Growing Policy Support Creates Strong Tailwinds for the Low-Carbon Hydrogen Industry

Low-carbon hydrogen holds substantial promise as a pathway to decarbonize a range of hard-to-abate industries such as refining, fertilizer production, long-haul transport, and shipping. While low-carbon hydrogen accounts for less than 1% of total hydrogen production, the green and blue hydrogen industries are taking shape and are forecast to grow quickly.1,2 Today, most hydrogen is grey hydrogen, produced through a process of steam methane reforming (SMR). However, hydrogen’s production methods can be environmentally friendly. In particular, zero-emissions green hydrogen is produced through electrolyzers powered by renewable energy, while low-emissions blue hydrogen is produced through SMR with the addition of carbon capture, utilization, and storage (CCUS) technology. By 2030, low-carbon hydrogen production could reach 38 million tonnes (Mt), up from less than 1 Mt in 2022.3 In our view, robust government support, including in the United States, is a major reason for why this nascent industry is primed to scale. In this piece, we highlight key government initiatives that are likely to create significant growth opportunities over the coming years for companies throughout the hydrogen value chain.

Key Takeaways

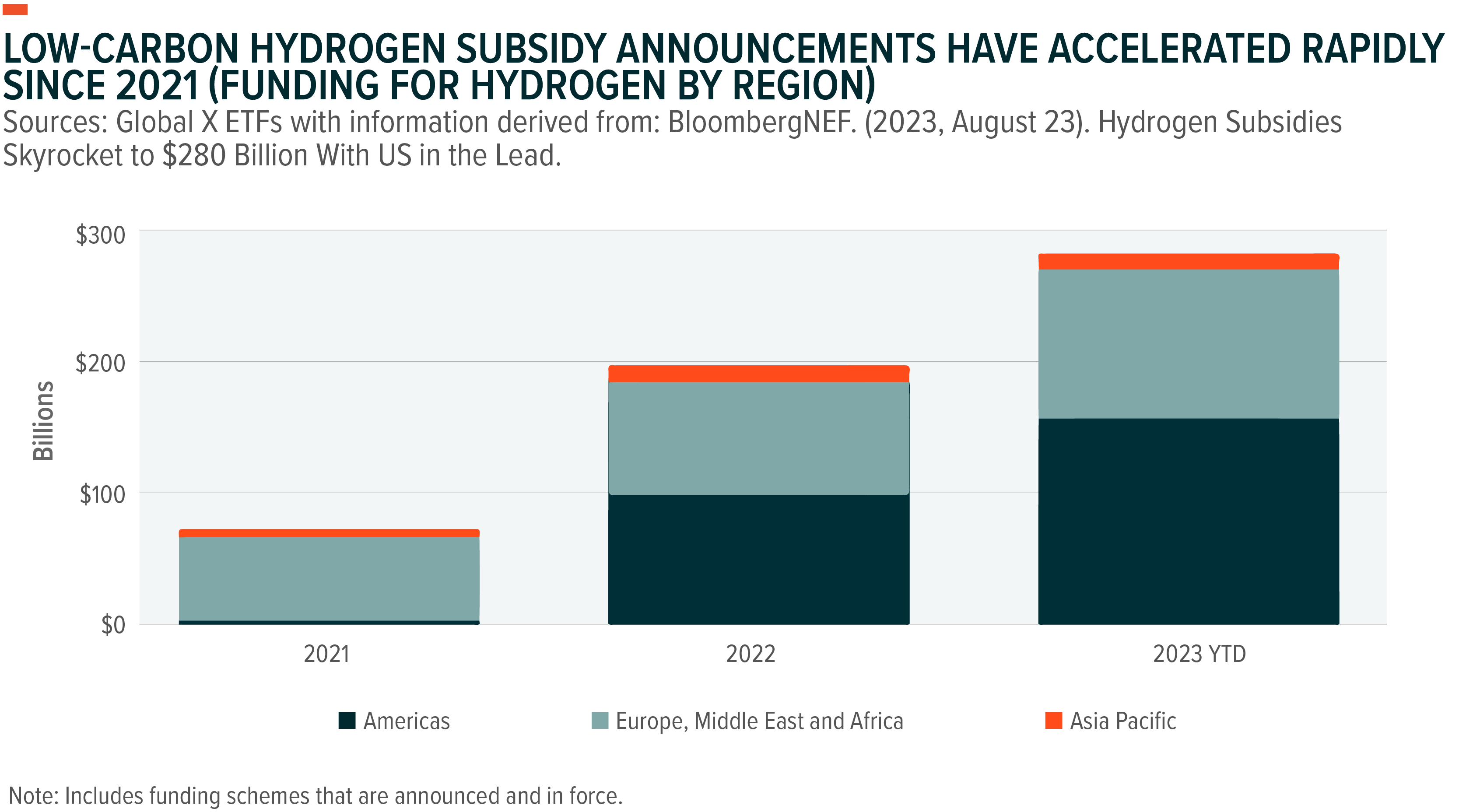

- Governments have announced over $280 billion in subsidies for low-carbon hydrogen, creating robust growth opportunities for the nascent green and blue hydrogen industries.4

- The U.S. has particularly strong policies in place to encourage the development of a low-carbon hydrogen industry, with the Biden Administration recently announcing $7 billion in funding towards the creation of regional hydrogen hubs.5

- As the low-carbon hydrogen industry scales, companies throughout the hydrogen and renewables value chains are likely to benefit.

Policy Support for Low-Carbon Hydrogen is Rapidly Accelerating

In the past five years, more than 50 governments have published national hydrogen strategies, including the United States, Canada, China, India, Brazil, Chile, Germany, the United Kingdom, and South Africa.6 In these publications, governments outline plans to rapidly scale clean hydrogen production and use. For example, The U.S. National Clean Hydrogen Strategy and Roadmap, published in June 2023, envisions 10 Mt of domestic clean hydrogen production by 2030, 20 Mt by 2040, and 50 Mt by 2050.7 The European Union is also targeting 10 Mt of domestic hydrogen production per year by 2030.8 For context, global hydrogen production totaled 95 Mt in 2022, of which less than 1% was clean hydrogen.9

In order to hit the milestones outlined in these hydrogen strategies, governments are quickly ramping up support for the clean hydrogen industry. Over the past two years, announced subsidies for low-carbon hydrogen have quadrupled to reach over $280 billion as of August 2023.10 Given the rapid pace of development, most of these subsidies have yet to fully materialize, meaning that companies throughout the clean hydrogen value chains could benefit for years to come.

The United States accounts for nearly half of these subsidies, with $137 billion projected to primarily go to projects that are eligible for the clean hydrogen production tax credit.11 The tax credit, created in the Inflation Reduction Act, offers up to $3 per kilogram of low-carbon hydrogen, which could help green and blue hydrogen reach cost parity with traditional grey hydrogen more quickly.12 In addition to tax credits, the U.S. government is also implementing research and development funding and grant programs, including $7 billion towards the development of regional hydrogen hubs.13,14

There are also increasingly robust subsidies outside of the U.S. that provide further tailwinds for low carbon hydrogen development, particularly in Europe and Asia. Governments in the Europe, Middle East, and Africa region have announced over $100 billion in subsidies.15 In August 2023, the Government of France announced plans to provide €4 billion in subsidies for projects that focus on the production of hydrogen from clean energy sources such as renewables and nuclear.16 The Asia Pacific region’s subsidies total over $11 billion from initiatives by governments in Singapore, India, Australia, and China, among others.17,18

Billions in Funding for U.S. Hydrogen Hubs Set Up Significant Opportunities

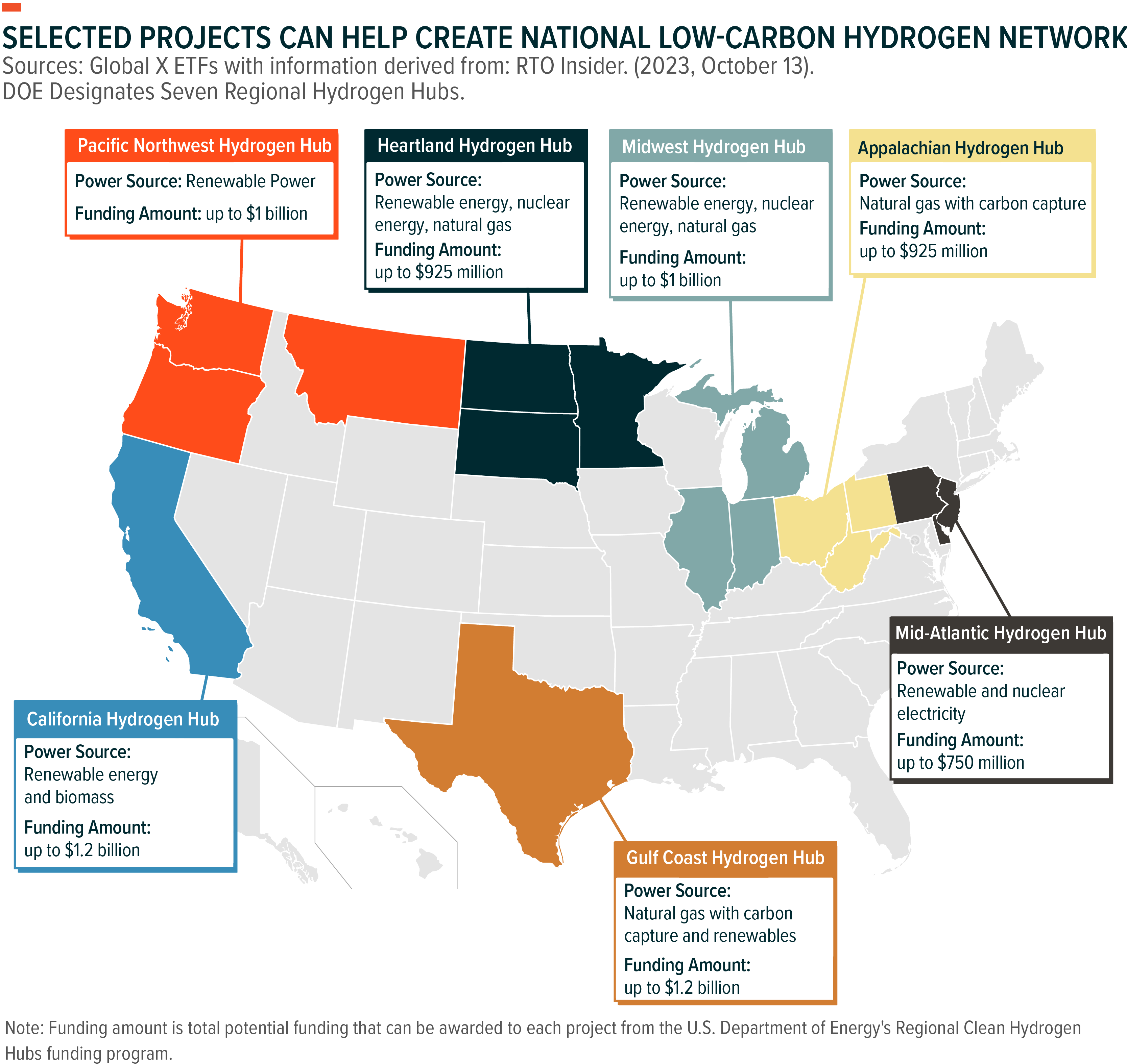

In mid-October, the Biden-Harris Administration announced seven regional clean hydrogen hubs that are eligible to receive up to $7 billion collectively in funding from the Infrastructure Investment and Jobs Act.19 With this funding, the U.S. government aims to help accelerate the development of a domestic affordable clean hydrogen industry. The seven hubs are planning to produce more than three million metric tons of clean hydrogen per year, which would be equal to about one-third of the country’s clean hydrogen production goal for 2030.20

In our view, this funding marks a potentially significant step forward for the industry, as these hubs could form the basis for a national clean hydrogen network in the United States. Notably, two-thirds of the funding is expected to go towards the production of green hydrogen.21 Hydrogen hubs consist of localized hydrogen production, hydrogen demand, and connective transport and storage infrastructure, all in close proximity.22 Benefits of developing hubs include reducing challenges around shipping and storage and building a robust hydrogen workforce, two components which we believe are essential for early projects to succeed.

Additionally, the seven hubs are projected to help catalyze more than $40 billion in private investment.23 Some of the companies that are partners within the selected hydrogen hubs include fuel cell and electrolyzer manufacturers Bloom Energy and Plug Power, fuel cell producers Ballard Power Systems and FuelCell Energy, industrial gas supplier Linde PLC, hydrogen vehicle makers Hyzon Motors, General Motors, and Hyundai, as well as renewables project developers Brookfield Renewable Partners and Ørsted, among others.24,25

Conclusion: Long-Term Growth Cycle Likely Just Beginning

The low-carbon hydrogen market is growing quickly, with increasingly robust government policies playing a key part in the rising momentum. Hundreds of billions in government subsidies are set to be distributed over the coming years, which can help amplify private investments and accelerate the timeline for tech advancements, cost declines, and low-carbon hydrogen adoption. As the industry matures over time and details on government programs come into focus, we expect companies throughout the hydrogen value chain to benefit, creating compelling opportunities for investors.

Related ETFs

Click the fund name above to view current holdings. Holdings are subject to change. Current and future holdings are subject to risk.