Gaming Industry Charts a Rebound in 2023

After the pandemic-induced spike in gaming, player engagement dipped in 2022 as everyday life resumed. Persistent supply chain disruptions that delayed launches and caused hardware scarcity also took their toll. In 2023, the gaming industry hit the reset button. Highly anticipated game releases, innovations in mobile gaming, a resurgence in in-app purchases, and advancements in cloud gaming are among the factors responsible for the positive momentum the industry has heading into 2024. In this report, we discuss these and other factors, including the positive industry signal that is the recent green light for the Microsoft–Activision Blizzard merger.

Key Takeaways

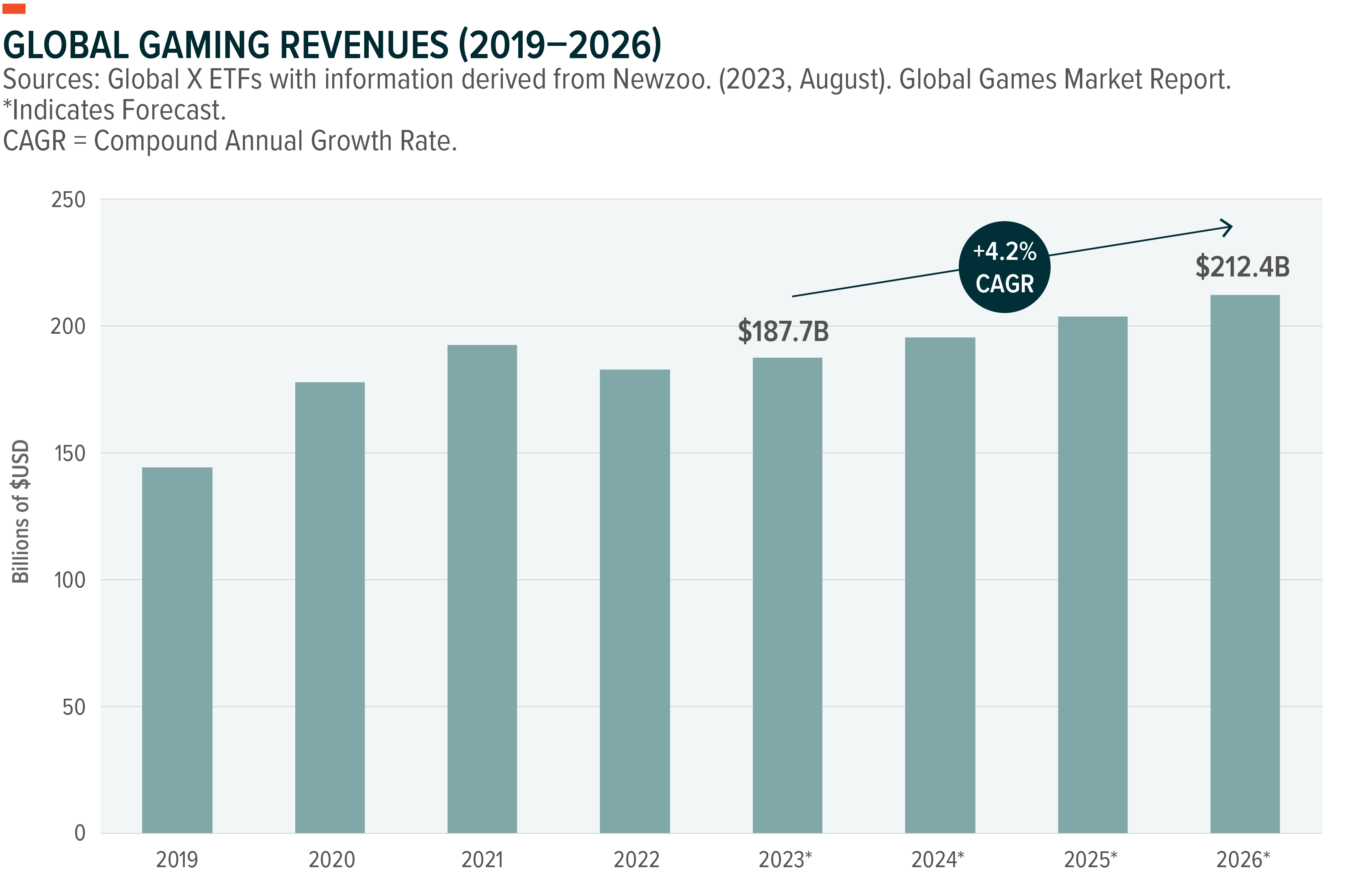

- U.S. gaming sales are on an upswing in 2023. Results thus far set the industry up for success, in our view. According to one estimate, global gaming revenues are projected to soar beyond $212 billion by 2026, a 16% increase from 2022.1

- The gaming industry owes much of its recovery in 2023 to strong console sales, which can continue with the help of new game titles. Expectations for a 2.6% year-over-year (YoY) increase in global gaming revenue to $187.7 billion in 2023 are largely driven by a potential 7.4% surge in hardware sales.2

- In addition to resurgent spending activity, we expect gaming to benefit from heightened merger and acquisition (M&A) activity and breakthroughs in mobile and cloud gaming.

Strong Growth in the U.S. Gaming Market

Improving economic conditions and persistent consumer strength accelerated U.S. gaming sector sales in recent months, particularly in September, when sales increased a significant 10% YoY to $4.5 billion.3 This growth continued the positive momentum from the first nine months of the year, during which the sector totaled $39.4 billion in revenue, a 2% YoY increase.4

The strength in the market is further confirmed by the three gaming hardware giants. Microsoft, Nintendo, and Sony all reported strong results in recent quarters. In Q1 Fiscal Year (FY) 2024, Microsoft reported a 13% YoY increase in Xbox content and services revenue, and Nintendo’s revenue surged 50% YoY thanks to The Legend of Zelda: Tears of the Kingdom release.5,6 Also, Sony’s PlayStation unit continued to perform well, leading to a 7% upward revision of its sales forecast for games and network services in Q2 2023.7

Hardware Reigns Supreme as the Primary Catalyst

Hardware gaming sales, which can be a strong leading indicator of spending on content and services, bounced back in a big way in 2023. As of the end of September, U.S. hardware sales had increased by an impressive 10% Year-to-Date (YTD).8 This trend aligns with global gaming industry projections for a 7.4% surge in hardware sales to drive overall revenue to $187.7 billion this year.9

The revived interest in consoles is attributable to several factors, including the release of long-awaited game titles, including some that were previously delayed. Also, the supply of new gaming consoles finally caught up with demand.

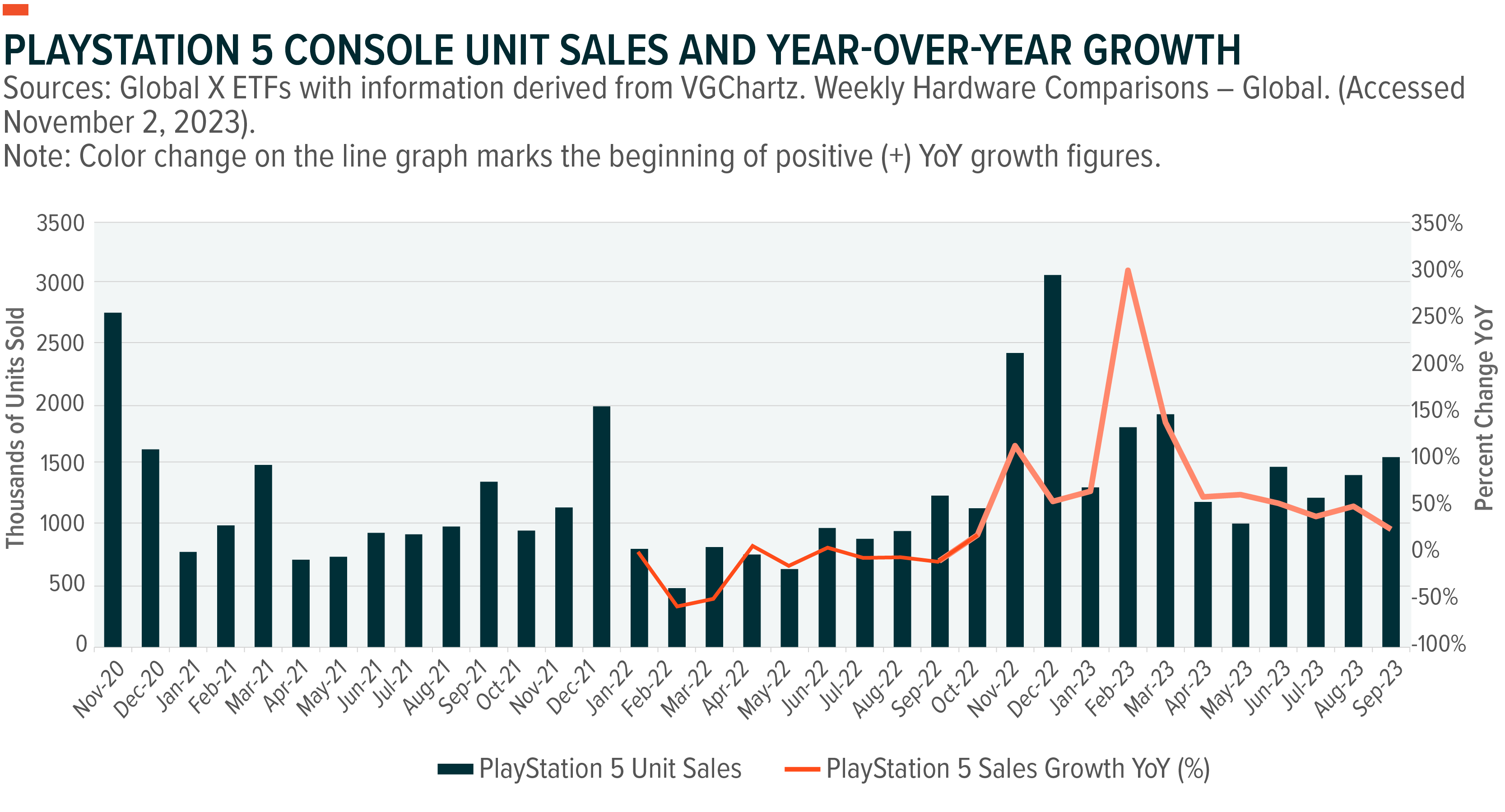

Console sales and new game titles often go hand in hand. For example, launched in November 2020, the PlayStation5 (PS5) has reported monthly YoY sales growth since October 2022.10 The release of popular game titles also played a pivotal role in nurturing this growth reacceleration. For instance, Marvel’s Spider-Man 2, an exclusive PS5 title, sold over 2.5 million units worldwide in the first 24 hours of the highly anticipated game’s release in October 2023.11 The release’s success, including that of the limited edition DualSense controller bundled with the game, enhanced the console’s attractiveness to consumers. This trend may also foreshadow a healthy 2023 holiday season for the PS5.12

Similarly, the release of the long-awaited Starfield largely impacted Xbox Series X sales, which increased 1,056% on Amazon leading up to its early access launch.13

Key Factors Likely to Shape the Gaming Industry’s Trajectory in 2024

In addition to an uptick in spending activity, we view an active M&A market and breakthroughs in mobile and cloud gaming as the main factors that can propel the gaming sector over the next 12 months.

- Favorable M&A Environment:Microsoft’s acquisition of Activision Blizzard, which cleared in Q3 2023, can help the industry embrace more M&A. Last year, there were a total of 222 M&A deals in the industry, with most of them geared towards expanding gaming ecosystems.14 We expect that number to tick up in the coming years as weakened economic conditions compel smaller firms to consider alternatives. Notably, game developers are investing in the mobile game ad spending space, strategically acquiring struggling in-game ad companies. U.S. mobile game ad spending is projected to reach $6.67 billion in 2023, up 12% from last year.15,16

- Gaming Hardware Upgrades:Advancements in personal computing and mobile devices aim to bring high-fidelity, graphic-rich gaming experiences beyond consoles, appealing to a broader audience, and growing the total addressable base. For example, Apple recently made a game-changing move by introducing AAA games, including titles like Assassin’s Creed Mirage, Resident Evil, and Death Stranding, to its iPhone Pro 15 models, starting H1 2024.17 Also, Apple fortified its gaming PC offerings by launching its M3 family of processors, which come equipped with advanced central processing unit (CPU) and graphics processing unit (GPU) capabilities.18

- Cloud Gaming Adoption:Despite delays, cloud gaming is coming of age. Helping develop its mainstream appeal is Netflix, which is launching an experimental version of gaming on its platform in the United States.19 The company intends to increase gaming’s share of its overall revenue in the coming years, in part by making gaming accessible across various devices.20 In our view, this move has the potential to stimulate mass market adoption for interactive streaming and gaming by eliminating the high entry cost associated with consoles.

Conclusion: Gaming’s Investment Case Gets a Reset

The gaming industry has weathered its share of challenges in recent years and is emerging from a period of decline with revitalized strength. Strategic initiatives by key players such as Microsoft, Apple, and Netflix along with the industry’s increasing focus on M&A activity, signify a dynamic and competitive environment that can evolve into different dimensions over time. And as it does, we expect it to offer investors differentiated opportunities to participate in a thriving market. Meanwhile, gaming valuations remain at historical lows, further boosting the investment case.

Related ETFs

HERO – Global X Video Games & Esports ETF

Click the fund name above to view current holdings. Holdings are subject to change. Current and future holdings are subject to risk.