India’s Digitization Journey: Opportunities for Stock Selection Beyond the Benchmark

India’s digital journey is one of inertia. India launched its “Digital India Program” in 2015, which has driven “new economy” sectors from ~5% to ~15% of gross domestic product (GDP), as structural reforms have opened the door to everyone from start-ups to multinationals to finally take advantage of India’s leading tech-stack.1 Furthermore, government incentives are now helping drive additional long-term growth opportunities. In turn, we see an abundance of unique secular investment opportunities in India.

Key Takeaways

- The Indian digital journey started nearly a decade ago with the Digital India Program, and the economy is now reaping its harvest.

- Reforms and incentives are supporting a shift in foreign direct investment (FDI) intentions, which will likely support long-term growth in India, especially within the “new” digital economy.

- We believe these rapid changes are creating a unique investment opportunity for active stock pickers beyond the average Indian benchmark.

The Launch of Digital India

The 2015 Digital India Program was based on three key pillars to help connect citizens and the government via e-services.

- Robust Digital Infrastructure (Identity):The first pillar to support the digital revolution was based on initiatives like Aadhaar, a unique digital identity program that helps millions of Indians access essential services and financial inclusion. Before the launch of Aadhaar, only one in 25 people had formal identification and only one in four had a bank account.2 The online bio-metric digital identity system now covers over 1.35bn people and has helped improve the know your customer (KYC) process, reducing the cost of e-KYC from US$12 to just US$0.06 (cents).3

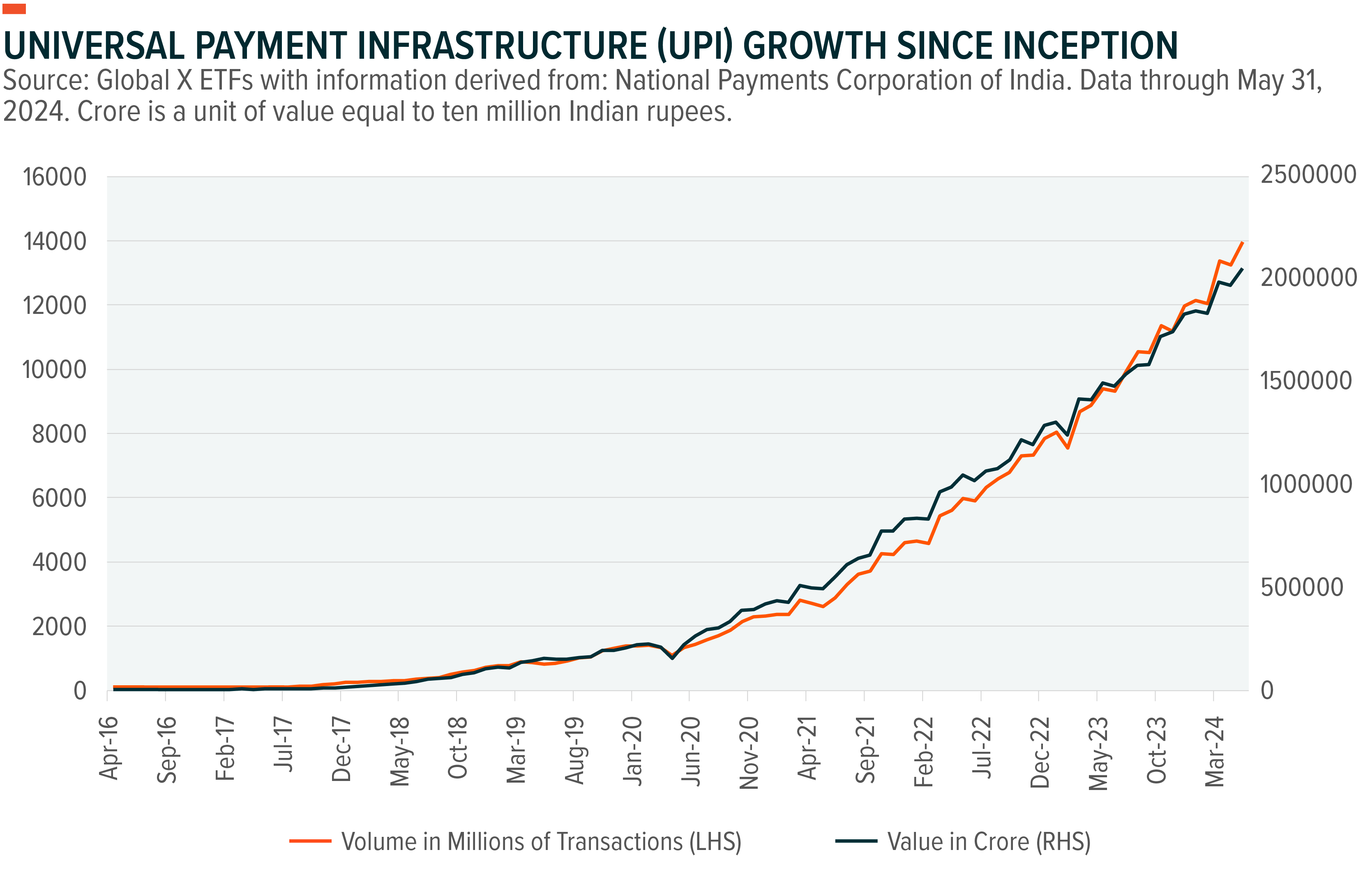

- Accessible Government Services (Payments):The second pillar was based on UPI – Universal Payment Infrastructure. UPI is helping formalize the digital economy by deepening financial inclusion as it helps small and unbanked businesses/individuals create financial records and credit histories, which then allow for the development of e-commerce. UPI transaction value grew from US$12bn in FY17-18 to US$1.66tn in FY22-23, with 118bn transactions in 2023.4

- Empowered Citizens (Data):The third pillar is focused on building an account aggregator framework that could transform the credit industry in India. In short, account aggregators act as consent managers that manage data-sharing across different institutions using the DEPA (Data Empowerment and Protection Architecture) infrastructure, which was launched in 2021.5 In turn, this helps solve the common issues of a lack of collateral and/or non-standard loan requirements. It also reduces the often-high cost of acquiring and verifying financial documents.

Roadmap for Development

Indian companies benefit from a unique infrastructure to drive innovation. The fact that the “India Stack” offers a set of open application programming interfaces (API) means entrepreneurs can leverage national infrastructure to develop services targeting all Indians.

India has expanded high speed internet networks across the country to help citizens take up the use of digital services. Smartphone penetration has grown from around 250mn in 2015 to over 1bn in 2023 with close to a 71% penetration rate.6 Within these 1bn smartphones, over 350mn cost only ~USD18, but are still interoperable with UPI.7

This has fostered the growth of the digital economy, underpinned by innovation and entrepreneurship. We believe domestic innovation is the next logical step, as India has already been a services powerhouse for global tech companies for years. In fact, the Google for India Digitization Fund will invest USD10bn by 2025 to help MSMEs (micro, small, and medium enterprises) digitize their business operations; Microsoft plans to train 100k developers in India in the latest AI tech and tools under its AI Odyssey initiatives.8,9

The National Payments Corporation of India (NPCI) launched UPI in 2016. UPI was created by a consortium of the Reserve Bank of India (RBI), public and private banks, and the government. UPI provides a 24/7, immediate, mobile-first payment system that provides an open API, unlike the closed payment system in neighboring China.10 This open architecture within the “India Stack” has driven private players to incorporate various applications, leading to a massive increase in UPI transactions. The result is increased efficiency in transactions, improved financial inclusion, and lower informality in the economy. This has set a stage for companies to grow with digital payment and lending capabilities that could increase cross-selling opportunities, cut costs, and boost profitability.

Opportunities Beyond the Benchmark

India’s powerful digital journey is creating opportunities beyond the benchmark – setting a potentially attractive backdrop for long-term stock pickers. For example, Zomato, a mobile food delivery and quick commerce platform was only listed in 2021 and took six months to be added to the MSCI India Index. The name is up nearly 150% since its listing, with just over 100% of the total return coming in the period before MSCI index inclusion.11 The company has continued to benefit from the growth in UPI and even received approval from the Reserve Bank of India (RBI) to operate as an online payment aggregator.

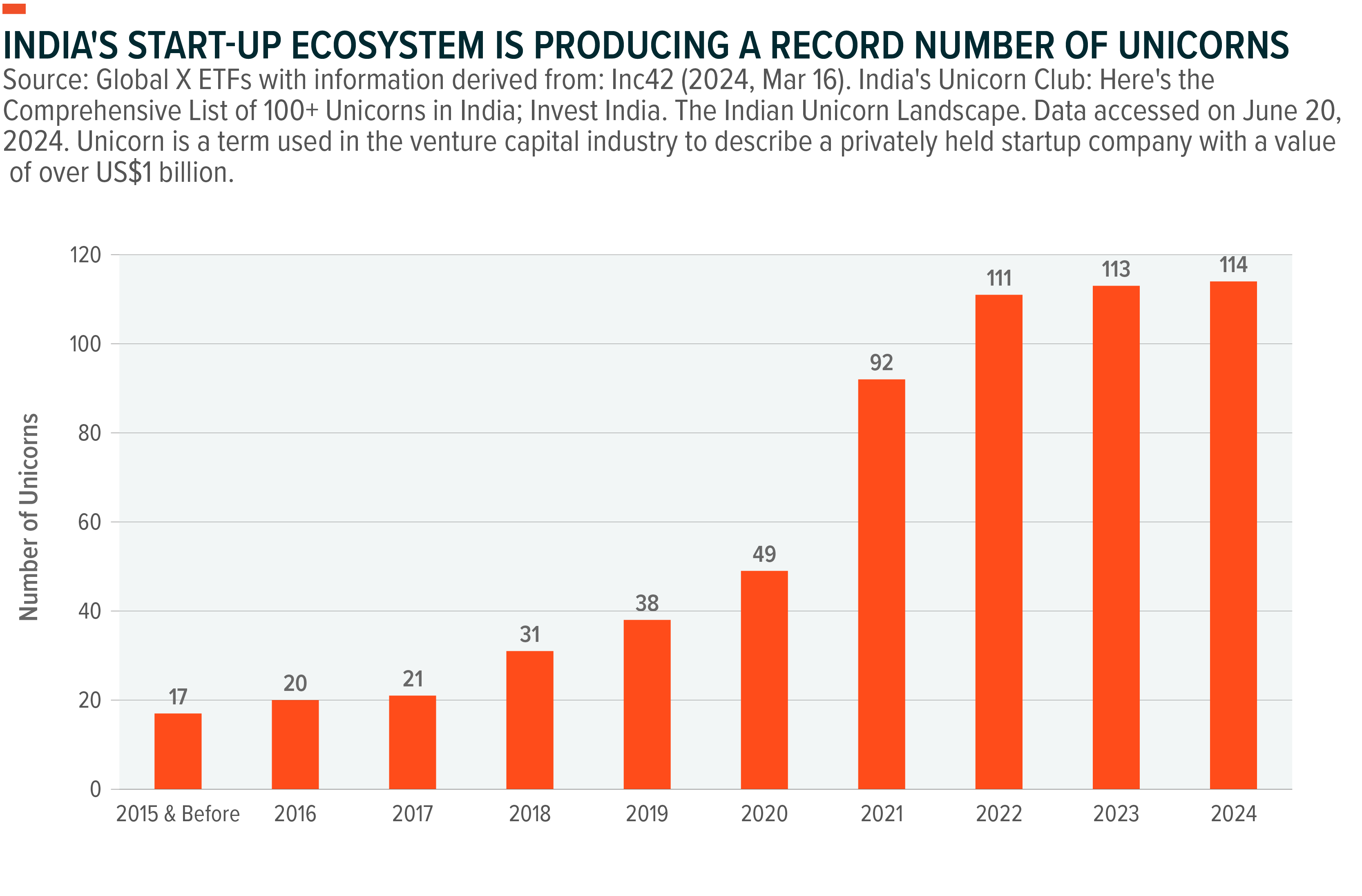

While Zomato might be one of the most well-known success stories, there are thousands of digital and e-commerce related start-ups in India seeking to take advantage of increased internet and smartphone penetration. India has the third largest start-up ecosystem in the world with more than 123k start-ups and a record 114 “unicorns” – those startups with a value of over US$1bn – worth more than a combined US$350bn.12 Furthermore, India is expected to have the second largest cohort of online shoppers by 2030 at 500-600mn, and we expect more companies to continue coming to market across industries from fast-moving consumer goods to rural micro-finance.13

We are also excited about the prospects of future IPOs, such as the potential listing of Reliance Jio Infocomm. This was the company that rolled-out 5G across India and introduced the affordable “Jio Bharat” phone, allowing low-income consumers to participate in the digital economy.

The beauty and personal care (BPC) segment is another beneficiary of India’s digital journey, as e-commerce is rapidly growing the direct to consumer (D2C) channel. Digital first BPC players are growing at twice the rate of traditional players.14 One local champion is Nykaa, which is competing in India’s expected US$30bn BPC market by 2027.15 The Company crossed over US$1bn in gross merchandise value (GMV) with ~12mn customers placing over 40mn orders in FY24.16

Digital India

Digital India is inclusive and prosperous. Before the Covid-19 pandemic, 92% of MSMEs in India still lacked access to formal credit.17 Digital India is changing that. It is increasing efficiencies, improving competitiveness, helping bridge the rural economic divide, and is likely setting up the country for another decade of growth. MSMEs represent roughly 30% of GDP and nearly 50% of exports, so their digital development and transformation could create step-change economic growth.18 Today, the “India Stack” remains the global benchmark for digital programs, and we are encouraged to see how the wide scale adoption of UPI and digital payments is helping formalize and grow the economy. As economies go through these powerful and structural transitions, it creates a unique opportunity for active stock pickers.