Energy & MLP Insights: U.S. Midstream Sector Can Gain from M&A Activity and Energy Supply Fundamenta

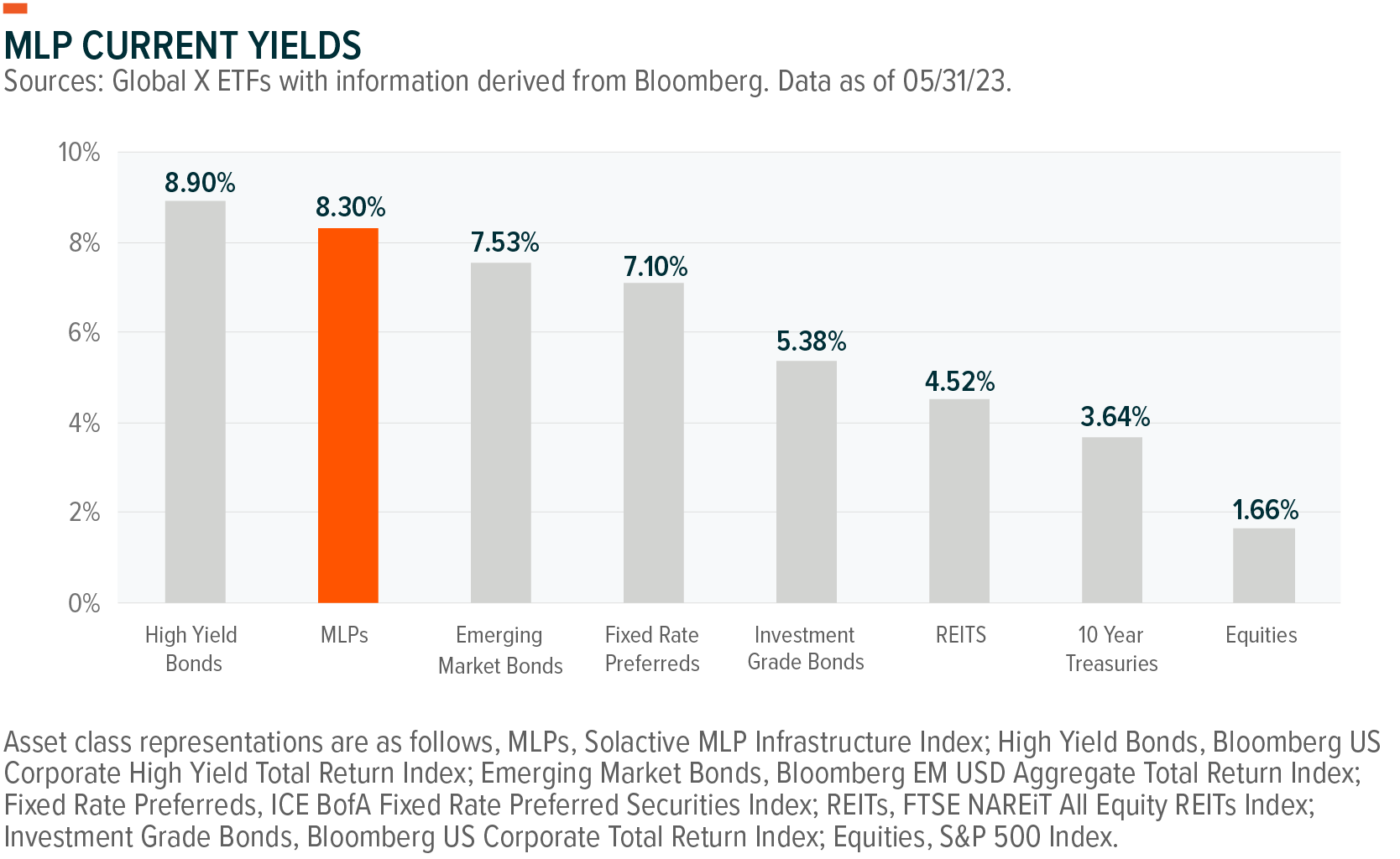

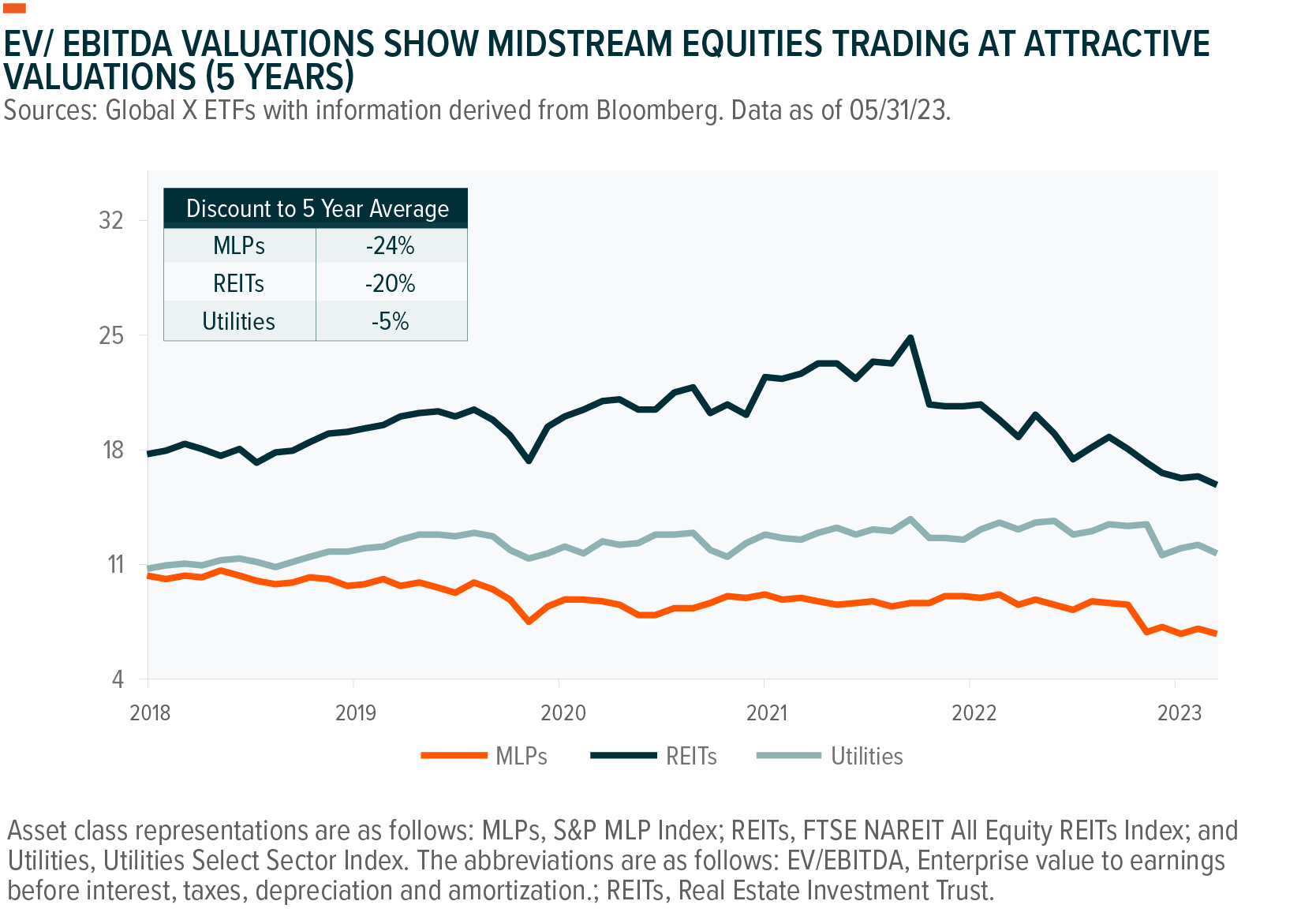

U.S. midstream pipelines continue to show high distribution yields and inexpensive valuations, and even after a prolonged upswing, we believe that sector offers a compelling investment case. As we discussed in our last Energy & MLP Insights, diversification potential and inflation pass-through capabilities are core features of the sector. Historically, its defensive contracts and fee structures make it better positioned in volatile price environments than other energy sectors. This quarter, we highlight how the industry increasingly turning to mergers and acquisitions (M&A) for growth can potentially sustain its positive momentum. We also highlight how OPEC+’s recent decision to extend production cuts can create positive supply fundamentals for U.S pipelines amid record energy production in the United States.

Key Takeaways

- M&A activity remains an increasingly popular growth strategy among pipeline operators. Oneok’s recent acquisition of Magellan is but one prominent example.1

- OPEC+’s decision to follow through with additional cuts may add price volatility to an already tenuous price environment, but it is likely to benefit the U.S. energy industry.

- Record U.S. oil and gas output means demand for midstream infrastructure like pipelines, storage, and processing plants is likely to remain high.

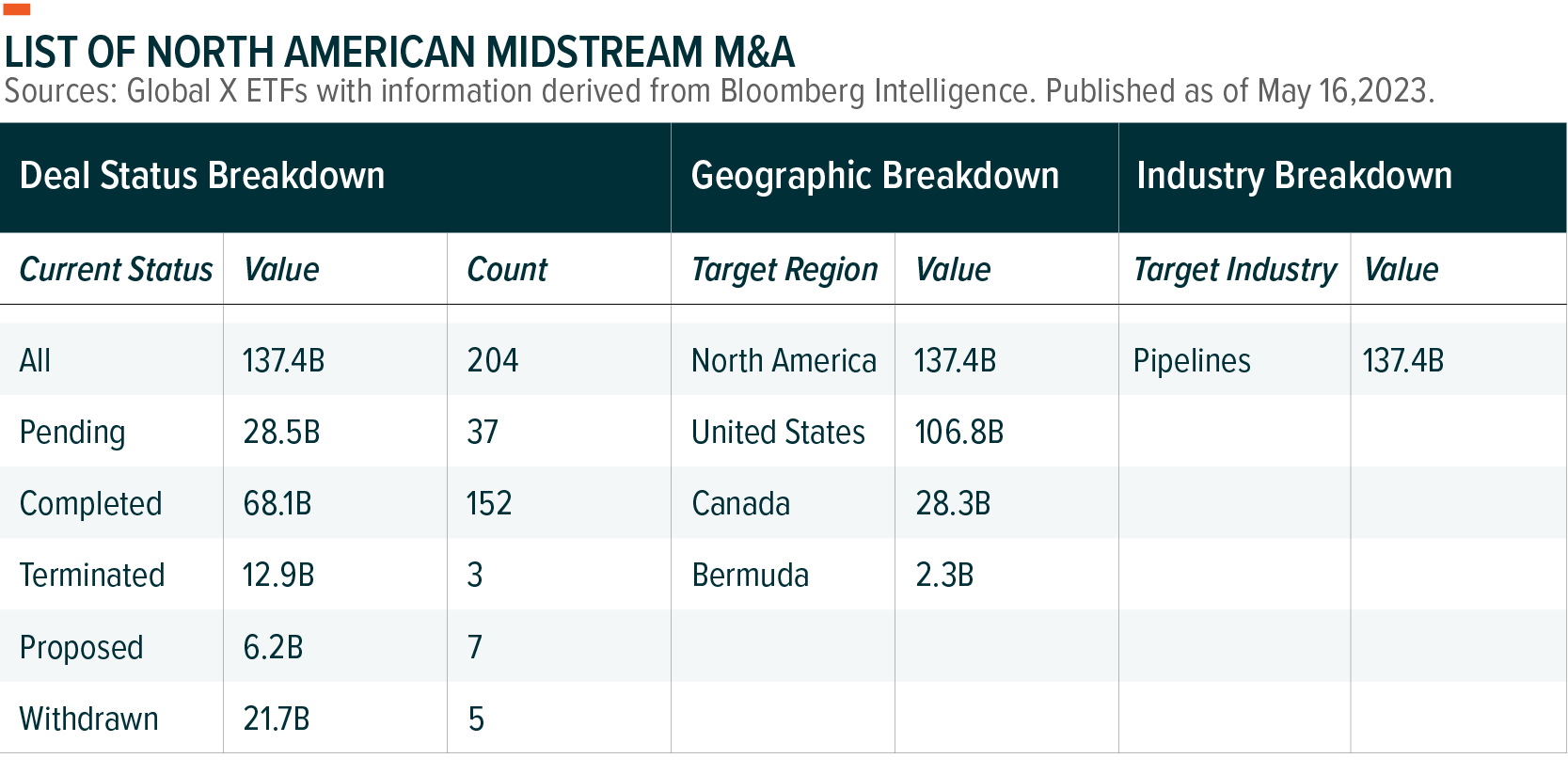

U.S. Pipeline Firms Are Growing Through M&A

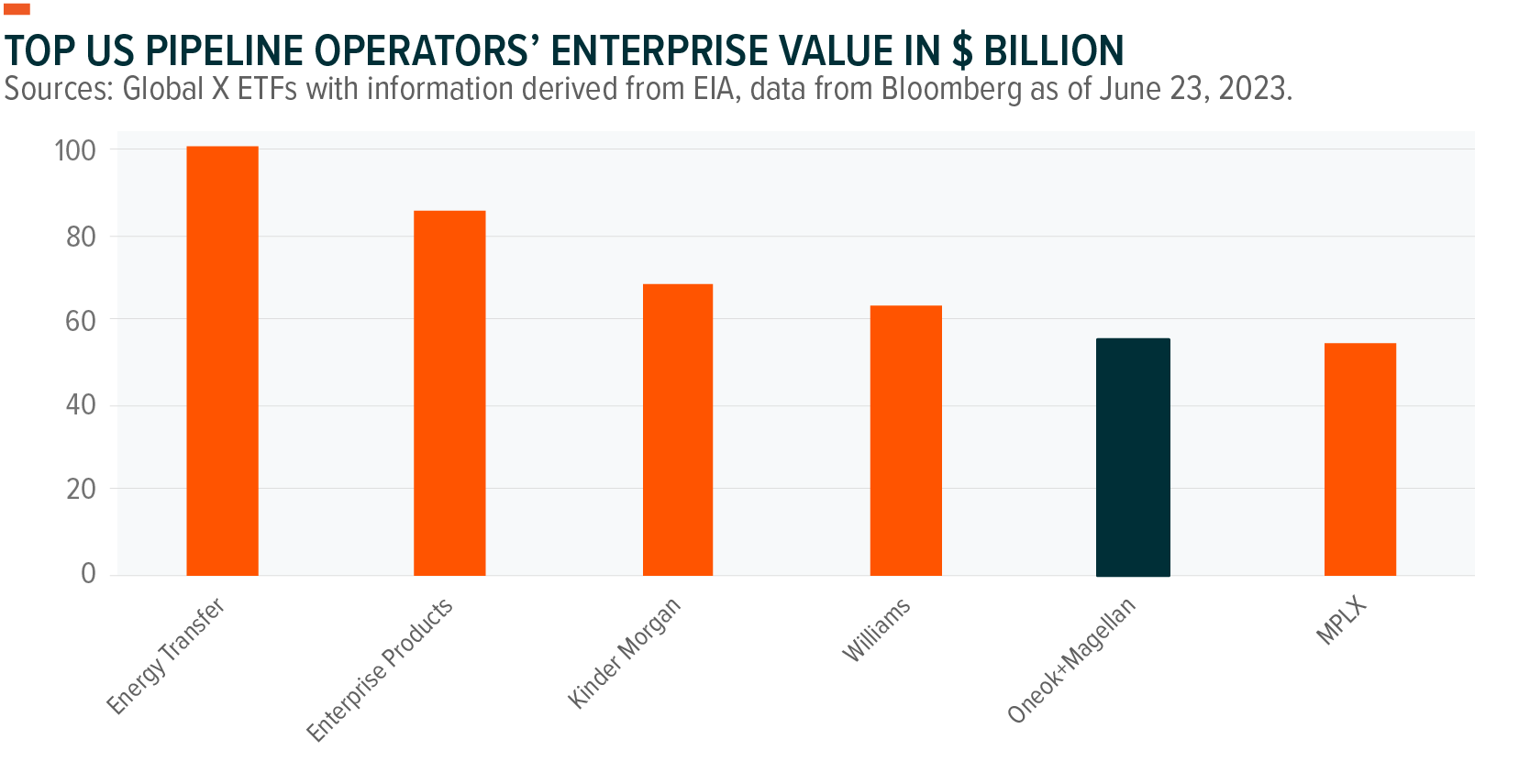

In May, leading U.S. pipeline company Oneok announced that it would pay $18.8 billion to purchase Magellan Midstream Partners, the latest deal in what has been a robust multi-year run of M&A activity in the industry. The deal between two companies that have successful track records of generating diverse free cash flow and impressive returns on capital is expected to be finalized in Q3 2023. With a market value of almost $60 billion, the combined entity will have an extensive pipeline network that spans 25,000 miles, making it one of the largest oil and gas infrastructure corporations in North America.2

Oneok, whose primary focus is the gas business, believes that the acquisition will give it a considerable position in the crude and refined products markets. Potential benefits include more predictable cash flows despite fluctuations in the commodities markets and a more resilient energy infrastructure organization. In the near term, Oneok expects the deal to result in immediate monetary gains and to have a favorable effect on earnings per share and free cash flow per share.3 With a more diverse commodity mix and the efficiencies that come with higher scale, we expect the combined business to be more appealing to generalist investors.

M&A can help midstream companies expand their operations quickly, increase their profits, and cut their operating expenses, and in this environment, we expect the deal activity trend to continue. Other notable deals in the past year include Williams’s acquisition of Trace Midstream’s gathering and processing assets in the Haynesville region.4 Targa Resources acquired Blackstone Energy Partners’ 25% interest in Grand Prix NGL Pipeline.5 Also, Energy Transfer acquired infrastructure company Lotus Midstream.6 Elsewhere, Phillips 66 just completed the purchase of the remaining portion of DCP Midstream.7 While some companies may expand their current assets or move into the renewable energy sector, others may focus on developing projects in the Permian and Haynesville.

OPEC+ Cuts Create an Opportunity for U.S. Production

At its June meeting, OPEC+ agreed to the 1.16 million barrels per day (Mb/d) voluntary decrease that was proposed back in April. The cuts will remain in effect until the end of 2024, with the possibility of an extension into 2025.8 Saudi Arabia made it clear that it would take any step necessary to stabilize the oil market. In fact, for the Saudi economy to achieve fiscal stability and start funding essential projects for the country such as the $500 billion Neom city, it needs higher oil prices. The Saudis committed to reducing production by an additional 1 million barrels per day beginning in July, which would reduce the country’s oil output to its lowest point in decades. The move would help them achieve their goal of establishing a floor for the oil markets, or at least to mitigate crude oil price drops for the remainder of the year.9

Russia did not commit to reducing its output any further, and the United Arab Emirates received permission to raise its output targets for the year. The United Arab Emirates has made significant investments in its manufacturing sector, but underinvestment in nations like Nigeria and Angola make it difficult for them to reach output goals.10

Oil price volatility and uncertainty are likely to remain high on the supply side as the market waits on the possibility that the Saudis could further extend production cuts.11 Moreover, concerns about the potential impact of further interest rate hikes on the global economy may pressure energy demand;12 while rising U.S. and China’s domestic and international aviation activity are factors that could lead supply to ramp up.13

Despite the extension of OPEC+ production cuts, the U.S. Energy Information Administration (EIA) forecasts global liquid fuels production will increase by 1.5 million barrels per day (Mb/d) in 2023 and by 1.3 Mb/d in 2024, primarily because of growth from non-OPEC producers. Among the leading sources of non-OPEC growth are the United States, Norway, Canada, Brazil, and Guyana.14

Increased U.S. oil and natural gas production can close supply gaps in the global energy market, especially in Europe, where there are concerns again about global competition for LNG cargos. Gas shipments from the United States to Europe are scarcer with supply funneling to Asia, where prices are more competitive in the summer months due to stronger demand for cooling.15

Therefore, although the sector has been on a protracted upswing, we still think it’s an attractive investment. Moreover, as discussed in our last Energy & MLP Insights, diversification opportunities and the ability to pass inflation along to investors are key strengths and also this past quarter the industry has continued to show high distribution yields and low valuations.

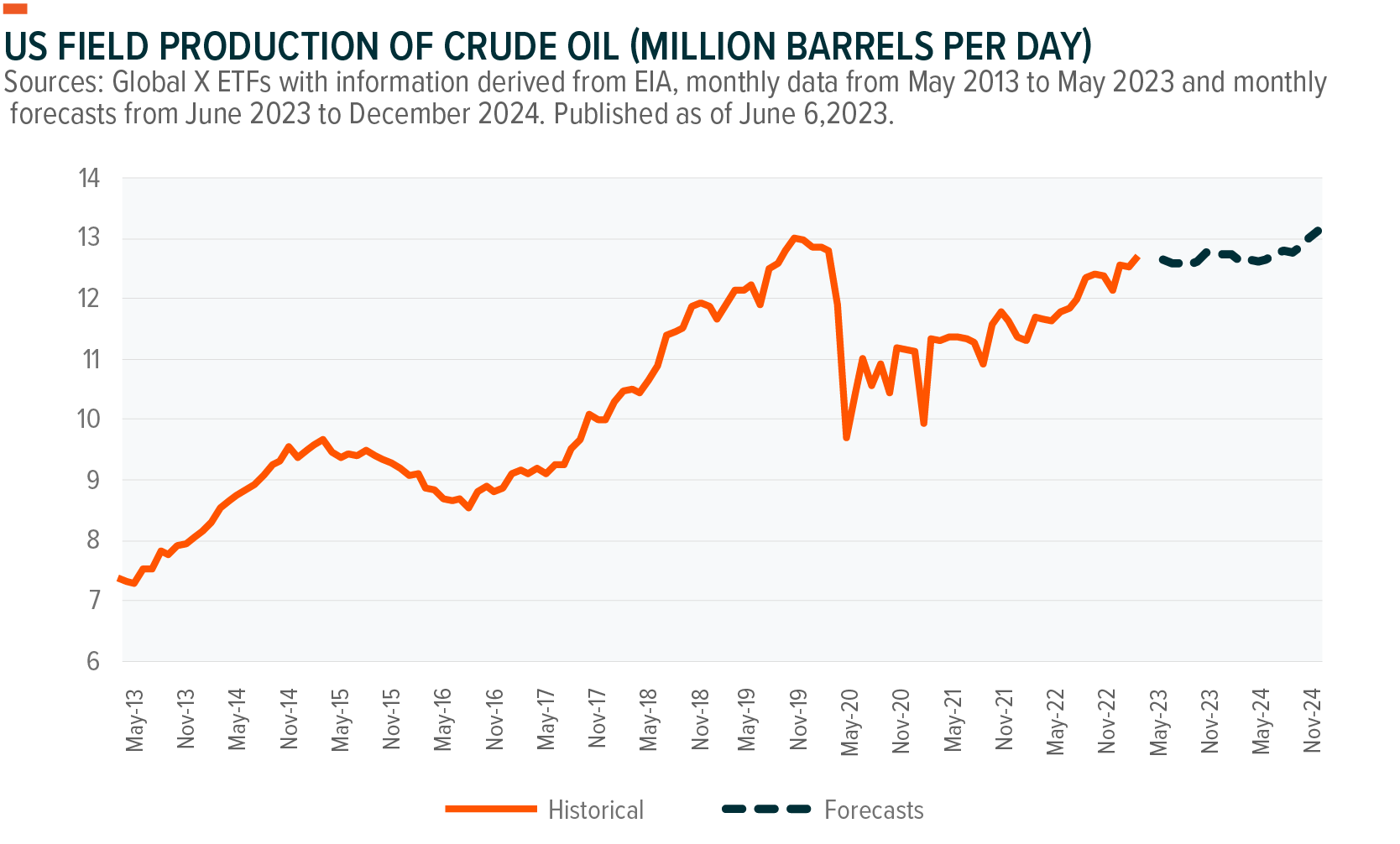

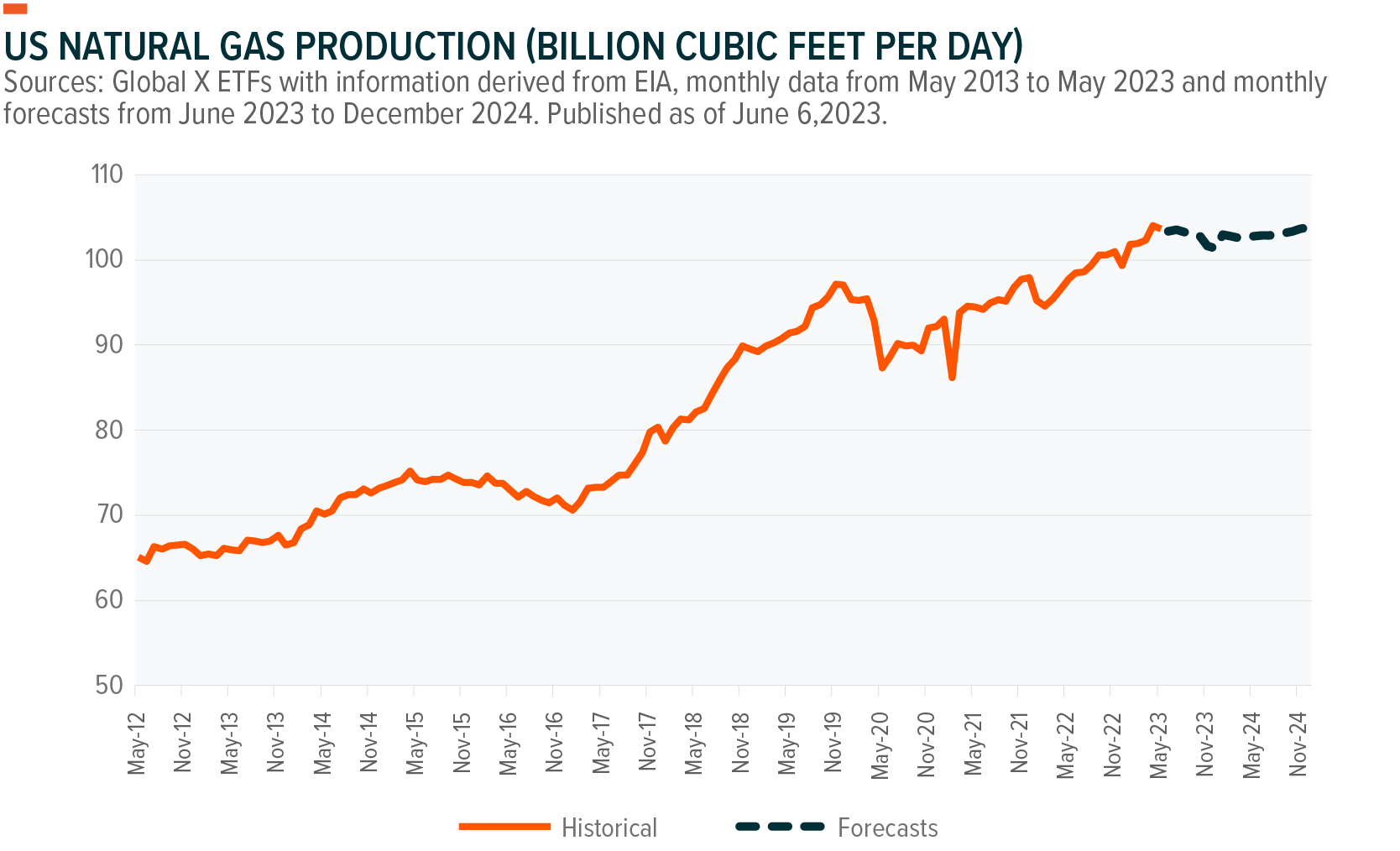

U.S. Oil & Gas Outputs at Record Highs Support U.S. Midstream Sector

In April, U.S. dry natural gas output reached a record 104 billion cubic feet per day (Bcf/d), up from 102 Bcf/d in March. The record was set despite March and April Henry Hub natural gas prices at $2.50 per million British thermal units (MMBtu), about $4.00 below the 2022 annual average. The Haynesville region in northeastern Texas and northern Louisiana and the Permian Basin in western Texas and southeastern New Mexico led production growth.16

The EIA expects dry natural gas production to average around 103 Bcf/d in the second half of 2023 and in 2024. The EIA expects record U.S. crude oil production to continue with a forecast of 13.11 Mb/d in December 2024, driven primarily by production growth in the Permian Basin. Since our March Energy & MLP Insights, in June, the EIA revised its 2023 and 2024 forecasts for average U.S. oil and gas production. For gas, the EIA’s estimates increased 2.1% from 100.67 Bcf/d to 102.74 Bcf/d for 2023 and 1.3% from 101.69 Bcf/d to 103.04 Bcf/d for 2024. For oil, the estimates increased 0.9% from 12.44 Mb/d to 12.56 Mb/d for 2023 and 1.1% from 12.63 Mb/d to 12.67 Mb/d for 2024.17

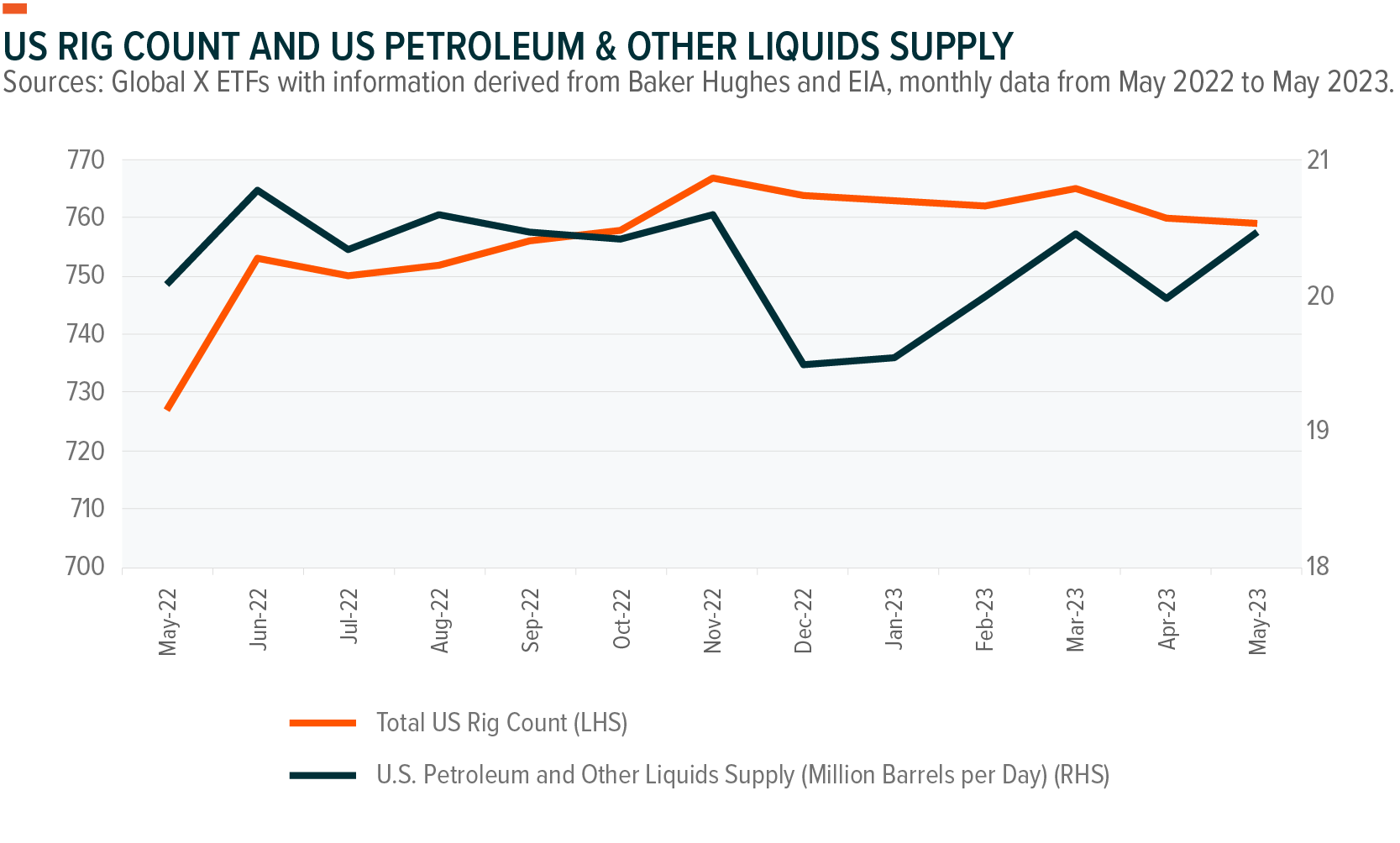

Although Permian Basin-related natural gas output has increased, natural gas-directed drilling has decreased overall due to the price dip. However, reducing the number of active rigs does not necessarily lower production. Frac fleet activity is a better predictor of production than rig numbers, and frac fleets can sustain basin production. JP Morgan raised its forecast for total U.S. energy supply after adjusting basin-level production forecasts for dropped rigs and brought them in line with productivity measures.18

Capital expenditure is another consideration in this environment. Based on a peer group of 24 corporations, representative of the midstream sector, capital expenditures should increase by $5.4 billion year-over-year, or 17%, to $38.4 billion in 2023. Cost inflation is a factor, and midstream companies typically invest in more modest growth projects.19 However, North American oil and gas production potentially rising further in 2023 could support midstream operator throughput expansion. Several projects under construction could boost Permian and Haynesville capacity. And strong Permian production growth raises the need for additional gas egress, as pipelines may reach maximum capacity this year.20

Among the notable leading spenders is TC Energy, despite recent large Coastal GasLink cost overruns and expenditures for organic growth projects. Also, the backlog of projects at Enbridge could increase expenditure by $1.3 billion.21

Conclusion: U.S. Midstream Offers Unique Exposure to Energy

The United States is producing the most energy it ever has, which means that the need for midstream infrastructure is likely to remain strong. OPEC+’s agreement to reduce output further may increase price volatility but benefit the U.S. energy sector. In our view, these factors bolster midstream’s investment profile, even as price volatility remains high. Midstream MLPs’ fee-based business models and contractual escalators mean they are not as correlated to energy prices as other energy sectors. When considering exposure, it’s important to remember that their business models and their core functions as facilitators, including processing, storing, and transporting oil and gas, make their association with oil and gas prices unique.

Related ETFs

MLPA – Global X MLP ETF

MLPX – Global X MLP & Energy Infrastructure ETF

Click the fund name above to view current holdings. Holdings are subject to change. Current and future holdings are subject to risk.