Mapping the Cloud: A Look at the Segments Driving Growth

In today’s world where robust digital infrastructure and remote work arrangements are vital, we increasingly hear about the importance of the cloud – the virtual space where software applications run, data reside, and computing occurs.

A few firms’ services may immediately come to mind when discussing the cloud: Amazon’s AWS, Microsoft’s Azure, and Alphabet’s Google Cloud. These are part of the public Infrastructure-as-a-Service (IaaS) cloud segment that offers customers scalable and dynamic IT environments. Their emergence reflects a shift away from the localized computing paradigm of the past, where individuals and enterprises ran software on desktop computers and stored data in on-premises servers.

Yet, the cloud computing industry extends far beyond name-brand IaaS cloud providers. Software-as-a-Service (SaaS) and Platform-as-a-Service (PaaS) companies build their products on top of cloud infrastructure and provide solutions across and within certain verticals. These products can range from HR or CRM software to solutions specifically designed for health care providers. Such companies tend to be cloud-natives, developed from the ground up to offer their services to any device with an internet connection.

In the following piece, we explore the cloud ecosystem’s distinct segments, identifying some of the key trends and investment rationales that are relevant to today’s technology investors.

Public Clouds Rain on Physical IT’s Parade

Public cloud service providers, or hyperscalers, offer on-demand data storage and processing. These services are centralized in shared data centers and accessed via the internet. In the IaaS business model, enterprises and individuals typically pay cloud providers on a recurring basis, with costs determined by the services subscribed to and the volume of usage.

Recently, hyperscalers’ growth outpaced that of other cloud segments: Gartner estimates that IaaS-based revenues grew 27.5% in 2019, ahead of the PaaS (21.8%) and SaaS (18.5%) segments.1 Forecasts predict a similar growth trajectory, with IaaS revenues reaching $76B by 2022, up from $39B in 2019 representing a 25.3% CAGR.2 What drives this growth? Traditional on-premise IT environments require costly upkeep and expertise to manage. Integrating the technologies that make up such infrastructure also presents significant challenges.

IaaS companies address these pain points by taking IT resource management out of clients’ hands. Law firms, hospitals, and other enterprise clients without IT expertise are more than happy to offload these function to IaaS providers. To them, it means predictable IT costs, far fewer processes to manage, and more reliable and readily accessible tech infrastructure.

Hyperscale infrastructure can wrap around legacy systems like local servers, coexist alongside other public or private clouds in what is called a hybrid cloud, and serve as the foundational infrastructure for myriad SaaS cloud applications. This dynamism expands the reach of cloud providers. In a 2019 survey of 800 enterprises, 85% employed public cloud solutions.3

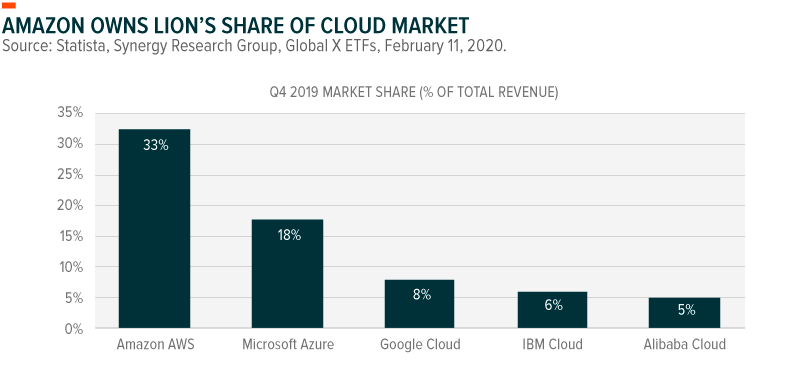

Ranked by market share, the major players in the segment are Amazon’s AWS (33%), Microsoft’s Azure (18%), Alphabet’s Google Cloud (8%), and IBM Cloud (6%).4 These cloud providers represent some of the largest companies in the world by market cap and overall revenue. None began as cloud companies, but each recognized the growth opportunity presented by the structural shift toward external IT infrastructure and leveraged their significant resources and experience to build out cloud offerings.

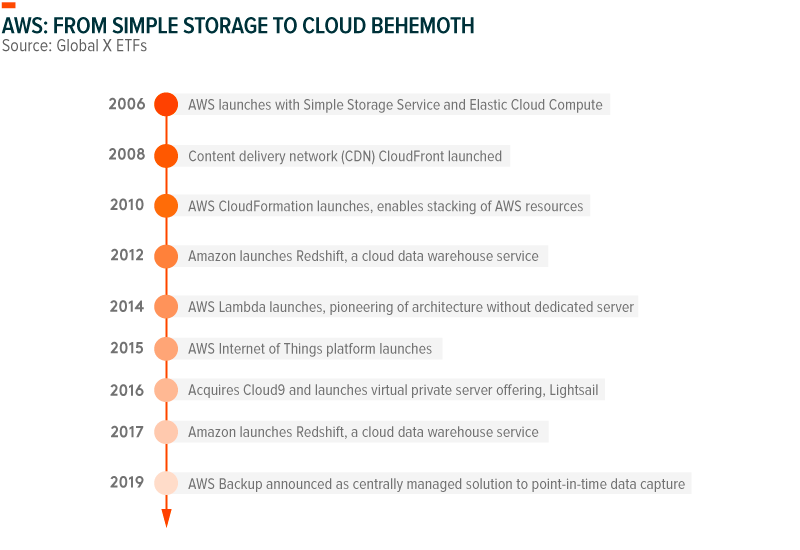

Currently the segment’s leader, Amazon pioneered the IaaS concept with the advent of Amazon Web Services (AWS) and the 2006 launches of Amazon Elastic Compute Cloud and Simple Storage Service. In the years since, Amazon invested in software engineers and data centers, spending tens of billions in CapEx to establish a server/network infrastructure presence in over 245 countries and territories.5 They built myriad services on top of their initial offering, including relational database services (Amazon RDS) and data warehousing services (Amazon Redshift) and made strategic acquisitions to complement and augment them. In 2015, they purchased Israeli chipmaker Annapurna Labs for an estimated $350M. Today, Annapurna’s tech serves as the foundation for Amazon’s custom AWS Graviton Processor and cloud-based Machine Learning chips.6 These investments paid off, with AWS becoming a profit machine. In 2019, AWS generated 12.5% of Amazon’s total revenue but 63% of their operating income.7

Other hyperscalers similarly invested in their public cloud segments to bring them to scale as viable cloud infrastructure options. In 2018, top hyperscalers’ combined data center CapEx reached a record $128B.8 And over the past two years, these same companies made significant acquisitions looking to chip away at AWS’ market share. Last year, IBM acquired leading enterprise cloud software developer RedHat for $35B, while Google spent a reported $250M for cloud storage company Elastifile.9,10

Beyond acquisitions designed to deepen their offerings, hyperscalers added cloud migration companies to their portfolios to facilitate adoption of their respective platforms. Google purchased mainframe-to-cloud migration company Cornerstone Technology this past February and last October Microsoft acquired Movere to streamline the migration of applications and infrastructure to Azure.11,12

Though Amazon’s pioneering efforts give them a head start, directing a strategic focus on cloud infrastructure paid off for other hyperscalers as well. Microsoft’s most recent fiscal quarter saw Azure revenues grow 27% year-over-year (YoY) to $12.5B for the period, representing almost 34% of Microsoft’s total revenues.13 Google, too, shows promise, reporting that cloud revenue grew 53% YoY to $2.6B last quarter.14 Considering Google’s multi-cloud focus and that cloud workloads are expected to grow 20% in the next three years, there is untouched ground for them to lay stakes in.15

We expect the IaaS segment to be a battleground for hyperscalers in the coming years. Strategic acquisitions and hires should continue to tick upwards as these companies look to expand and differentiate their offerings and attract new business. Large contracts like Microsoft’s recent $10B deal to provide cloud services to the Pentagon should distribute revenues across major providers and foster competition.16 And growing demand for multi-cloud environments across different providers will likely give footing to those with less established customer bases.

In our view, hyperscale exposure could serve as a valuable growth component in investors’ portfolios as providers further scale their operations. At the same time however, many of the major IaaS providers derive the majority of their revenues from other sources, like ecommerce, advertising, operating systems. Therefore while IaaS provides the backbone to the cloud computing ecosystem, we believe other segments offer greater purity to the cloud computing theme, while presenting similarly attractive business models and growth prospects.

SaaS Is Just Getting Started

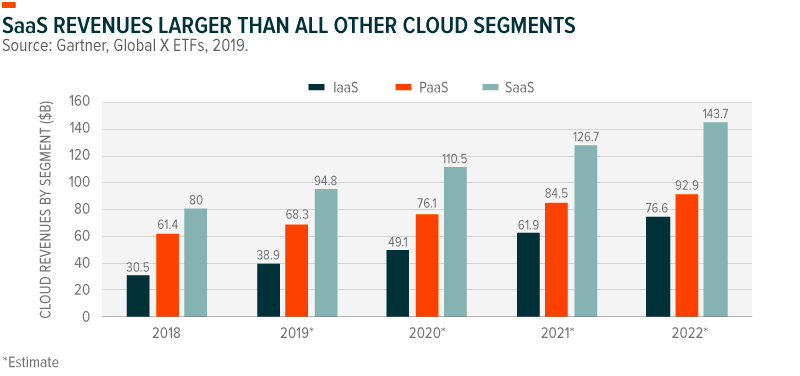

Software-as-a-Service generates more revenue than any other cloud segment. In 2019, combined SaaS revenues totaled $94.8B, ahead of PaaS ($61.4B), IaaS ($38.9B) and other cloud segments ($10.5B).17 SaaS revenues should continue to eclipse other cloud segments in the near- and long-term – by 2022, they are expected to reach $144B.18 Adding credence to SaaS maintaining its significant revenue-share, Cisco expects that by 2021, 75% of all cloud workloads and computing instances will come from SaaS applications versus 16% for IaaS and 9% for PaaS.19

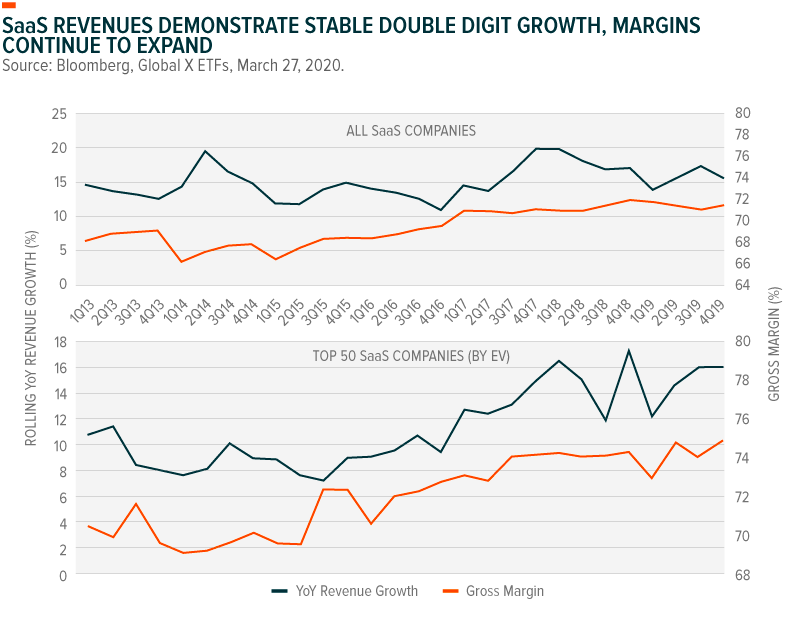

SaaS presents an attractive business model that has the potential to support long-term growth. Subscription fees generate recurring, sticky, and projectable cash flow. Once companies integrate software into their processes and their employees become accustomed to it, it becomes very difficult to fire that SaaS provider – even if fees are increased. The ingrained nature of this relationship creates direct-to-consumer marketing channels through which they can upsell product, further driving potential revenues. Over the last decade, revenues grew as the segment matured. From 2013 to 2016, quarterly SaaS revenues grew by an average 14% YoY and in the three years since, this average reached 17%.20 In recognition of expected growth, SaaS companies tend to have valuations that are multiples of current revenues – in Q4 2019, the top 50 SaaS companies by valuation totaled $1.5T in enterprise value on a $194.7B revenue run rate with an average EV/Sales multiple of 10.5x.21 But in our view, these multiples are warranted given how the SaaS business model could continue to offer profitability potential. They are not due to a growth at any cost mentality.

SaaS companies’ cost structures are largely fixed: they develop software and sell it to as many clients as possible with little and predictable incremental costs. Partnerships with hyperscalers partially contribute to this by presetting back-end infrastructure expenses – Salesforce, for example, enlisted AWS as its primary public cloud provider in a 4-year, $400M agreement.22 These characteristics allow for significant profit margin expansion as SaaS companies add more clients and upsell additional features.

In 2019, the median gross margin for public SaaS companies was 72%, up from 68% in 2014.23 Though customer acquisition cost ratios (CAC) ticked upward due to increased market saturation and penetration – in 2018, $1 of new annual recurring revenue (ARR) cost a median $1.14 versus $1.11 in 2017 – organic ARR growth far outpaces the CAC increase.24,25 Including new customers, upsells, and expansions, organic ARR grew 36% YoY in 2018.26 Simply put, SaaS companies are attracting new customers, retaining existing customers, and upselling expanded services, with all of these things supporting higher profit margins.

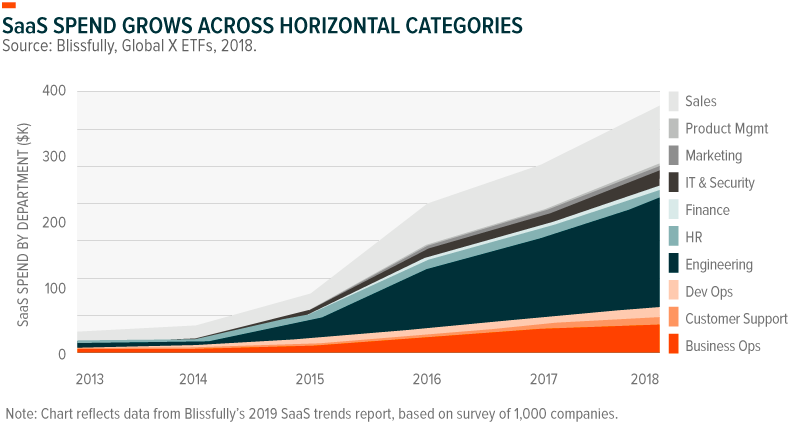

Horizontal Solutions Push Broad Shift to SaaS

SaaS applications offer streamlined solutions and enhancements at multiple levels of organizations’ business operations and across most industry verticals. Horizontally-architected SaaS applications serve specific functions to enterprises across industries. They can include software for enterprise resource planning (ERP), customer relationship management (CRM), compliance, HR, and cybersecurity.

The horizontal SaaS business model is mature and companies that develop such applications tend to be large enterprises themselves. Their scale and level of embeddedness mean that many also fall into the PaaS bucket, where external developers can develop and/or offer software on platform to complement the primary SaaS offering.

Salesforce CRM is one example of a company that hosts horizontally architected SaaS applications. The firm started as a web-based solution to customer relationship management, and today offers an entire suite of enterprise applications focused on business optimization. Some of these applications are the result of internal development – Salesforce Einstein for instance. Though many joined through M&A, like the recent acquisition of data visualization-leader Tableau. Additionally, Salesforces’ evolution illustrates how such companies can evolve into large-scale platforms. Many of the applications offered on AppExchange, Salesforce’s enterprise software marketplace, come from 3rd party developers who built them on the Salesforce Lightning or Heroku development platforms.27

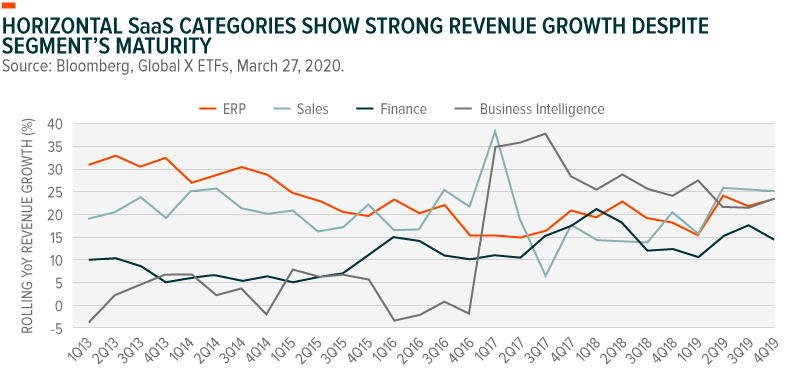

SaaS spend has increased in recent years, both overall and within specific segments – 81% of companies expect to increase SaaS spending more in 2020.28 We expect this spend to increase in many departments, benefiting horizontal SaaS companies across most categories. Looking at the chart below, we expect strength in companies that offer software focusing on ERP, finance and spend management, sales, and business intelligence. That said, future growth is no guarantee and investors should remain cognizant of potential risks and factors that could limit growth prospects.

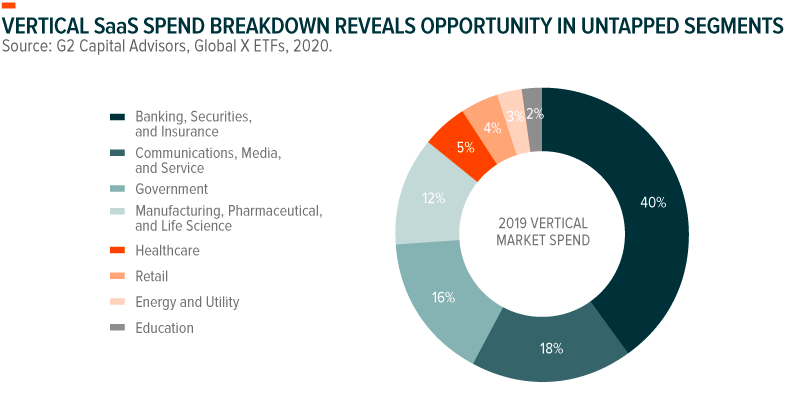

Vertically Integrated Solutions Offer Earlier Stage Growth

Vertically architected applications, on the other hand, offer broader services that cater to specific industries. Companies in this space tend to be earlier on in their lifecycles, and could consist of those that develop healthcare-oriented applications designed specifically for doctors, education platforms built for colleges and universities, or property management software that serves the housing industry.

For investors, vertical SaaS companies can offer exposure to earlier stage growth opportunities, while still benefiting from exposure to the SaaS business model. From the chart below, we can see that demand for vertical SaaS applications spans most industries.

Certain segments could see additional penetration. Some estimate that 2020 manufacturing software spend could reach $91.1B, a 8.3%YoY increase, and that healthcare spend could reach $24.8B, a 7.4% YoY increase.29 Novel industries like cannabis are mostly untapped and could expect to see new software solutions that meet their specific needs. Venture capital investment in cannabis-related SaaS companies grew by an estimated 45% in 2019 (YoY), with $153M invested since 2017.30

As of now, there are a limited number of publicly traded vertical SaaS companies. Yet, software review aggregator G2 listed over 34,000 SaaS products across 745 vertical SaaS categories in 2018.31 We expect a surge of vertical SaaS IPOs in the coming years, expanding the breadth of software-based exposure to industries and more granular sub-categories.

Looking ahead, there will be winners and losers across all segments as the market matures. We expect this to hold especially true in the more established horizontal SaaS categories where there are multiple players competing for market share. Heightened M&A activity is also likely to continue as firms look to further diversify their offerings and client bases. This trend will consolidate some segments and should dampen the impact of oversaturation. Overall, we see SaaS as an attractive technology segment that offers investors both growth opportunity and exposure to stable revenue streams. But as with any investment, increased adoption and maturation could possibly limit future growth prospects.

Cloud Computing in Our Rapidly Evolving World

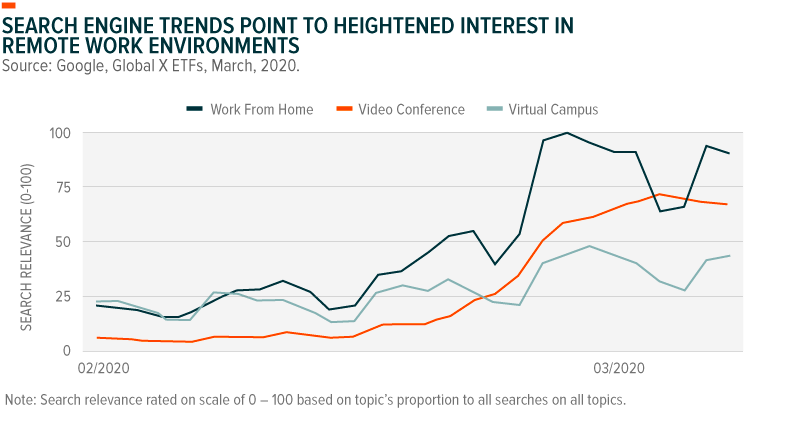

The COVID-19 pandemic and its disruptive impact on economies, societies, and industries around the world is placing a new emphasis on cloud-based solutions. Many governments shuttered non-essential businesses and encouraged workers to work from home if possible. For many, cloud infrastructure and software as a service makes it possible for critical business functions to operate as usual. Requiring only a computer and an internet connection, employees can use the same applications they would in the office, access files stored on their companies’ servers and collaborate with their colleagues through virtual work environments.

As the world recovers, learns, and adapts from this crisis, we expect companies and their employees to place an even greater emphasis on migrating to cloud-based solutions. The flexibility to work from the office, at home, or on the road, is now a key piece of business operations and continuity planning.

Conclusion

Migrating to cloud-based infrastructure and software affords enterprises greater flexibility, predictability, and scale. The transformative power of cloud-based solutions ingrains the companies that offer such services in their clients’ business operations, enhances productivity, and controls costs. Despite these features, the business world has yet to fully adopt cloud computing. There remain opportunities across industries and within organizations to further leverage SaaS and IaaS solutions. And with increased demand for virtual work environments, such adoption is likely to accelerate in the coming years, fueling further across the ecosystem.

Related ETFs:

CLOU: The Global X Cloud Computing ETF (CLOU) seeks to invest in companies positioned to benefit from the increased adoption of cloud computing technology, including companies whose principal business is in offering computing Software-as-a-Service (SaaS), Platform-as-a-Service (PaaS), Infrastructure-as-a-Service (IaaS), managed server storage space and data center real estate investment trusts, and/or cloud and edge computing infrastructure and hardware.

Please click the fund name above for holdings information.

1. Gartner, “Gartner Forecasts Worldwide Public Cloud Revenue to Grow 17.5 Percent in 2019,” April 2, 2019.

2. Ibid.

3. Flexera, “2019 State of the Cloud,” 2019.

4. Statista, “Amazon Leads $100 Billion Cloud Market,” February 11, 2020.

5. Amazon, “Why Cloud Infrastructure Matters,” 2020.

6. Forbes, “How An Acquisition Made By Amazon In 2016 Became Company’s Secret Sauce,” March 10, 2019.

7. The Motley Fool, “Amazon’s Record 2019 in 7 Metrics,” February 6, 2020.

8. CRN, “Hyper-Scale Data Center ‘Capex Kings’ Spend Record $120 Billion,” March 15, 2019.

9. RedHat, “IBM Closes Landmark Acquisition of Red Hat for $34 Billion; Defines Open, Hybrid Cloud Future,” July 9, 2020.

10. Seeking Alpha, “Google to acquire Elastifile, reportedly for $200M-$250M,” July 9, 2019.

11. Google, “Google Cloud acquires Cornerstone Technology to help you migrate your mainframe,” February 19, 2020.

12. VentureBeat, “Microsoft acquires Mover to bolster cloud migration solutions,” October 21, 2019.

13. SDX Central, “Microsoft Cloud Momentum Send Q2 Earnings Soaring,” January, 2020.

14. ZDNet, “Google Cloud hits a $10B annual revenue run rate,” February 3, 2020.

15. CNBC “Microsoft Azure has an edge over Amazon Web Services at big companies, Goldman Sachs survey says,” January 7, 2020.

16. Wall Street Journal, “Microsoft’s Challenge of Amazon in the Cloud Gains Force,” October 27, 2019.

17. Gartner, “Gartner Forecasts Worldwide Public Cloud Revenue to Grow 17.5 Percent in 2019,” April 2, 2019.

18. Ibid.

19. Cisco, “Cisco Global Cloud Index: Forecast and Methodology, 2016-2021,” 2018.

20. Bloomberg, Global X ETFs as of March 26, 2020.

21. Bloomberg, Global X ETFs as of March 26, 2020.

22. Wall Street Journal, “In $400 Million Deal, Salesforce to Piggyback on Amazon’s Growing Cloud,” May 25, 2016.

23. Bloomberg, Global X ETFs as of March 26, 2020.

24. KeyBanc, “2018 SaaS Survey Results,” 2018.

25. KeyBanc, “2019 SaaS Survey Results,” 2019.

26. Ibid.

27. Salesforce, “What is PaaS? – Platform as a Service Explained,” 2020.

28. Flexera, “2020 State of Tech Spend,” 2020.

29. Bowery Capital, “Opportunities in Vertical Software v2.0,” June, 2016.

30. Bowery Capital, “SaaS Opportunity in the Cannabis Vertical,” June 28, 2019.

31. G2 Learning Hub, “Saturation of the SaaS Industry,” May 21, 2018.