Index (PPI), and the differential between producer and consumer inflation reached the highest on record in 2022.16 The relationship shifts when adjusting for inflation, and costs fell drastically relative to sales early in the high capex period.

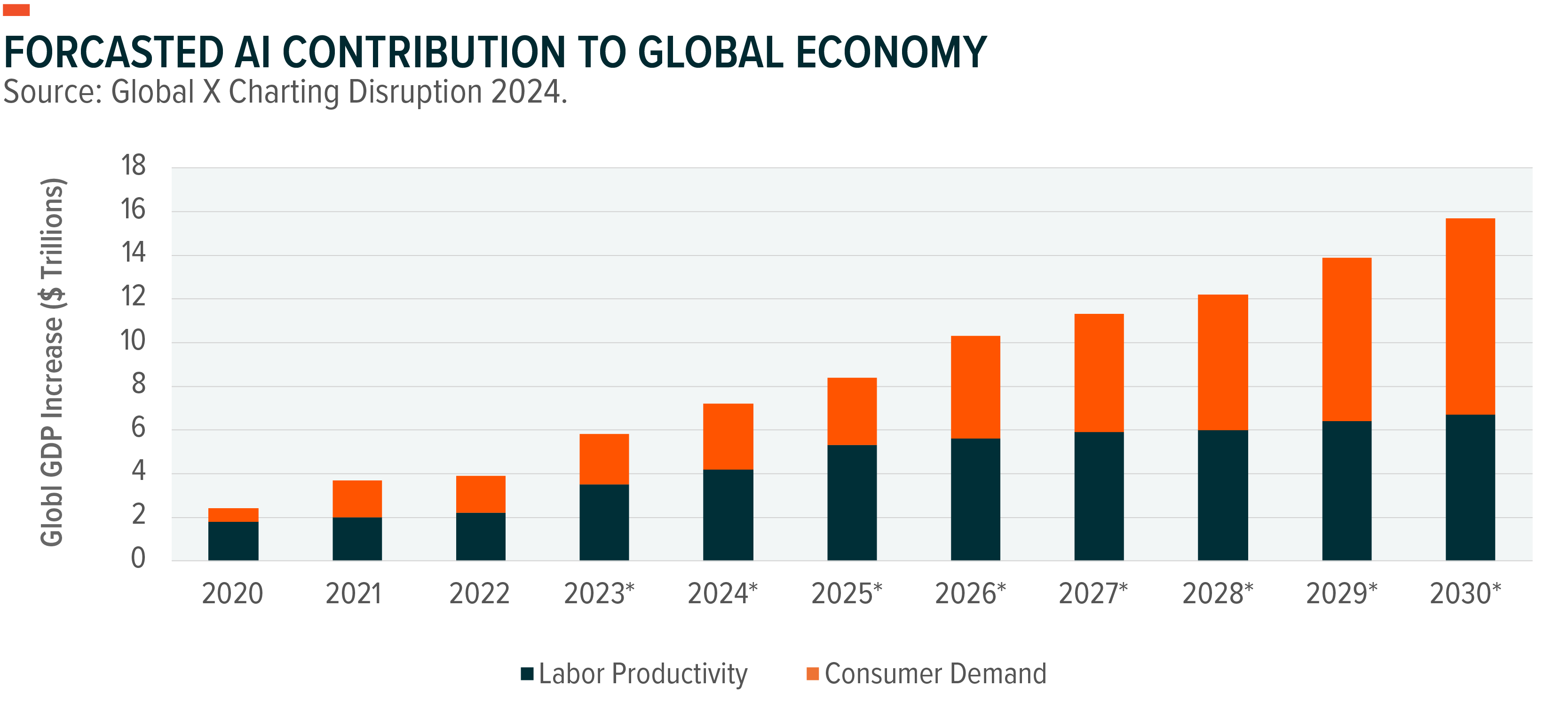

Then there’s AI, the topic du jour. ChatGPT was first released to the public in November 2023, and implementation of AI aimed at generating efficiencies is in the very early innings. Global cost savings from AI are estimated to reach $16 trillion annually in 10 years.17 The 2025 forecast calls for more than $8 trillion. Even if cost-savings from AI falls short and delivers only 20% of the forecast, that would still amount to a 10% reduction in the S&P 500’s last 12-month costs and a 10% improvement in profit margin.18 AI only needs to a deliver of fraction of expected benefits for the impact to be wide-ranging and help push margins meaningfully higher in the next few years.

Adoption of this cost-saving technology will not be uniform across the economy. Large companies with ample resources, both human and financial capital, will likely benefit first. Companies are piloting new technology while AI providers learn to monetize these new capabilities. Successful applications will likely be deployed within 12-18 months, refining products for easier adoption by mid- and small-cap companies, where margin expansion is more challenging.19

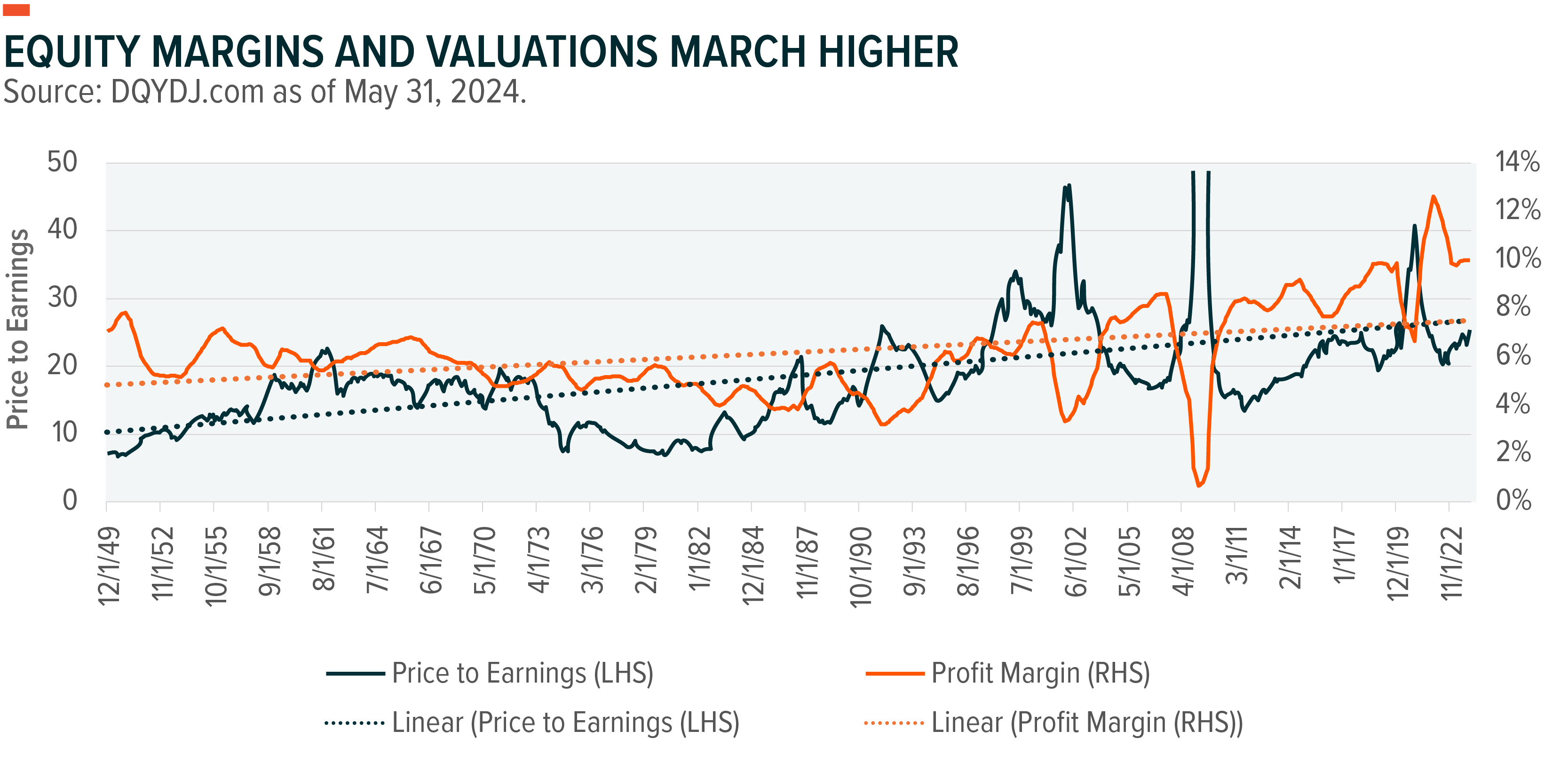

Continued margin expansion should interest investors because it could help catalyze higher valuations. While valuations seem rangebound at various points in any economic cycle, the long-term view tells a different story. Price-to-earnings multiples tend to move higher over time and follow margins.20 If companies are better at converting sales to profit, then investors may have to pay more. Should 12% margins prove sustainable, producer inflation remains tame, and AI delivers further efficiencies, valuations could move to a higher range.

Monetary Policy Vol Gives Way to Geopolitical Vol

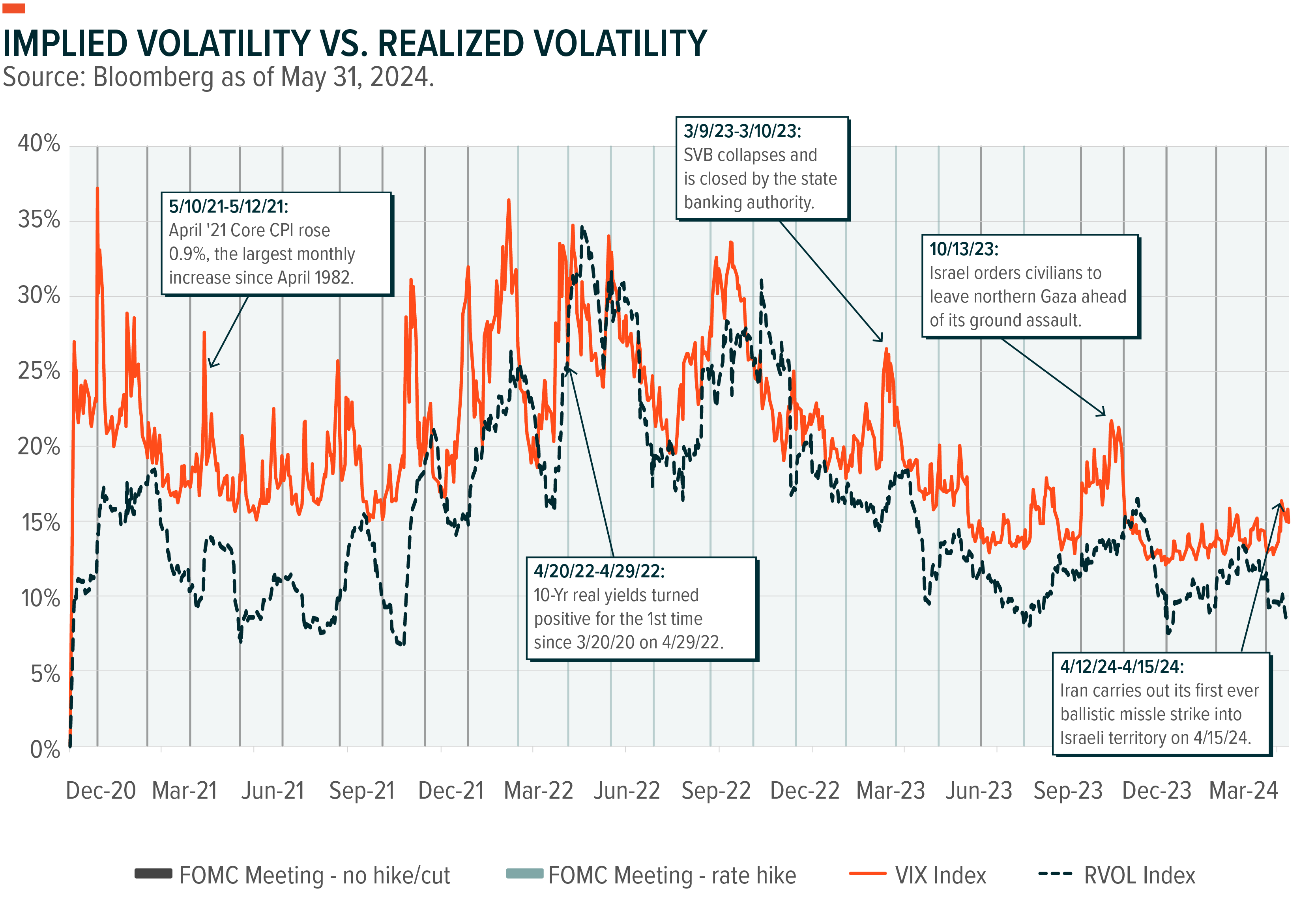

For the past two years, monetary policy was the big source of market volatility.21 With inflation slowing and fewer rate cuts expected, the increasingly tense geopolitical landscape may become a greater source of market volatility. Comparing implied and actual volatility provides some insight.

Significant challenges to core U.S. interests are now evident in four different theaters, creating a uniquely challenging environment in the post-World War II era. The geopolitical landscape in 1973 might be analogous, which featured Vietnam winding down, the Israeli-Arab War heating up, and a half-dozen coups around the world. In 1973, the United States accounted for 31% of global GDP.22 Today, it only accounts for about 25%, suggesting U.S. influence may be waning somewhat. The government and armed forces are not constructed to handle so many challenges at once, and adversaries understand these constraints.23

U.S.-China relations are probably at or near a historic low, and they could deteriorate further. Recently, the U.S. Department of Defense publicly noted that Chinese weapons were turning up in Ukraine, suggesting that intense Putin-Xi engagements are paying off for Russia.24 The U.S. subsequently warned China of dumping cheap goods onto the global markets and tightened tariffs, which drew condemnation and increased threatening rhetoric around Taiwan.25 Both U.S. political parties taking a hawkish stance on China going into the November elections could complicate matters.

The Middle East remains a critical U.S. interest. The October 7 Hamas attack, funded and encouraged by Iran, was intended to derail a historic peace agreement between Israel and Saudi Arabia, Iran’s two biggest regional adversaries.26 The attack also came at an auspicious time for Russia, a customer of Iranian drones.27 In a tit-for-tat escalation, Iran conducted a direct missile strike on Israel, which was reciprocated.28 While efforts to secure a Gaza ceasefire are ongoing, securing one will be difficult.

The Ukraine conflict is a third challenge. The Ukrainians achieved some impressive successes early on, Russia’s tactical shift towards greater brutality and civilian targeting shifted the momentum.29 The U.S.’ inability to send a clear signal of resolve and provide timely military support may have further improved Russia’s position.30 The West is finally about to allow Ukraine to strike targets within Russia, which is an important strategic step, but it’s also one that carries meaningful escalatory risk in the coming months.31

The fourth regional challenge is below the radar for many investors. Recently, Venezuela seized coastal territory from neighboring Guyana. The move gives Venezuela a claim to Exxon’s offshore oil rigs, which could amount to a seizure of U.S.-owned private property.32 Exxon has substantial investments in Guyana as well. The USS George Washington aircraft carrier group is now making an unscheduled stop in South America before proceeding to Japan.33 Meanwhile, Venezuelan President Nicolás Maduro has been posting pictures of his recent shipment of Iranian fast boats, known to menace U.S. warships, and Russian recently arrived in Cuba for Caribbean military exercises.34

This new global security landscape coincides with a contentious U.S. election. Once again, voters must choose from candidates with high unfavorability ratings, and independents will likely play a large role, making polling less reliable.35 The ties between Russia, Iran, North Korea, Venezuela, and possibly China add to the uncertainty, and misinformation and disinformation operations are likely.36 The lead-up to the November ballot, and the weeks following, could be a source of market volatility.

Second-Half Investment Considerations

Better-than-expected growth along with evidence of sustainable and improving margins could well lift stocks higher despite geopolitical risks. That said, the beta trade that started with end of the hiking cycle may be closing out. In recent weeks, the factors that worked best reversed, including momentum and size.37 Asset selection may prove increasingly important under these conditions, and we identify three areas to consider.

The AI Ecosystem Offers Reasonable Value

Corporate investment is a central part of our thesis for the rest of 2024 and into 2025, and much of that investment is going to AI and automation technologies.38 AI is not about one or two mega companies, but rather an ecosystem of companies that bring together hardware, software, and data to improve efficiency and decision-making. While the largest and most profitable companies are at the forefront, we expect ample opportunities among AI software developers, cloud computing providers, data centers, internet of things connectivity companies, robotics firms, materials providers, and energy suppliers.39

There is concern that much of the AI opportunity has been priced, but we believe the AI monetization cycle is only just beginning for most participants. The hardware companies, not just GPU chipmakers, are likely the first-wave beneficiaries, followed by software and data companies in the second wave, and then the firms that integrate AI will be in the third. Numerous opportunities in the ecosystem offer strong fundamentals and still reasonable valuations based on 2025 expectations.40

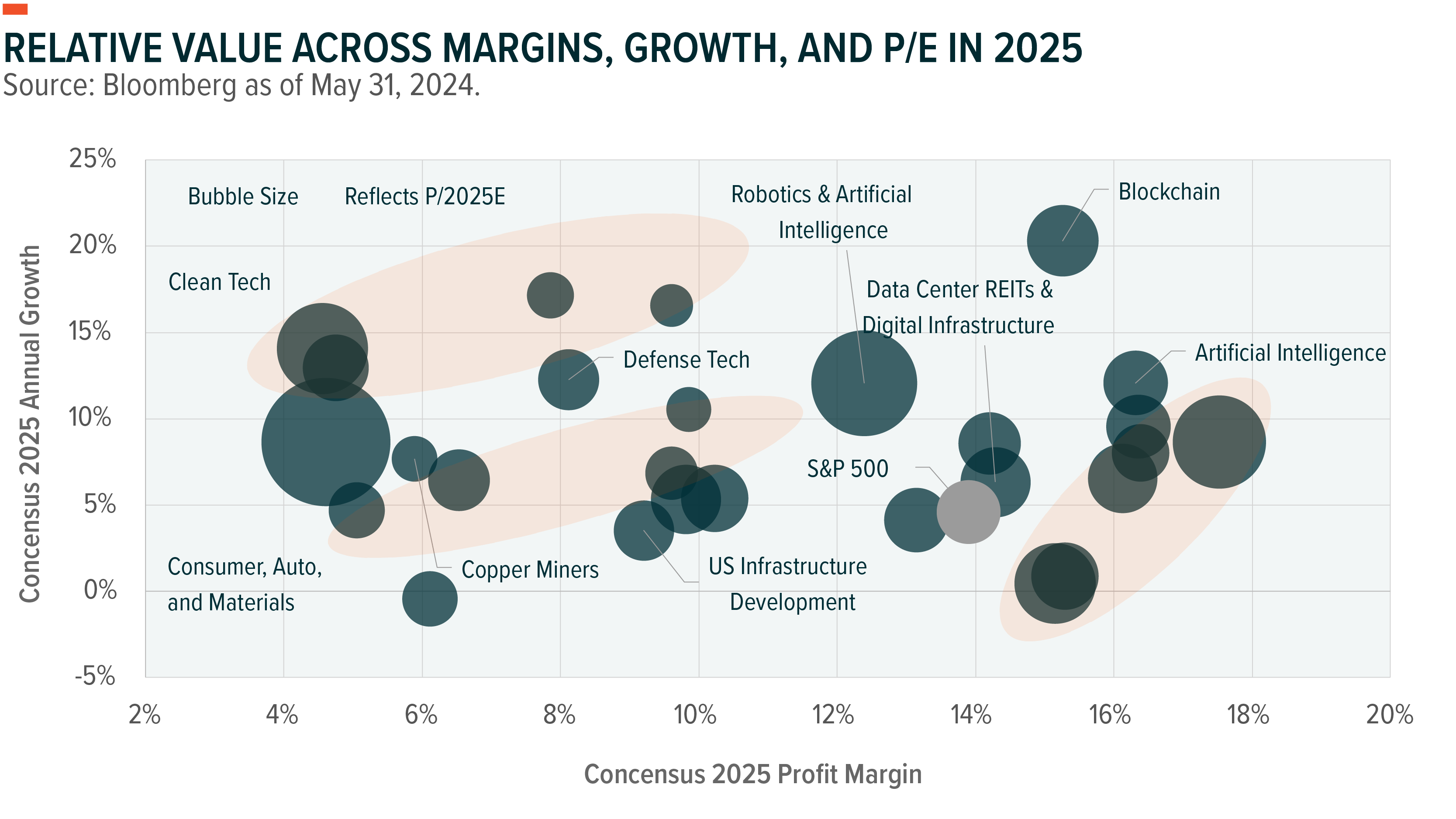

Three AI-related themes seem particularly well-positioned. The first is a broad basket of AI software and hardware companies currently selling at a 2025 PE of 19.3 times, compared to the broader S&P 500 at 19.1, but with better forecasted growth and margins.41 AI companies are expected to grow revenue 12% annually and deliver margins of 16%, compared to the S&P 500 with topline forecasts at 5% and margins at 14%.

The data infrastructure buildout remains critical to AI deployment and likely part of the first wave of monetization. Just a couple years ago, there was concern about overcapacity in data centers. Now, the concern is undersupply, which has led to swings in fundamentals.42 While data centers are currently priced at a modest premium to 2025 earnings at 21 times, margins are expected to expand meaningfully from 7% in 2024 to 14%.

Copper miners comprise a third theme. Materials companies can sell at meaningful discounts to the broad markets given the high fixed costs and lower margins, but valuations can charge higher with improved demand. The hardware buildout for AI, in conjunction with a healthy economy, provides secular and cyclical tailwinds.43 Cooper miners currently trade at 14 times 2025 despite double-digit price appreciation for the underlying commodity year-to-date. The relatively low valuation might suggest the cyclical tailwind fades out, but secular AI infrastructure demand could provide a second wind.

Port in the Geopolitical Storm

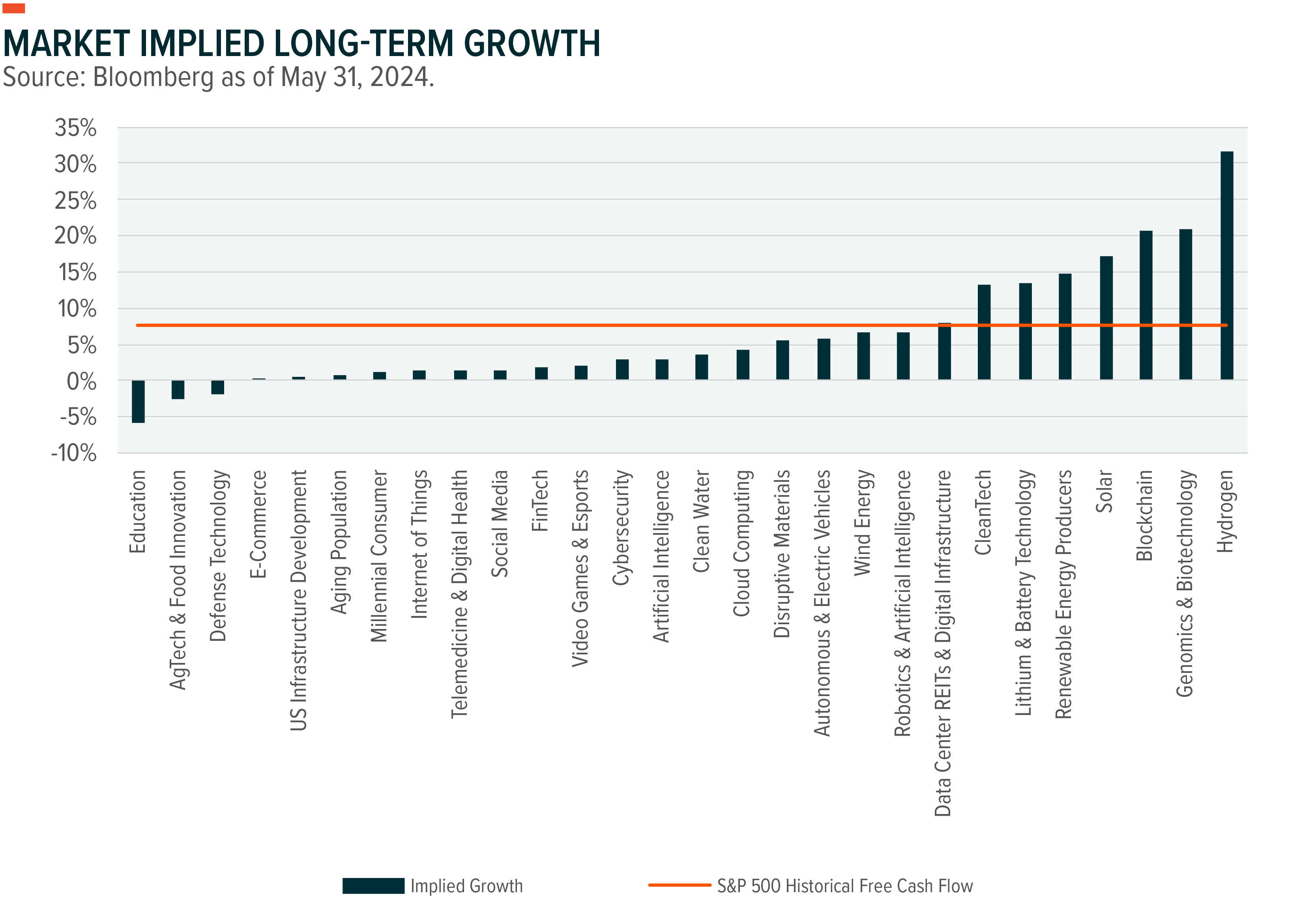

International and domestic politics could roil markets, but they may also present opportunities. To understand the how markets are pricing growth and potentially identify underappreciated assets, one metric that we use is long-term market implied cash flow growth. This incorporates consensus estimates and cost of capital to deliver market priced expectations for growth relative to the S&P 500’s historical cash flow growth at around 7.5%.44

In our view, one amid geopolitical-induced chop is the U.S. Infrastructure Development theme. The political parties are divided on many issues, but they both support infrastructure. The Infrastructure Investment and Jobs Act (IIJA) passed with resounding bipartisan support, as did the CHIPS Act to onshore technology manufacturing.45 When the parties talk of building a better economy for the future or focus on global competition, infrastructure is a common theme.

So far, $492 billion of the IIJA’s $1.2 trillion remains to be allocated, let alone spent.46 Infrastructure developers, in contrast to asset owners, build the facilities and are direct beneficiaries of the government funds. U.S. Infrastructure Development companies are forecast to deliver just 4% revenue growth and 9% margins through 2025.47 With significant infrastructure spending still to come, that revenue growth forecast could be low. The market implied long-term free cash flow growth is just 1%, and currently U.S. Infrastructure companies are selling at a discount relative to the S&P 500.

A second theme is Defense Technology. Even without the proliferation of global challenges, military spending seems like a compelling driver. The U.S. and China are spending over $1 trillion on defense this year alone, and they’re increasingly allocating capital to tech-related capabilities like AI and unmanned vehicles.48

Despite strong performance year-to-date, relative valuation is also compelling. Defense Tech companies are selling at 18 times 2025 earnings, a discount to the S&P 500. Revenue is expected to grow 12% annually, faster than the broader market, but margins are lower at 8%.49 Based on implied growth, the market forecasts long-term cash flow to the theme to shrink, but unfortunately, the geopolitical challenges driving defense spending are unlikely to subside anytime soon.

Reconciling Volatility with Hedged Equity

While healthy growth and margins remain our base case, there are risks to our optimistic forecast should corporate investment remain in single digits, economic growth slow, or margin expansion levels off. A hedged equity strategy offers upside participation while potentially reducing downside risk and volatility.50

One such strategy is selling a covered call on 50% of the underlying on a major index like the S&P 500 or the Nasdaq. This strategy provides an opportunity to participate in 50% of the upside should the index advance and generate an income stream, possibly in the 5-6% range, by selling the call and monetizing the premium. Along with the equity exposure, investors would get income in line with money markets. Given our expectations for increased volatility in the second half, investors may find hedged equity an attractive alternative.